You might also like

- AAU Community's Attitude Toward InsuranceDocument64 pagesAAU Community's Attitude Toward InsurancechuchuNo ratings yet

- 7 Ps of ICICIDocument8 pages7 Ps of ICICIshirishaggNo ratings yet

- Chap003 Solution Manual Financial Institutions Management A Risk Management ApproachDocument15 pagesChap003 Solution Manual Financial Institutions Management A Risk Management ApproachFami Famz100% (1)

- Introduction to Insurance Risk and PrinciplesDocument13 pagesIntroduction to Insurance Risk and PrinciplesAnupriya ChuriNo ratings yet

- F - UnderwritingDocument15 pagesF - UnderwritingRavid Villa Arya100% (5)

- Lagnajit Ayaskant Sahoo Gourab Biswas Suchismita Das Santanu Rath Ranjeet Kumar September, 2010Document23 pagesLagnajit Ayaskant Sahoo Gourab Biswas Suchismita Das Santanu Rath Ranjeet Kumar September, 2010Lagnajit Ayaskant SahooNo ratings yet

- Insurance Intermediaries Roles RegulationsDocument45 pagesInsurance Intermediaries Roles RegulationsGracy100% (1)

- Defining and Classifying RisksDocument29 pagesDefining and Classifying RisksRaj GanjooNo ratings yet

- Insurance: 1 Lesson 1 Introduction To InsuranceDocument14 pagesInsurance: 1 Lesson 1 Introduction To Insurancevipul sutharNo ratings yet

- Essentials of Life InsuranceDocument15 pagesEssentials of Life InsuranceAayush AgrawalNo ratings yet

- Fundamentals of Insurance Part 2Document10 pagesFundamentals of Insurance Part 2Rajendranath Behera0% (1)

- Chapter 1 - Risk and Its ManagementDocument6 pagesChapter 1 - Risk and Its ManagementAbeer AlSalem67% (3)

- A Report On: Customer Relationship Management of Idbi Federal Life InsuranceDocument95 pagesA Report On: Customer Relationship Management of Idbi Federal Life InsuranceamitNo ratings yet

- Iii Semester, Insurance and Risk Management ModuleDocument10 pagesIii Semester, Insurance and Risk Management ModuleSofi KhanNo ratings yet

- QUESTION BANK For Banking and Insurance MBA Sem IV-FinanceDocument2 pagesQUESTION BANK For Banking and Insurance MBA Sem IV-FinanceAgnya PatelNo ratings yet

- Price Attention and MemoryDocument14 pagesPrice Attention and MemoryMohamed LisaamNo ratings yet

- HDFC LifeDocument66 pagesHDFC LifeChetan PahwaNo ratings yet

- Role of Insurance in SocietyDocument3 pagesRole of Insurance in Societyatege linggi0% (2)

- Life and General InsuranceDocument28 pagesLife and General InsuranceAravinda ShettyNo ratings yet

- Role of Insurance in Economic DevelopmentDocument9 pagesRole of Insurance in Economic Developmentm_dattaias81% (16)

- Fire InsuranceDocument34 pagesFire InsuranceSaurav PandeyNo ratings yet

- Consumerism As An Emerging ForceDocument34 pagesConsumerism As An Emerging Forceevneet216736No ratings yet

- Market Efficiency PDFDocument17 pagesMarket Efficiency PDFBatoul ShokorNo ratings yet

- Insurance ProjDocument20 pagesInsurance ProjMahesh ParabNo ratings yet

- Insurance PrincipleDocument15 pagesInsurance Principlemanyasingh100% (1)

- Insurance Industry RM1Document62 pagesInsurance Industry RM1Raj Kumar RanganathanNo ratings yet

- Indian insurance industry history and changing faceDocument21 pagesIndian insurance industry history and changing facePradeep KumarNo ratings yet

- Presented By: Mr. Rashmi Ranjan PanigrahiDocument35 pagesPresented By: Mr. Rashmi Ranjan PanigrahiRashmi Ranjan PanigrahiNo ratings yet

- Life Insurance ProjectDocument73 pagesLife Insurance ProjectSanthosh SomaNo ratings yet

- P's of Marketing and Life Insurance IndustryDocument5 pagesP's of Marketing and Life Insurance IndustryatulbhushanNo ratings yet

