You might also like

- DDocument1 pageDabracadabra33No ratings yet

- LIFE INSURANCE CHECKLIST TERMSDocument3 pagesLIFE INSURANCE CHECKLIST TERMSabracadabra33No ratings yet

- LIFE INSURANCE CHECKLIST TERMSDocument3 pagesLIFE INSURANCE CHECKLIST TERMSabracadabra33No ratings yet

- 2011-12-23 QE Subscriber LetterDocument7 pages2011-12-23 QE Subscriber Letterabracadabra33No ratings yet

- A 23Document4 pagesA 23abracadabra33No ratings yet

- DDocument1 pageDabracadabra33No ratings yet

- Essential property and auto insurance terms explainedDocument3 pagesEssential property and auto insurance terms explainedabracadabra33No ratings yet

- DDocument1 pageDabracadabra33No ratings yet

- DDocument1 pageDabracadabra33No ratings yet

- A 23Document4 pagesA 23abracadabra33No ratings yet

- DDocument1 pageDabracadabra33No ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5782)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (890)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (72)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Basic Mortgage ConceptsDocument5 pagesBasic Mortgage Conceptsmdal10No ratings yet

- Kings County Lawsuit Against Citigroup and AffiliatesDocument423 pagesKings County Lawsuit Against Citigroup and AffiliatesDavid B. StarkeyNo ratings yet

- Student Loan Repayment Program Service AgreementDocument2 pagesStudent Loan Repayment Program Service AgreementDawn RallosNo ratings yet

- Conformity on new housing loan cross-default policyDocument1 pageConformity on new housing loan cross-default policyjonathan magdatoNo ratings yet

- Example Pooling and Servicing Agreement PDFDocument2 pagesExample Pooling and Servicing Agreement PDFTrentonNo ratings yet

- You Exec - Ultimate Loan FreeDocument174 pagesYou Exec - Ultimate Loan FreeVíctor Hugo TeránNo ratings yet

- Chapter 09: Mortgage Markets: Page 1Document19 pagesChapter 09: Mortgage Markets: Page 1AS SANo ratings yet

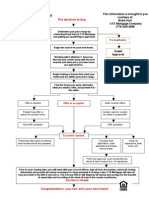

- Home Buying Process Flow ChartDocument1 pageHome Buying Process Flow ChartNevadaHomes100% (5)

- 20-Hour MLO Course OutlineDocument34 pages20-Hour MLO Course OutlinethemufiNo ratings yet

- Mapi Lending Investors Inc.: Member Loan Ledger UnitDocument2 pagesMapi Lending Investors Inc.: Member Loan Ledger UnitMhine MhineNo ratings yet

- Housing Loan GuidelinesDocument10 pagesHousing Loan GuidelinesDon DineroNo ratings yet

- Economic Crisis 2008Document31 pagesEconomic Crisis 2008Enio E. DokaNo ratings yet

- SECURITISATIONDocument40 pagesSECURITISATIONHARSHA SHENOYNo ratings yet

- Essential Requisites of Contracts of Pledge, Real Estate Mortgage and Chattel MortgageDocument6 pagesEssential Requisites of Contracts of Pledge, Real Estate Mortgage and Chattel MortgageGlen Mervin EsguerraNo ratings yet

- Court CaseDocument62 pagesCourt CaseKenneth SandersNo ratings yet

- Tutorial 1 Time Value of Money PDFDocument2 pagesTutorial 1 Time Value of Money PDFLâm TÚc NgânNo ratings yet

- Hurricane Katrina Telephone Numbers To Contact LendersDocument4 pagesHurricane Katrina Telephone Numbers To Contact LendersamericanaNo ratings yet

- Loan Calculator1Document9 pagesLoan Calculator1Md Jakir HossainNo ratings yet

- Revised Guidelines Implementing The Pag-IBIG Fund HRRL ProgramDocument11 pagesRevised Guidelines Implementing The Pag-IBIG Fund HRRL ProgramRaine Buenaventura-EleazarNo ratings yet

- Loan Pay CalculatorDocument6 pagesLoan Pay CalculatorHRITHIK CHOUKSENo ratings yet

- Badcreditloans Review HTMLDocument8 pagesBadcreditloans Review HTMLmakemoneyonlinebrosNo ratings yet

- TVR Format - Shrikrushn Namdev Kavar - TF4343554Document19 pagesTVR Format - Shrikrushn Namdev Kavar - TF4343554Nikhil MohaneNo ratings yet

- EMI CalculatorDocument7 pagesEMI Calculatorarunasagar_2011No ratings yet

- Practice Multiple Choice Test 6Document10 pagesPractice Multiple Choice Test 6api-3834751No ratings yet

- HSC Past Paper Questions 2u Maths - Time Payments 1Document1 pageHSC Past Paper Questions 2u Maths - Time Payments 1greycouncilNo ratings yet

- RFBT 3- Law on Credit Transactions Post-Test ReviewDocument5 pagesRFBT 3- Law on Credit Transactions Post-Test ReviewCharles D. FloresNo ratings yet

- Subprime Mortgage CrisisDocument35 pagesSubprime Mortgage CrisisVineet GuptaNo ratings yet

- Rising Interest RatesDocument4 pagesRising Interest RatesRAJESH BHANDERINo ratings yet

- Loss Mitigation FlyerDocument2 pagesLoss Mitigation FlyerreomarketingNo ratings yet

- Overview & Principles of Credit Management by Prof. Divya GuptaDocument28 pagesOverview & Principles of Credit Management by Prof. Divya GuptaArun SinghNo ratings yet