You might also like

- TOA 2012 Mock ExamDocument8 pagesTOA 2012 Mock ExamCharry RamosNo ratings yet

- Final Preboard Examination ReviewDocument15 pagesFinal Preboard Examination ReviewLester AguinaldoNo ratings yet

- Income Tax Deductions GuideP15,000,0005,000,000P20,000,0002,000,000P18,000,0003,300,000P5.45Document10 pagesIncome Tax Deductions GuideP15,000,0005,000,000P20,000,0002,000,000P18,000,0003,300,000P5.45Keysi02No ratings yet

- Partnership Operations: Problem CDocument3 pagesPartnership Operations: Problem CJoeneil DamalerioNo ratings yet

- IFRS 1 Presentation of Financial StatementsDocument14 pagesIFRS 1 Presentation of Financial StatementsCatherine RiveraNo ratings yet

- Practical Accounting 1Document3 pagesPractical Accounting 1Angelo Otañes GasatanNo ratings yet

- PSA 560 Auditor Responsibilities for Subsequent EventsDocument1 pagePSA 560 Auditor Responsibilities for Subsequent EventsDanielle Potter RadcliffeNo ratings yet

- Chapter 12 - Test BankDocument25 pagesChapter 12 - Test Bankgilli1tr100% (1)

- Fundamentals of Audit and Assurance ServicesDocument50 pagesFundamentals of Audit and Assurance ServicesAndrea ValdezNo ratings yet

- FAR-4102b (Lecture Notes - Discontinued Operations & NCA Held For Sale)Document2 pagesFAR-4102b (Lecture Notes - Discontinued Operations & NCA Held For Sale)Eira ShaneNo ratings yet

- 13th NCR Cup Series 7 SGVDocument9 pages13th NCR Cup Series 7 SGVrcaa04No ratings yet

- Finals Reviewer AudtheoDocument36 pagesFinals Reviewer AudtheoMae VillarNo ratings yet

- Problem 3 5 6 Special TransactionDocument5 pagesProblem 3 5 6 Special TransactionBabyann BallaNo ratings yet

- RFBT Quiz 1 B45 PDFDocument5 pagesRFBT Quiz 1 B45 PDFrose annNo ratings yet

- Donor's TaxDocument1 pageDonor's TaxJustineMaeMillanoNo ratings yet

- AfardocDocument14 pagesAfardocJhedz CartasNo ratings yet

- AFAR-03 (Corporate Liquidation)Document6 pagesAFAR-03 (Corporate Liquidation)Maricris AlilinNo ratings yet

- Exercises 04 - Intangibles INTACC2 PDFDocument3 pagesExercises 04 - Intangibles INTACC2 PDFKhan TanNo ratings yet

- BLT 2008 First Pre-Board August 2Document15 pagesBLT 2008 First Pre-Board August 2Lester AguinaldoNo ratings yet

- Ap 9004-IntangiblesDocument5 pagesAp 9004-IntangiblesSirNo ratings yet

- CPA firm considerations accepting new clientsDocument19 pagesCPA firm considerations accepting new clientsNathalie PadillaNo ratings yet

- Fin MarDocument2 pagesFin MarKoleen Mae LindayenNo ratings yet

- UCP Tax Guide: Income Tax for IndividualsDocument9 pagesUCP Tax Guide: Income Tax for IndividualsDin Rose GonzalesNo ratings yet

- Partnership and Corporation AccountingDocument2 pagesPartnership and Corporation AccountingEmman S NeriNo ratings yet

- Advanced Financial Accounting Midterm: For Questions 2-4Document13 pagesAdvanced Financial Accounting Midterm: For Questions 2-4Mister MysteriousNo ratings yet

- Crc-Ace Review School: TAXATION (1-70)Document10 pagesCrc-Ace Review School: TAXATION (1-70)LuisitoNo ratings yet

- Chapter 10 Identifying and Assessing The Risks of Material MisstatementsDocument7 pagesChapter 10 Identifying and Assessing The Risks of Material MisstatementsRichard de LeonNo ratings yet

- Cash Equivalents Financial ReportingDocument4 pagesCash Equivalents Financial ReportingKeanna Denise GonzalesNo ratings yet