- Risk Chapter 6Document27 pagesRisk Chapter 6Wonde BiruNo ratings yet

- Chapter 3 Marketing Mix of Life InsuranceDocument19 pagesChapter 3 Marketing Mix of Life Insurancerahulhaldankar0% (1)

- Customer Service and Customer Lifetime ValueDocument10 pagesCustomer Service and Customer Lifetime ValueTaher BalasinorwalaNo ratings yet

- Chapter 03 - Principles & Practice of Life InsuranceDocument21 pagesChapter 03 - Principles & Practice of Life InsuranceShubham GuptaNo ratings yet

- 0-Principles of Risk Management and Insurance-COURSE OUTLINEDocument14 pages0-Principles of Risk Management and Insurance-COURSE OUTLINEJ-Claude DougNo ratings yet

- Insurance IntermediariesDocument9 pagesInsurance IntermediariesarmailgmNo ratings yet

- Functions of InsuranceDocument8 pagesFunctions of InsuranceBasappaSarkarNo ratings yet

- Principles of Life InsuranceDocument63 pagesPrinciples of Life InsuranceKanishk GuptaNo ratings yet

- Industrial Management ModelDocument2 pagesIndustrial Management Modelrajendrakumar100% (1)

- Research On Life InsuranceDocument90 pagesResearch On Life InsuranceDhananjay SharmaNo ratings yet

- Insurance & Risk Management JUNE 2022Document11 pagesInsurance & Risk Management JUNE 2022Rajni KumariNo ratings yet

- Sickness in Small EnterprisesDocument15 pagesSickness in Small EnterprisesRajesh KumarNo ratings yet

- 7ps of International Marketing With Ref To Domestic & International MarketsDocument15 pages7ps of International Marketing With Ref To Domestic & International MarketsSimrat Singh Arora0% (2)

- Risks of Derivative Markets in BDDocument3 pagesRisks of Derivative Markets in BDAsadul AlamNo ratings yet

- Rnis College of Insurance: New Ic 33 - Model Test 4Document6 pagesRnis College of Insurance: New Ic 33 - Model Test 4Raj Kumar DepalliNo ratings yet

- Literature Review on Insurance Management AutomationDocument5 pagesLiterature Review on Insurance Management AutomationAncy KalungaNo ratings yet

- Marketing Mix of Idbi Bank Insurance CompanyDocument16 pagesMarketing Mix of Idbi Bank Insurance CompanydimanshuNo ratings yet

- Financial Management Assignment - Sem IIDocument11 pagesFinancial Management Assignment - Sem IIAkhilesh67% (3)

- Ic33 Print Out 660 English PDFDocument54 pagesIc33 Print Out 660 English PDFumesh100% (1)

- Element of CostDocument16 pagesElement of CostcwarekhaNo ratings yet

- Insurance Industry: Product ClassificationDocument16 pagesInsurance Industry: Product Classificationsadafkhan21No ratings yet

- Regulation of Insurance Business in IndiaDocument27 pagesRegulation of Insurance Business in IndiaRachamalla KrishnareddyNo ratings yet

- Social Insurance SyllabusDocument11 pagesSocial Insurance SyllabusrbugblatterNo ratings yet

- Chapter 1906Document29 pagesChapter 1906Fozia MehtabNo ratings yet

- Recruitment of Advisors For Bharti Axa Life InsuranceDocument63 pagesRecruitment of Advisors For Bharti Axa Life InsuranceMohit kolliNo ratings yet

- Insurance@8: Measurement of RiskDocument13 pagesInsurance@8: Measurement of RiskMD Rifat ZahirNo ratings yet

- Compare The Risks of (A) Fire With (B) Unemployment in Terms of How Well They Meet The Requirements of An Ideally Insurable RiskDocument4 pagesCompare The Risks of (A) Fire With (B) Unemployment in Terms of How Well They Meet The Requirements of An Ideally Insurable RiskEileen WongNo ratings yet

- Application of Probability TheoryDocument7 pagesApplication of Probability TheoryNikhil RanjanNo ratings yet

- Risk Management Procedure TemplateDocument39 pagesRisk Management Procedure Templatealexrferreira75% (4)

- Proposal No. PMTB112211795455: Motor Insurance - Proposal Form Cum Transcript Letter For Private Car PackageDocument2 pagesProposal No. PMTB112211795455: Motor Insurance - Proposal Form Cum Transcript Letter For Private Car Packagekrishna11143No ratings yet

