You might also like

- Bob Robotti - Navigating Deep WatersDocument35 pagesBob Robotti - Navigating Deep WatersCanadianValueNo ratings yet

- Amitabh Singhvi L MOI Interview L JUNE-2011Document6 pagesAmitabh Singhvi L MOI Interview L JUNE-2011Wayne GonsalvesNo ratings yet

- Scott Miller of Greenhaven Road Capital: Long On Zix CorpDocument0 pagesScott Miller of Greenhaven Road Capital: Long On Zix CorpcurrygoatNo ratings yet

- H. Kevin Byun's Q4 2013 Denali Investors LetterDocument4 pagesH. Kevin Byun's Q4 2013 Denali Investors LetterValueInvestingGuy100% (1)

- Summary of Bruce C. Greenwald, Judd Kahn & Paul D. Sonkin's Value InvestingFrom EverandSummary of Bruce C. Greenwald, Judd Kahn & Paul D. Sonkin's Value InvestingNo ratings yet

- The Dividend Imperative: How Dividends Can Narrow the Gap between Main Street and Wall StreetFrom EverandThe Dividend Imperative: How Dividends Can Narrow the Gap between Main Street and Wall StreetNo ratings yet

- AVM Ranger Returns 29.1% in 2016Document6 pagesAVM Ranger Returns 29.1% in 2016ChrisNo ratings yet

- Boyar's Intrinsic Value Research Forgotten FourtyDocument49 pagesBoyar's Intrinsic Value Research Forgotten FourtyValueWalk100% (1)

- Graham Doddsville Issue 33 v23Document46 pagesGraham Doddsville Issue 33 v23marketfolly.comNo ratings yet

- Be Your Own ActivistDocument11 pagesBe Your Own ActivistSwagdogNo ratings yet

- 2009 Annual LetterDocument5 pages2009 Annual Letterppate100% (1)

- The 400% Man: How A College Dropout at A Tiny Utah Fund Beat Wall Street, and Why Most Managers Are Scared To Copy HimDocument5 pagesThe 400% Man: How A College Dropout at A Tiny Utah Fund Beat Wall Street, and Why Most Managers Are Scared To Copy Himrakeshmoney99No ratings yet

- 8th Annual New York: Value Investing CongressDocument46 pages8th Annual New York: Value Investing CongressVALUEWALK LLCNo ratings yet

- Lisa Rapuano Finding Your Way Along The Many Paths of ValueDocument29 pagesLisa Rapuano Finding Your Way Along The Many Paths of ValueValueWalk100% (1)

- Hillhouse-Zhang-Value Investing Congress West 2010Document24 pagesHillhouse-Zhang-Value Investing Congress West 2010jackefellerNo ratings yet

- Thomas Russo: Global Value Investing - Richard Ivey School of Business, 2013Document34 pagesThomas Russo: Global Value Investing - Richard Ivey School of Business, 2013Hedge Fund ConversationsNo ratings yet

- Chuck Akre Value Investing Conference Talk - 'An Investor's Odyssey - The Search For Outstanding Investments' PDFDocument10 pagesChuck Akre Value Investing Conference Talk - 'An Investor's Odyssey - The Search For Outstanding Investments' PDFSunil ParikhNo ratings yet

- Morgan Stanley - ROICDocument44 pagesMorgan Stanley - ROICGaurav AhirkarNo ratings yet

- Graham Doddsville Issue 24Document61 pagesGraham Doddsville Issue 24CanadianValueNo ratings yet

- Graham and Doddsville - Issue 9 - Spring 2010Document33 pagesGraham and Doddsville - Issue 9 - Spring 2010g4nz0No ratings yet

- Aquamarine Fund PresentationDocument25 pagesAquamarine Fund PresentationVijay MalikNo ratings yet

- Ghazi ValueInvestingCongress 100112Document70 pagesGhazi ValueInvestingCongress 100112VALUEWALK LLC100% (1)

- On Streaks: Perception, Probability, and SkillDocument5 pagesOn Streaks: Perception, Probability, and Skilljohnwang_174817No ratings yet

- Mauboussin - Does The M&a Boom Mean Anything For The MarketDocument6 pagesMauboussin - Does The M&a Boom Mean Anything For The MarketRob72081No ratings yet

- Public To Private Equity in The United States: A Long-Term LookDocument82 pagesPublic To Private Equity in The United States: A Long-Term LookYog MehtaNo ratings yet

- Office Hours With Warren Buffett May 2013Document11 pagesOffice Hours With Warren Buffett May 2013jkusnan3341No ratings yet

- Allan Mecham Interview PDFDocument6 pagesAllan Mecham Interview PDFRajeev BahugunaNo ratings yet