- Module 4 Accounting For TaxesDocument14 pagesModule 4 Accounting For TaxesFujoshi BeeNo ratings yet

- Financial Planning and Forecasting: Multiple Choice: ConceptualDocument2 pagesFinancial Planning and Forecasting: Multiple Choice: ConceptualKristel SumabatNo ratings yet

- Cash ReviewerDocument35 pagesCash ReviewerAprile AnonuevoNo ratings yet

- Wiley Basic ActgDocument30 pagesWiley Basic ActgstarstarstarNo ratings yet

- RFBT Plmor-4-7Document9 pagesRFBT Plmor-4-7KyohyunNo ratings yet

- Auditing Theory Overview of The Audit Process With AnswersDocument44 pagesAuditing Theory Overview of The Audit Process With AnswersNikolajay MarrenoNo ratings yet

- PSU Financial QuizDocument3 pagesPSU Financial QuizRanjit SandovalNo ratings yet

- Essay On Assurance EngagementDocument2 pagesEssay On Assurance EngagementSheena ClataNo ratings yet

- AT-02 Q Assurance and Non-Assurance ServicesDocument43 pagesAT-02 Q Assurance and Non-Assurance ServicesNicale JeenNo ratings yet

- 21 x12 ABC DDocument5 pages21 x12 ABC DAnjo PadillaNo ratings yet

- Auditing fraud risk factors and responsibilitiesDocument2 pagesAuditing fraud risk factors and responsibilitiesnhbNo ratings yet

- RESA TOA Special Handouts MAY2015Document11 pagesRESA TOA Special Handouts MAY2015Jeffrey CardonaNo ratings yet

- PRELEC1 Final ExamDocument4 pagesPRELEC1 Final ExamAramina Cabigting BocNo ratings yet

- CashDocument37 pagesCashRyan SanchezNo ratings yet

- Basic accounting for defined benefit plansDocument23 pagesBasic accounting for defined benefit plansKristine Diane CABAnASNo ratings yet

- FAR 4310 Investment Property Other Fund InvestmentsDocument5 pagesFAR 4310 Investment Property Other Fund InvestmentsATHALIAH LUNA MERCADEJASNo ratings yet

- Accountancy exam reviewDocument4 pagesAccountancy exam reviewJERROLD EIRVIN PAYOPAYNo ratings yet

- Applied Auditing Audit of Receivables Problem 1: QuestionsDocument9 pagesApplied Auditing Audit of Receivables Problem 1: QuestionsPau SantosNo ratings yet

- TOA CparDocument12 pagesTOA CparHerald Gangcuangco100% (2)

- Basic Accounting - Midterm 2009Document6 pagesBasic Accounting - Midterm 2009Trixia Floie GalimbaNo ratings yet

- TA-258: STATEMENT OF COMPREHENSIVE INCOME & ACCOUNTING CHANGESDocument5 pagesTA-258: STATEMENT OF COMPREHENSIVE INCOME & ACCOUNTING CHANGESfggfdgdsNo ratings yet

- Review School of Accountancy First Pre-Board Examination Theory of Accounts QuestionsDocument12 pagesReview School of Accountancy First Pre-Board Examination Theory of Accounts QuestionsPhilip CastroNo ratings yet

- CFAS Testbank Answer KeyDocument14 pagesCFAS Testbank Answer KeyPrince Jeffrey FernandoNo ratings yet

- CFASDocument15 pagesCFASCamille Anne GalvezNo ratings yet

- Img 0008Document1 pageImg 0008Bernadette BenignosNo ratings yet

- Soal Compre 020418Document7 pagesSoal Compre 020418mayda nurul alamsariNo ratings yet

- Conceptual Framework and Accounting StandardsDocument15 pagesConceptual Framework and Accounting StandardsPrince Jeffrey FernandoNo ratings yet

- Promotion Test for Assistant ManagerDocument10 pagesPromotion Test for Assistant ManagerVimalKumarNo ratings yet

- Project: Bill IsDocument8 pagesProject: Bill IsN.J. PatelNo ratings yet

- Chap 018Document60 pagesChap 018Amit JindalNo ratings yet

- ch07 CASH AND CAH EQUIVALENTDocument30 pagesch07 CASH AND CAH EQUIVALENTMichael Vincent Buan SuicoNo ratings yet

