You might also like

- General Foods Capital Budgeting AnalysisDocument5 pagesGeneral Foods Capital Budgeting Analysisgpadhye123No ratings yet

- Solman 12 Second EdDocument23 pagesSolman 12 Second Edferozesheriff50% (2)

- Cash Flow StatementDocument4 pagesCash Flow StatementRavina Singh100% (1)

- CAMELBACK COMMUNICATIONS REVAMPS COSTING SYSTEMDocument23 pagesCAMELBACK COMMUNICATIONS REVAMPS COSTING SYSTEMVidya Sagar Ch100% (2)

- Rougir Cosmetics International Did Not Have Internal Capacity To Meet DemandDocument3 pagesRougir Cosmetics International Did Not Have Internal Capacity To Meet DemandSameed Zaheer Khan100% (1)

- Financial Accounting and Reporting: The Game of Financial RatiosDocument8 pagesFinancial Accounting and Reporting: The Game of Financial RatiosANANTHA BHAIRAVI MNo ratings yet

- © Mrityunjay Tiwary Unauthorised Circulation/upload/download Strictly ProhibitedDocument12 pages© Mrityunjay Tiwary Unauthorised Circulation/upload/download Strictly ProhibitedsumitNo ratings yet

- Chapter 7Document19 pagesChapter 7Arun Kumar SatapathyNo ratings yet

- Cochin MarineDocument4 pagesCochin MarineSivasaravanan A TNo ratings yet

- Camelback CommunicationsDocument9 pagesCamelback Communicationsvir1672100% (1)

- Decision Sheet P&GDocument2 pagesDecision Sheet P&GApurv Toppo100% (2)

- Operations Management-II End Term Paper 2020 IIM IndoreDocument14 pagesOperations Management-II End Term Paper 2020 IIM IndoreRAMAJ BESHRA PGP 2020 Batch100% (2)

- Pioma Plastics Cash Flow Statement Year Ended July 31Document4 pagesPioma Plastics Cash Flow Statement Year Ended July 31Prajwal PaiNo ratings yet

- Planning The Product Mix at Panchtantra CorporationDocument14 pagesPlanning The Product Mix at Panchtantra CorporationNRLDCNo ratings yet

- Quality Management QP EPGP 13Document5 pagesQuality Management QP EPGP 13Saket ShankarNo ratings yet

- Case Analysis Operations Research Red Brand Canners (Download To View Full Presentation)Document12 pagesCase Analysis Operations Research Red Brand Canners (Download To View Full Presentation)mahtaabk83% (12)

- Varun Nagar Cooperative Society: (Document Subtitle)Document9 pagesVarun Nagar Cooperative Society: (Document Subtitle)Vedansh DubeyNo ratings yet

- Modern Pharma SolnDocument3 pagesModern Pharma SolnSakshiNo ratings yet

- Banyan HouseDocument8 pagesBanyan HouseNimit ShahNo ratings yet

- Indian Electricals Weighs Accepting Trial Order for Vending MachinesDocument8 pagesIndian Electricals Weighs Accepting Trial Order for Vending MachinesJoseph MathewNo ratings yet

- Mini CaseDocument13 pagesMini CaseVaibhav Goyal0% (1)

- OPTIMIZING HEALTHCARE STAFFINGDocument53 pagesOPTIMIZING HEALTHCARE STAFFINGPriyesh Wankhede50% (2)

- Managerial Accounting - Hallstead Jewelers CaseDocument2 pagesManagerial Accounting - Hallstead Jewelers Casesxzhou23100% (1)

- Cci CaseDocument3 pagesCci CaseDanielle Eller BurnettNo ratings yet

- 15.963 Managerial Accounting at MITDocument11 pages15.963 Managerial Accounting at MITabhishekbehal50120% (1)

- Airline Cost and Revenue Comparison: Delta, Southwest, JetBlueDocument7 pagesAirline Cost and Revenue Comparison: Delta, Southwest, JetBlueKumar AbhishekNo ratings yet

- 14 Additional Solved Problems 13Document17 pages14 Additional Solved Problems 13PIYUSH CHANDRAVANSHINo ratings yet

- Camelback Management AccountingDocument4 pagesCamelback Management Accountingnitinr18No ratings yet

- Case-American Connector CompanyDocument9 pagesCase-American Connector CompanyDIVYAM BHADORIANo ratings yet

- Interest (1 - (1+r) - N/R) + PV of The Principal AmountDocument2 pagesInterest (1 - (1+r) - N/R) + PV of The Principal AmountBellapu Durga vara prasadNo ratings yet

