You might also like

- Ratio Analysis - APDocument31 pagesRatio Analysis - APPrachi SinghNo ratings yet

- Ratio Analysis GuideDocument1 pageRatio Analysis GuideUltras SevenNo ratings yet

- Fsa - Ratios AnalysisDocument8 pagesFsa - Ratios AnalysiscugutsNo ratings yet

- Lecture 10 Create Financial PlanDocument42 pagesLecture 10 Create Financial Planmoizlaghari71No ratings yet

- Financial Statement AnalysisDocument55 pagesFinancial Statement AnalysisPravin UntooNo ratings yet

- Session 24Document40 pagesSession 24Ashutosh GuptaNo ratings yet

- Ratios Revision Unit 4 1 2 1Document33 pagesRatios Revision Unit 4 1 2 1api-679810879No ratings yet

- Financial: AnalysisDocument55 pagesFinancial: AnalysisJennelyn MercadoNo ratings yet

- Ratio AnalysisDocument65 pagesRatio AnalysisAakash ChhariaNo ratings yet

- Lecture 1. Ratio Analysis Financial AppraisalDocument11 pagesLecture 1. Ratio Analysis Financial AppraisaltiiworksNo ratings yet

- RatiosDocument23 pagesRatiosUsman gNo ratings yet

- Topic 9 (Part 1) SolutionsDocument8 pagesTopic 9 (Part 1) SolutionsLiang BochengNo ratings yet

- Financial Statement Analysis: by Aditi RodeDocument36 pagesFinancial Statement Analysis: by Aditi RodegrshneheteNo ratings yet

- Dupont MethodDocument4 pagesDupont MethodgitzNo ratings yet

- Financial Accounting TermsDocument2 pagesFinancial Accounting TermsNaman AgarwalNo ratings yet

- RATIO ANALYSIS FOR ALWADI INTERNATIONAL SCHOOL ACCOUNTING GRADE 11Document25 pagesRATIO ANALYSIS FOR ALWADI INTERNATIONAL SCHOOL ACCOUNTING GRADE 11FarrukhsgNo ratings yet

- Unit 3 - Cashflow RatiosDocument5 pagesUnit 3 - Cashflow RatiosVishika jainNo ratings yet

- Foundations of Financial Ratio AnalysisDocument49 pagesFoundations of Financial Ratio AnalysisAnna MahmudNo ratings yet

- Analyze financial ratios to evaluate FM222 courseDocument60 pagesAnalyze financial ratios to evaluate FM222 courseLai Alvarez100% (1)

- Ratio Analysis: DR Simran KaurDocument33 pagesRatio Analysis: DR Simran Kaurauddyuttam1No ratings yet

- Financial Statement Analysis Justin Miguel C. YturraldeDocument21 pagesFinancial Statement Analysis Justin Miguel C. YturraldeJustin Miguel Cato YturraldeNo ratings yet

- Ratio AnalysisDocument21 pagesRatio AnalysisRasha rubeenaNo ratings yet

- Finance v3Document41 pagesFinance v3Marcus McGowanNo ratings yet

- Ratio Analysis - A2-Level-Level-Revision, Business-Studies, Accounting-Finance-Marketing, Ratio-Analysis - Revision WorldDocument5 pagesRatio Analysis - A2-Level-Level-Revision, Business-Studies, Accounting-Finance-Marketing, Ratio-Analysis - Revision WorldFarzan SajwaniNo ratings yet

- Business RevisionDocument5 pagesBusiness RevisionCressida KhoueiryNo ratings yet

- Financial Statement & Ratio AnalysisDocument37 pagesFinancial Statement & Ratio AnalysisNeha BhayaniNo ratings yet

- ProfitabilityDocument30 pagesProfitabilitySumit KumarNo ratings yet

- Understand key liquidity ratios like current ratio and quick ratio to evaluate a firm's ability to meet short-term obligationsDocument80 pagesUnderstand key liquidity ratios like current ratio and quick ratio to evaluate a firm's ability to meet short-term obligationsAppleCorpuzDelaRosaNo ratings yet

- Ratio AnalysisDocument26 pagesRatio AnalysisPratibha ChandilNo ratings yet

- Chapter 14 - Financial Statement AnalysisDocument40 pagesChapter 14 - Financial Statement Analysisphamngocmai1912No ratings yet

- Balance Sheet: Current AssetsDocument32 pagesBalance Sheet: Current AssetsGiri ReddyNo ratings yet

- Assignment Ratio AnalysisDocument7 pagesAssignment Ratio AnalysisMrinal Kanti DasNo ratings yet

- Working Capital-1 PDFDocument57 pagesWorking Capital-1 PDFClarenciaAdhemesTantriNo ratings yet