- PRTC - Final PREBOARD Solution Guide (1 of 2)Document4 pagesPRTC - Final PREBOARD Solution Guide (1 of 2)Charry RamosNo ratings yet

- PRTC Preboard Solutions Guide and Key AnswersDocument17 pagesPRTC Preboard Solutions Guide and Key AnswersCharry RamosNo ratings yet

- CRC Solution Set A & Set BDocument2 pagesCRC Solution Set A & Set BCharry RamosNo ratings yet

- Bl.m-1402.Law On ContractsDocument23 pagesBl.m-1402.Law On ContractsCharry RamosNo ratings yet

- Certs - Auditing Problems Quizzers 2013Document14 pagesCerts - Auditing Problems Quizzers 2013Charry RamosNo ratings yet

- PRTC Preboard Solutions Guide and Key AnswersDocument17 pagesPRTC Preboard Solutions Guide and Key AnswersCharry RamosNo ratings yet

- IM Ch14-7e - WRLDocument25 pagesIM Ch14-7e - WRLCharry RamosNo ratings yet

- BLT Quizzer (Unknown) - Law On Negotiable InstrumentsDocument7 pagesBLT Quizzer (Unknown) - Law On Negotiable InstrumentsJasper Ivan PeraltaNo ratings yet

- Stock Valuation ModelsDocument21 pagesStock Valuation ModelsAnonymous FFeOk16cINo ratings yet

- Donors Tax Theory ExplainedDocument5 pagesDonors Tax Theory ExplainedJoey Acierda BumagatNo ratings yet

- Certs - Auditing Problems Quizzers 2013Document14 pagesCerts - Auditing Problems Quizzers 2013Charry RamosNo ratings yet

- Segment ReportingDocument1 pageSegment ReportingCharry RamosNo ratings yet

- P1 Final Preboard - May 2011Document3 pagesP1 Final Preboard - May 2011Charry RamosNo ratings yet

- PRTC Preweek - Toa Partii - 2014Document7 pagesPRTC Preweek - Toa Partii - 2014Charry RamosNo ratings yet

- CHAPTER 2 Caselette - Correction of ErrorsDocument37 pagesCHAPTER 2 Caselette - Correction of Errorsmjc24100% (4)

- Practical Accounting 1: I ExamcoverageDocument12 pagesPractical Accounting 1: I ExamcoverageCharry Ramos0% (2)

- (Sffis: The 8tel. 735 9807 AccountancyDocument18 pages(Sffis: The 8tel. 735 9807 AccountancyCharry RamosNo ratings yet

- Audit of Stockholders EquityDocument25 pagesAudit of Stockholders Equityxxxxxxxxx87% (39)

- Single Entry FormulasDocument3 pagesSingle Entry FormulasDexter DeeNo ratings yet

- CHAPTER 1 Caselette - Accounting CycleDocument51 pagesCHAPTER 1 Caselette - Accounting Cyclemjc24No ratings yet

- Discontinued Operations and Interim ReportingDocument3 pagesDiscontinued Operations and Interim ReportingRinokukunNo ratings yet

- Audit Investments ChapterDocument34 pagesAudit Investments ChapterMr.AccntngNo ratings yet

- Aud TheoDocument30 pagesAud TheoCharry RamosNo ratings yet

- Audit of ReceivablesDocument32 pagesAudit of Receivablesxxxxxxxxx96% (55)

- Toa 1Document14 pagesToa 1Charry RamosNo ratings yet

- CHAPTER 7 Caselette - Audit of PPEDocument34 pagesCHAPTER 7 Caselette - Audit of PPErochielanciola60% (5)

- PRTC - Final PREBOARD Solution Guide (1 of 2)Document4 pagesPRTC - Final PREBOARD Solution Guide (1 of 2)Charry RamosNo ratings yet

- CRC Solution Set A & Set BDocument2 pagesCRC Solution Set A & Set BCharry RamosNo ratings yet

- Profit and Loss Practice QuestionsDocument4 pagesProfit and Loss Practice QuestionsAkanksha SinghNo ratings yet

- Business PlanDocument18 pagesBusiness PlanAngelo Francis100% (2)