- Ford Auto CollectionDocument10 pagesFord Auto Collectionkarishma_sehgal50% (4)

- CMA Individual assignment analysis of costing methods and product profitabilityDocument6 pagesCMA Individual assignment analysis of costing methods and product profitabilityCH NAIRNo ratings yet

- Mphasis - ALP Case Study 2 PDFDocument4 pagesMphasis - ALP Case Study 2 PDFshivamchughNo ratings yet

- A Study On Non Traditional Channels of B Natural Juices in Retail MarketDocument54 pagesA Study On Non Traditional Channels of B Natural Juices in Retail Marketakhil sai100% (1)

- Merton Truck Company Analysis OptimizationDocument11 pagesMerton Truck Company Analysis Optimizationkrishna sharmaNo ratings yet

- DHL Global Forwarding Consolidation Program - Group Assignment Case AnalysisDocument13 pagesDHL Global Forwarding Consolidation Program - Group Assignment Case AnalysisNitin Shankar100% (1)

- Star Engineering CompanyDocument5 pagesStar Engineering CompanyMarilou GabayaNo ratings yet

- Market Analysis of Nimyle: by Anandu P ShajiDocument13 pagesMarket Analysis of Nimyle: by Anandu P ShajiDaily Journal100% (1)

- PGP/24/097 Paras Mavani: Indian Institute of Management Kozhikode, Post Graduate Programme PGP 24 - Section BDocument10 pagesPGP/24/097 Paras Mavani: Indian Institute of Management Kozhikode, Post Graduate Programme PGP 24 - Section BParas Mavani100% (1)

- Business CaseDocument4 pagesBusiness CaseJoseph GonzalesNo ratings yet

- Problem Set 2Document2 pagesProblem Set 2nskabra0% (1)

- MacDocument4 pagesMacalwar_shi262068100% (1)

- End Point Model CaseDocument8 pagesEnd Point Model CaseSAURAV KUMAR GUPTANo ratings yet

- Merton Truck Company CaseDocument22 pagesMerton Truck Company CaseSubharthi Sen100% (1)

- Boardroom GameDocument12 pagesBoardroom GameShivam SomaniNo ratings yet

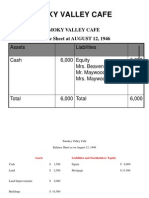

- Smokey Valley Cafe Balance Sheets 1946Document3 pagesSmokey Valley Cafe Balance Sheets 1946mohit_namanNo ratings yet

- Coffee Wars: CCD vs Starbucks in IndiaDocument3 pagesCoffee Wars: CCD vs Starbucks in IndiaSreeda PerikamanaNo ratings yet

- Problem Set 2Document2 pagesProblem Set 2Rithesh KNo ratings yet

- S4 - 7 - Merton Truck Case StudyDocument4 pagesS4 - 7 - Merton Truck Case StudyBikram Satapathy100% (2)

- SecA Group4 CISCO OBDocument17 pagesSecA Group4 CISCO OBAnimesh KumarNo ratings yet

- Had On The $158,000 Profit of First Six Months of 2004? AnswerDocument3 pagesHad On The $158,000 Profit of First Six Months of 2004? AnswerRamalu Dinesh ReddyNo ratings yet

- Meddeal Private Limited: Putting A Price Tag For The BusinessDocument20 pagesMeddeal Private Limited: Putting A Price Tag For The BusinessShivani SinghNo ratings yet

- Macro OB Case QuestionsDocument4 pagesMacro OB Case Questionsrock sinhaNo ratings yet

- TWA grp8Document10 pagesTWA grp8Aryan Anand100% (1)

- 202E10Document33 pages202E10Ashish BhallaNo ratings yet

- Question Bank Test 1Document12 pagesQuestion Bank Test 1bolai.lethabo19No ratings yet

- Process Costing 1Document32 pagesProcess Costing 1errNo ratings yet

- Natural Blends IncDocument21 pagesNatural Blends IncKanishk Shah50% (2)

- Joint Cost Allocation Using Net Realizable Value MethodDocument3 pagesJoint Cost Allocation Using Net Realizable Value Methodkarthikdora_007No ratings yet

- Capital Budgeting 2Document4 pagesCapital Budgeting 2rebecabeczNo ratings yet

- LIME 5 Case Study Gold GymDocument5 pagesLIME 5 Case Study Gold GymUdit VarshneyNo ratings yet

- What Makes Great Boards Great Boards GreatDocument6 pagesWhat Makes Great Boards Great Boards GreatUdit VarshneyNo ratings yet