- Hayman Bass 20081017Document3 pagesHayman Bass 20081017dylan555100% (1)

- 10 Years PAt Dorsy PDFDocument32 pages10 Years PAt Dorsy PDFGurjeevNo ratings yet

- Klarman Yield PigDocument2 pagesKlarman Yield Pigalexg6No ratings yet

- Ubben ValueInvestingCongress 100212Document27 pagesUbben ValueInvestingCongress 100212VALUEWALK LLC100% (1)

- Aquamarine - 2013Document84 pagesAquamarine - 2013sb86No ratings yet

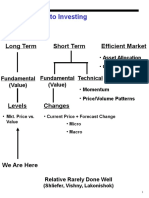

- Approaches To Investing: Long Term Short Term Efficient MarketDocument71 pagesApproaches To Investing: Long Term Short Term Efficient MarketPeter WarmeNo ratings yet

- Buffett On ValuationDocument7 pagesBuffett On ValuationAyush AggarwalNo ratings yet

- Clear Thinking About Share RepurchaseDocument29 pagesClear Thinking About Share RepurchaseVrtpy CiurbanNo ratings yet

- Max Heine Forbes March 29 1982Document2 pagesMax Heine Forbes March 29 1982jkusnan3341100% (2)

- Mick McGuire Value Investing Congress Presentation Marcato Capital ManagementDocument70 pagesMick McGuire Value Investing Congress Presentation Marcato Capital Managementmarketfolly.comNo ratings yet

- Arlington Value's 2013 LetterDocument7 pagesArlington Value's 2013 LetterValueWalk100% (7)

- Biggest mistakes in value investing and lessons learnedDocument9 pagesBiggest mistakes in value investing and lessons learnedPook Kei JinNo ratings yet

- Bankruptcy BasicsDocument106 pagesBankruptcy Basicsvaruntalukdar0% (1)

- The Incredible Shrinking Universe of StocksDocument29 pagesThe Incredible Shrinking Universe of StocksErsin Seçkin100% (1)

- Murray Stahl Discusses Value Investing Approach and Top Stock IdeasDocument10 pagesMurray Stahl Discusses Value Investing Approach and Top Stock IdeaskdwcapitalNo ratings yet

- Baupost Group outlines value-focused thrift stock analysisDocument11 pagesBaupost Group outlines value-focused thrift stock analysisDavid Collon100% (1)

- Graham - Doddsville - Issue 40 - v19 PDFDocument61 pagesGraham - Doddsville - Issue 40 - v19 PDFRofiq 4 NugrohoNo ratings yet

- Austrian Economics & InvestingDocument20 pagesAustrian Economics & InvestingRaj KumarNo ratings yet

- TTS - LBO PrimerDocument5 pagesTTS - LBO PrimerKrystleNo ratings yet

- Elliott Management's BMC PresentationDocument36 pagesElliott Management's BMC PresentationDealBookNo ratings yet

- Corvex Management 2014 Robin Hood Investment Conference PresentationDocument42 pagesCorvex Management 2014 Robin Hood Investment Conference PresentationValueWalk100% (1)

- Economic Returns, Reversion To The Mean, and Total Shareholder Returns Anticipating Change Is Hard But ProfitableDocument15 pagesEconomic Returns, Reversion To The Mean, and Total Shareholder Returns Anticipating Change Is Hard But ProfitableAhmed MadhaNo ratings yet

- Creating Value Thru Best-In-class Capital AllocationDocument16 pagesCreating Value Thru Best-In-class Capital Allocationiltdf100% (1)

- Private Equity Unchained: Strategy Insights for the Institutional InvestorFrom EverandPrivate Equity Unchained: Strategy Insights for the Institutional InvestorNo ratings yet

- The Art of Vulture Investing: Adventures in Distressed Securities ManagementFrom EverandThe Art of Vulture Investing: Adventures in Distressed Securities ManagementNo ratings yet

- Financial Fine Print: Uncovering a Company's True ValueFrom EverandFinancial Fine Print: Uncovering a Company's True ValueRating: 3 out of 5 stars3/5 (3)

- Wall Street Research: Past, Present, and FutureFrom EverandWall Street Research: Past, Present, and FutureRating: 3 out of 5 stars3/5 (2)

- Distressed Investment Banking - To the Abyss and Back - Second EditionFrom EverandDistressed Investment Banking - To the Abyss and Back - Second EditionNo ratings yet

- Behind the Curve: An Analysis of the Investment Behavior of Private Equity FundsFrom EverandBehind the Curve: An Analysis of the Investment Behavior of Private Equity FundsNo ratings yet