- Apple SWOT Analysis and CompetitorsDocument30 pagesApple SWOT Analysis and CompetitorsmarcosbiesaNo ratings yet

- Fundamental of Corporate Finance, chpt2Document8 pagesFundamental of Corporate Finance, chpt2YIN SOKHENGNo ratings yet

- Elasticity of Demand and SupplyDocument29 pagesElasticity of Demand and SupplyEmily Canlas DalmacioNo ratings yet

- Adani EnterprisesDocument41 pagesAdani Enterprisesprasad hegde0% (1)

- Coffee Table BookDocument4 pagesCoffee Table BookMiguel LigutanNo ratings yet

- Arizona Tax Rates TableDocument18 pagesArizona Tax Rates TableKaryll Trinidad AyangcoNo ratings yet

- Part1 Topic 3 Goodwill Nature and ValuationDocument20 pagesPart1 Topic 3 Goodwill Nature and ValuationShivani ChoudhariNo ratings yet

- What Is BudgetDocument4 pagesWhat Is BudgetDhanvanthNo ratings yet

- 4 Remuneration FormDocument2 pages4 Remuneration FormRDC SPUNo ratings yet

- 5Document2 pages5ABDUL WAHABNo ratings yet

- A Presentation On Special Economic Zones (SEZDocument29 pagesA Presentation On Special Economic Zones (SEZsvjiwaji96% (23)

- Kwame Nkrumah University Mechanical Engineering QuizDocument9 pagesKwame Nkrumah University Mechanical Engineering QuizMohammed Abdul-MananNo ratings yet

- Hamilton - Case A - 5 PDFDocument2 pagesHamilton - Case A - 5 PDFJayash Kaushal0% (1)

- A Primer On Structured FinanceDocument21 pagesA Primer On Structured FinanceBilyana PetrovaNo ratings yet

- APGLI Scheme ExplainedDocument25 pagesAPGLI Scheme ExplainedLunjala TeluguNo ratings yet

- Advanced Accounting May 2015 Suggested Answers PDFDocument26 pagesAdvanced Accounting May 2015 Suggested Answers PDFanupNo ratings yet

- Coca-Cola: Residual Income Valuation Exercise & Coca-Cola: Residual Income Valuation Exercise (TN)Document7 pagesCoca-Cola: Residual Income Valuation Exercise & Coca-Cola: Residual Income Valuation Exercise (TN)sarthak mendiratta100% (1)

- Installment SalesDocument12 pagesInstallment SalesAllyzzaBuhain100% (1)

- Module 2 - Pay For Position - Fixed Pay - FINAL - Oct2014Document101 pagesModule 2 - Pay For Position - Fixed Pay - FINAL - Oct2014zulianNo ratings yet

- United States Court of Appeals Tenth CircuitDocument7 pagesUnited States Court of Appeals Tenth CircuitScribd Government DocsNo ratings yet

- Ch1 - What Is Strategy - Why Is It ImportantDocument37 pagesCh1 - What Is Strategy - Why Is It ImportantFrancis Jonathan F. PepitoNo ratings yet

- 3 Significance of Working CapitalDocument4 pages3 Significance of Working CapitalShruti SehgalNo ratings yet

- Problem Set Capital StructureQADocument15 pagesProblem Set Capital StructureQAIng Hong100% (1)

- Integrated Strategy Optimisation for Complex Mining OperationsDocument8 pagesIntegrated Strategy Optimisation for Complex Mining OperationsCarlos A. Espinoza MNo ratings yet

- Sample: Study Question BankDocument64 pagesSample: Study Question BankWise Moon100% (1)

- Chapter 13 Property Plant and Equipment Depreciation and deDocument21 pagesChapter 13 Property Plant and Equipment Depreciation and deEarl Lalaine EscolNo ratings yet

- Integrated Annual Report 2017-18 Annual ReportDocument176 pagesIntegrated Annual Report 2017-18 Annual ReportMail and Guardian100% (1)

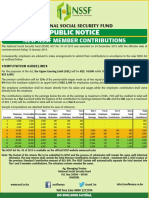

- Public Notice: New NSSF Member ContributionsDocument1 pagePublic Notice: New NSSF Member ContributionsDiana Dekatrinah KatrineNo ratings yet