- India's Food Processing IndustryDocument29 pagesIndia's Food Processing IndustryUdit VarshneyNo ratings yet

- FRA Quiz 2 SolnxDocument3 pagesFRA Quiz 2 SolnxUdit VarshneyNo ratings yet

- IEL Case Study Part 2Document1 pageIEL Case Study Part 2Udit VarshneyNo ratings yet

- Agri ResearchDocument124 pagesAgri ResearchUdit VarshneyNo ratings yet

- Group 9Document8 pagesGroup 9Udit VarshneyNo ratings yet

- Case Study: RajnigandhaDocument10 pagesCase Study: RajnigandhaUdit Varshney0% (1)

- financial accounting definitionsDocument6 pagesfinancial accounting definitionskingkhan009No ratings yet

- Forecasting RevenueDocument55 pagesForecasting RevenueHyacinth Alban100% (2)

- FARAP-4403 (Inventories)Document14 pagesFARAP-4403 (Inventories)Dizon Ropalito P.No ratings yet

- Cell Phone Shop FinalDocument26 pagesCell Phone Shop Finalapi-249675528No ratings yet

- PAYROLL PROBLEM SOLUTIONDocument39 pagesPAYROLL PROBLEM SOLUTIONHazel Joy UgatesNo ratings yet

- Chapter 17Document32 pagesChapter 17Ly Nguyễn Thị TuyếtNo ratings yet

- Proj CostDocument64 pagesProj CostCarlisle ChuaNo ratings yet

- Colorpak Indonesia - Bilingual - 31 - Des - 19Document76 pagesColorpak Indonesia - Bilingual - 31 - Des - 19Jefri Formen PangaribuanNo ratings yet

- Management AccountingDocument223 pagesManagement Accountingcyrus100% (2)

- RTP June 19 QnsDocument15 pagesRTP June 19 QnsbinuNo ratings yet

- Home Office and Branch Accounting ProblemsDocument9 pagesHome Office and Branch Accounting ProblemsMichaela QuimsonNo ratings yet

- Presentation On Recycling of PlasticDocument22 pagesPresentation On Recycling of PlasticTushar YadavNo ratings yet

- Bharti Airtel Capital Structure and Financing AnalysisDocument11 pagesBharti Airtel Capital Structure and Financing AnalysisDavid WilliamNo ratings yet

- Processing Transactions: by Prof Sameer LakhaniDocument83 pagesProcessing Transactions: by Prof Sameer LakhaniBhagyashree JadhavNo ratings yet

- Measuring of Assets RuswandyDocument5 pagesMeasuring of Assets RuswandyDillart SpaceNo ratings yet

- Cost and Management AccountingDocument6 pagesCost and Management AccountingAli HaiderNo ratings yet

- Accruals & PrepaymentsDocument5 pagesAccruals & PrepaymentsClouds consultantsNo ratings yet

- Research Report On: Cash Flow Statement Analysis of Reliance Industries LimitedDocument112 pagesResearch Report On: Cash Flow Statement Analysis of Reliance Industries Limitedpan cardNo ratings yet

- Tire City ExhibitsDocument7 pagesTire City ExhibitsAyushi GuptaNo ratings yet

- 66653bos53803 cp10Document81 pages66653bos53803 cp10TECH TeluguNo ratings yet

- Mi GTM 4Q20 PDFDocument79 pagesMi GTM 4Q20 PDFMoneycomeNo ratings yet

- ResultsDocument16 pagesResultsURVASHINo ratings yet

- Financial Statement Analysis FrameworkDocument7 pagesFinancial Statement Analysis FrameworkmkhanmajlisNo ratings yet

- Business Combination 4Document2 pagesBusiness Combination 4Jamie RamosNo ratings yet

- A.Income Statement: Pre-Operation Year 1Document5 pagesA.Income Statement: Pre-Operation Year 1Benjie MariNo ratings yet

- AFAR H01 Cost Accounting PDFDocument7 pagesAFAR H01 Cost Accounting PDFhellokittysaranghaeNo ratings yet

- Financial statement analysis ratiosDocument1 pageFinancial statement analysis ratiosprince100% (1)

- Accounting in Action 12eDocument65 pagesAccounting in Action 12eMd Shawfiqul Islam0% (1)

- B326 TMA 23-24 (Fall) V1Document9 pagesB326 TMA 23-24 (Fall) V1Reham Abdelaziz100% (2)

- Bec 225 AssignmentDocument4 pagesBec 225 Assignmentstanely ndlovuNo ratings yet