- Asian Financial Statement Analysis: Detecting Financial IrregularitiesFrom EverandAsian Financial Statement Analysis: Detecting Financial IrregularitiesNo ratings yet

- The Value Proposition: Sionna's Common Sense Path to Investment SuccessFrom EverandThe Value Proposition: Sionna's Common Sense Path to Investment SuccessNo ratings yet

- Ubben ValueInvestingCongress 100212Document27 pagesUbben ValueInvestingCongress 100212VALUEWALK LLC100% (1)

- Third Point Q3 2012 Investor Letter TPOIDocument11 pagesThird Point Q3 2012 Investor Letter TPOIVALUEWALK LLCNo ratings yet

- 8th Annual New York: Value Investing CongressDocument51 pages8th Annual New York: Value Investing CongressVALUEWALK LLCNo ratings yet

- Ghazi ValueInvestingCongress 100112Document70 pagesGhazi ValueInvestingCongress 100112VALUEWALK LLC100% (1)

- TAF 3Q 2012 Report and Shareholder LettersDocument77 pagesTAF 3Q 2012 Report and Shareholder LettersVALUEWALK LLCNo ratings yet

- Buckley ValueInvestingCongress 100112Document45 pagesBuckley ValueInvestingCongress 100112VALUEWALK LLCNo ratings yet

- Mauldin ValueInvestingCongress 100112Document11 pagesMauldin ValueInvestingCongress 100112VALUEWALK LLCNo ratings yet

- 8th Annual New York: Value Investing CongressDocument46 pages8th Annual New York: Value Investing CongressVALUEWALK LLCNo ratings yet

- The Best of Charlie Munger 1994 2011Document349 pagesThe Best of Charlie Munger 1994 2011VALUEWALK LLC100% (6)

- Value Investing Congress Presentation-Tilson-10!1!12Document93 pagesValue Investing Congress Presentation-Tilson-10!1!12VALUEWALK LLCNo ratings yet

- Rockstone Research VDR1 EnglishDocument28 pagesRockstone Research VDR1 EnglishVALUEWALK LLC100% (1)

- SHLDDocument18 pagesSHLDduwe7809100% (1)

- McGuire ValueInvestingCongress 100112Document70 pagesMcGuire ValueInvestingCongress 100112VALUEWALK LLCNo ratings yet

- Rosenstein ValueInvestingCongress 100112Document42 pagesRosenstein ValueInvestingCongress 100112VALUEWALK LLCNo ratings yet

- Roepers ValueInvestingCongress 100212Document30 pagesRoepers ValueInvestingCongress 100212VALUEWALK LLCNo ratings yet

- Green Mountain Coffee Roasters' Q2 and Q3 2011 Net Sales Figures Look Odd and Why It MattersDocument8 pagesGreen Mountain Coffee Roasters' Q2 and Q3 2011 Net Sales Figures Look Odd and Why It MattersmistervigilanteNo ratings yet

- 2012 Third Point Q2 Investor Letter TPOIDocument7 pages2012 Third Point Q2 Investor Letter TPOIVALUEWALK LLC100% (1)

- Rockstone Research URS1 EnglishDocument32 pagesRockstone Research URS1 EnglishVALUEWALK LLC100% (1)

- 2012 Third Point Q2 Investor Letter TPOIDocument7 pages2012 Third Point Q2 Investor Letter TPOIVALUEWALK LLC100% (1)

- T2 Accredited Fund Letter To Investors June 12Document10 pagesT2 Accredited Fund Letter To Investors June 12VALUEWALK LLCNo ratings yet

- Greenlight Q2 Letter To InvestorsDocument5 pagesGreenlight Q2 Letter To InvestorsVALUEWALK LLCNo ratings yet

- Buffett in Beijing Report JuneDocument15 pagesBuffett in Beijing Report JuneVALUEWALK LLCNo ratings yet

- MW Edu 07182012Document97 pagesMW Edu 07182012VALUEWALK LLCNo ratings yet

- HP PresentationDocument69 pagesHP Presentationssc320No ratings yet

- Dan Loeb Hedge Fund Letter June 2012Document2 pagesDan Loeb Hedge Fund Letter June 2012VALUEWALK LLCNo ratings yet

- GMCR Profits Overstated or MisunderstoodDocument8 pagesGMCR Profits Overstated or MisunderstoodVALUEWALK LLCNo ratings yet

- Fairholme: Ignore The CrowdDocument13 pagesFairholme: Ignore The CrowdVALUEWALK LLCNo ratings yet

- Fairholme: Ignore The CrowdDocument13 pagesFairholme: Ignore The CrowdVALUEWALK LLCNo ratings yet