- The Meyer Group - NORTH PAGE STORAGE MINI WAREHOUSE RENTAL AGREEMENTDocument2 pagesThe Meyer Group - NORTH PAGE STORAGE MINI WAREHOUSE RENTAL AGREEMENTrmeyer33No ratings yet

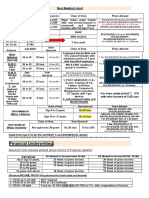

- Medical Chart LicDocument3 pagesMedical Chart LicBijay Krishna Chatterjee43% (7)

- Health and Saftey Ch. 10Document18 pagesHealth and Saftey Ch. 10Sarah AhmedNo ratings yet

- Exclusion & Limitation Clauses: Current Developments: James Carnie, Principal, Clendons - October 2011Document21 pagesExclusion & Limitation Clauses: Current Developments: James Carnie, Principal, Clendons - October 2011alph001No ratings yet

- (9final PreboardDocument7 pages(9final Preboardchowchow123100% (1)

- PensionDocument36 pagesPensionJp SwainNo ratings yet

- A191 GLUL 3093 Banking Law: Schedule 11 Financial Services Act 2013Document4 pagesA191 GLUL 3093 Banking Law: Schedule 11 Financial Services Act 2013neemNo ratings yet

- 2014 BigData Analytics Business Partner Case Studies 4-9-14Document59 pages2014 BigData Analytics Business Partner Case Studies 4-9-14Dario SimbañaNo ratings yet

- SBI+Life+-+Shubh+Nivesh V04 Policy+Document Form+595Document52 pagesSBI+Life+-+Shubh+Nivesh V04 Policy+Document Form+595ANIL TIWARINo ratings yet

- Chain of TitleDocument2 pagesChain of Titleklg_consultant8688No ratings yet

- La Clinica Career OpportunitiesDocument2 pagesLa Clinica Career OpportunitiesOffice on Latino Affairs (OLA)No ratings yet

- Financial Services Overview & Top Companies in IndiaDocument11 pagesFinancial Services Overview & Top Companies in IndiaAshwin ShettyNo ratings yet

- Muhammad Shadik Sastra Mubarak - 7311421379 - Analisis Laporan KeuanganDocument8 pagesMuhammad Shadik Sastra Mubarak - 7311421379 - Analisis Laporan KeuanganFuad Azmul FauziNo ratings yet

- US Internal Revenue Service: I1040 - 1999Document117 pagesUS Internal Revenue Service: I1040 - 1999IRSNo ratings yet

- Final English 2015 PCE PDFDocument192 pagesFinal English 2015 PCE PDFCheong Weng ChoyNo ratings yet

- Ar 13Document112 pagesAr 13ckiencrm_lvNo ratings yet

- Counterclaim in Property Dispute WithdrawnDocument182 pagesCounterclaim in Property Dispute WithdrawnthesacnewsNo ratings yet

- Jurisprudence 2015Document561 pagesJurisprudence 2015Euodia HodeshNo ratings yet

- Ayushman Bharat - KailashDocument11 pagesAyushman Bharat - KailashKailash NagarNo ratings yet

- COI FOR Mounce TransportationDocument2 pagesCOI FOR Mounce TransportationPintilei AlinNo ratings yet

- Abbreviations AllDocument21 pagesAbbreviations AllnanduNo ratings yet

- Finac 3 TopicsDocument9 pagesFinac 3 TopicsCielo Mae Parungo60% (5)

- 5-Rizal Surety Vs Manila RailroadDocument3 pages5-Rizal Surety Vs Manila RailroadJoan Dela CruzNo ratings yet

- Philippines labor ruling on 13th month pay appealDocument8 pagesPhilippines labor ruling on 13th month pay appealGerald HernandezNo ratings yet

- 3901 LN1Document3 pages3901 LN1Ayushmaan BhattacharjiNo ratings yet

- A Summer Training Project Report (Reliance Life Insurance)Document52 pagesA Summer Training Project Report (Reliance Life Insurance)Bhatzada Zahid Jameel100% (3)

- An Example of Accrued RevenueDocument5 pagesAn Example of Accrued RevenueBrian Reyes GangcaNo ratings yet

- As 4303-1995 (Reference Use Only) General Conditions of Subcontract For Design and ConstructDocument8 pagesAs 4303-1995 (Reference Use Only) General Conditions of Subcontract For Design and ConstructSAI Global - APACNo ratings yet