- Mauboussinonstrategy - Sharerepurchasefromallangles June 2012Document15 pagesMauboussinonstrategy - Sharerepurchasefromallangles June 2012zeebugNo ratings yet

- Beginners Guide To Sketching Chapter 06Document30 pagesBeginners Guide To Sketching Chapter 06renzo alfaroNo ratings yet

- General Session PresentationsDocument2 pagesGeneral Session PresentationsKrishna Kanaiya DasNo ratings yet

- Quiz Template: © WWW - Teachitscience.co - Uk 2017 28644 1Document49 pagesQuiz Template: © WWW - Teachitscience.co - Uk 2017 28644 1Paul MurrayNo ratings yet

- KnowThem PPT FDocument18 pagesKnowThem PPT FAANANDHINI SNo ratings yet

- Do Not Go GentleDocument5 pagesDo Not Go Gentlealmeidaai820% (1)

- Designing Organizational Structure: Specialization and CoordinationDocument30 pagesDesigning Organizational Structure: Specialization and CoordinationUtkuNo ratings yet

- Skripsi Tanpa Bab Pembahasan PDFDocument117 pagesSkripsi Tanpa Bab Pembahasan PDFArdi Dwi PutraNo ratings yet

- The United Republic of Tanzania National Examinations Council of Tanzania Certificate of Secondary Education Examination 022 English LanguageDocument5 pagesThe United Republic of Tanzania National Examinations Council of Tanzania Certificate of Secondary Education Examination 022 English LanguageAndengenie ThomasNo ratings yet

- Crisostomo Et Al. v. Atty. Nazareno, A.C. No. 6677, June 10, 2014Document6 pagesCrisostomo Et Al. v. Atty. Nazareno, A.C. No. 6677, June 10, 2014Pamela TambaloNo ratings yet

- Learn Microscope Parts & Functions Under 40x MagnificationDocument3 pagesLearn Microscope Parts & Functions Under 40x Magnificationjaze025100% (1)

- PV LITERATURE ROUGHDocument11 pagesPV LITERATURE ROUGHraghudeepaNo ratings yet

- TASSEOGRAPHY - Your Future in A Coffee CupDocument5 pagesTASSEOGRAPHY - Your Future in A Coffee Cupcharles walkerNo ratings yet

- AI technologies improve HR analysisDocument4 pagesAI technologies improve HR analysisAtif KhanNo ratings yet

- Static and Dynamic ModelsDocument6 pagesStatic and Dynamic ModelsNadiya Mushtaq100% (1)

- Sharpe RatioDocument7 pagesSharpe RatioSindhuja PalanichamyNo ratings yet

- Cultural Identity and Diaspora in Jhumpa Lahiri's The NamesakeDocument10 pagesCultural Identity and Diaspora in Jhumpa Lahiri's The NamesakeOlivia DennisNo ratings yet

- Workshop 3-6: RCS of A Cube: Introduction To ANSYS HFSSDocument11 pagesWorkshop 3-6: RCS of A Cube: Introduction To ANSYS HFSSRicardo MichelinNo ratings yet

- Mab, Boy, Son), Used in Patronymics See AlsoDocument46 pagesMab, Boy, Son), Used in Patronymics See AlsoEilise IrelandNo ratings yet

- The Curse of MillhavenDocument2 pagesThe Curse of MillhavenstipemogwaiNo ratings yet

- Analogy and LogicDocument2 pagesAnalogy and LogicCOMELEC CARNo ratings yet

- Pathfit 1Document2 pagesPathfit 1Brian AnggotNo ratings yet

- POM Q1 Week 3 PDFDocument10 pagesPOM Q1 Week 3 PDFMary Ann Isanan60% (5)

- Task 2 AmberjordanDocument15 pagesTask 2 Amberjordanapi-200086677100% (2)

- Drama GuidelinesDocument120 pagesDrama GuidelinesAnonymous SmtsMiad100% (3)

- I. Objectives: Checking of AttendanceDocument4 pagesI. Objectives: Checking of AttendanceJoAnn MacalingaNo ratings yet

- Bai Tap LonDocument10 pagesBai Tap LonMyNguyenNo ratings yet

- Women's Health: HysterectomyDocument7 pagesWomen's Health: HysterectomySuci RahmayeniNo ratings yet

- Chapter 17. Bothriocephalus Acheilognathi Yamaguti, 1934: December 2012Document16 pagesChapter 17. Bothriocephalus Acheilognathi Yamaguti, 1934: December 2012Igor YuskivNo ratings yet

- Article 9 of Japan ConstitutionDocument32 pagesArticle 9 of Japan ConstitutionRedNo ratings yet

- Sa Tally Education BrochureDocument6 pagesSa Tally Education BrochurePoojaMittalNo ratings yet