- Finance v4Document54 pagesFinance v4Marcus McGowanNo ratings yet

- Packages LTD.: Group MembersDocument31 pagesPackages LTD.: Group MembersVania MalikNo ratings yet

- Financial Statement AnalysisDocument27 pagesFinancial Statement AnalysisConikka Jane LagamayoNo ratings yet

- Profitability RatiosDocument24 pagesProfitability RatiosEjaz Ahmed100% (1)

- Financial Management Slides 2.3Document10 pagesFinancial Management Slides 2.3honathapyarNo ratings yet

- Answer 1.: Straight Line DepreciationDocument11 pagesAnswer 1.: Straight Line DepreciationDanish ShaikhNo ratings yet

- Profitability & Liquidity Ratio AnalysisDocument19 pagesProfitability & Liquidity Ratio AnalysisananditaNo ratings yet

- Accounting Exam 1: Review Sheet: InvestingDocument8 pagesAccounting Exam 1: Review Sheet: Investingюрий локтионовNo ratings yet

- Ratio NotesDocument4 pagesRatio Notesmoots altNo ratings yet

- Ratio AnalysisDocument37 pagesRatio AnalysisPriya SaxenaNo ratings yet

- RatiosDocument11 pagesRatioshansali diasNo ratings yet

- Financial Ratio Analysis GuideDocument39 pagesFinancial Ratio Analysis Guidebenjy woodNo ratings yet

- Finance and Accounting For Non-Financial ManagersDocument36 pagesFinance and Accounting For Non-Financial Managershenry720% (1)

- Ratio Analysis: Ratio Analysis Is The Process of Establishing and Interpreting Various RatiosDocument26 pagesRatio Analysis: Ratio Analysis Is The Process of Establishing and Interpreting Various RatiosTarpan Mannan100% (2)

- Ratio Analisis PresentationDocument21 pagesRatio Analisis PresentationMian TalhaNo ratings yet

- Mba 224 FINALDocument37 pagesMba 224 FINALJholina Kris HernandezNo ratings yet

- CHAPTERS Analysis and InterpretationDocument17 pagesCHAPTERS Analysis and InterpretationJAPHET NKUNIKANo ratings yet

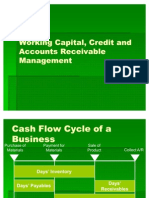

- Working Capital, Credit and Accounts Receivable ManagementDocument31 pagesWorking Capital, Credit and Accounts Receivable ManagementAnkit AgarwalNo ratings yet

- Project Appraisal Ratio Analysis - 2023 - Students - SlidesDocument36 pagesProject Appraisal Ratio Analysis - 2023 - Students - SlidesThaboNo ratings yet

- BusinessReview24 3 Ratio AnalysisDocument15 pagesBusinessReview24 3 Ratio AnalysisJahanzaib MalikNo ratings yet

- Receivables Management: Unit 5Document28 pagesReceivables Management: Unit 5ANUSHANo ratings yet

- Ratio Analysis: A2 AccountingDocument19 pagesRatio Analysis: A2 AccountingrahimiranNo ratings yet

- Ratio Analysis Formulas Guide Under 40 CharactersDocument6 pagesRatio Analysis Formulas Guide Under 40 CharactersSri Royal100% (1)

- Business Metrics and Tools; Reference for Professionals and StudentsFrom EverandBusiness Metrics and Tools; Reference for Professionals and StudentsNo ratings yet

- Accounting and Finance Formulas: A Simple IntroductionFrom EverandAccounting and Finance Formulas: A Simple IntroductionRating: 4 out of 5 stars4/5 (8)

- CPA Review Notes 2019 - BEC (Business Environment Concepts)From EverandCPA Review Notes 2019 - BEC (Business Environment Concepts)Rating: 4 out of 5 stars4/5 (9)

- Tutesols Chap14Document2 pagesTutesols Chap14jackmaloufNo ratings yet

- Tutesols Chap13Document1 pageTutesols Chap13jackmaloufNo ratings yet

- Tutesols Chap05Document1 pageTutesols Chap05jackmaloufNo ratings yet

- Week 12 Homework Chapter 6 Q12Document3 pagesWeek 12 Homework Chapter 6 Q12jackmaloufNo ratings yet

- HSC Physics Space NotesDocument21 pagesHSC Physics Space NotesjackmaloufNo ratings yet

- Week 12 Homework Chapter 6 Q12Document3 pagesWeek 12 Homework Chapter 6 Q12jackmaloufNo ratings yet

- HSC Physics Astrophysics NotesDocument26 pagesHSC Physics Astrophysics NotesjackmaloufNo ratings yet

- IFA 200536 Intermediate Financial Accounting Homework Solutions Chap 11Document1 pageIFA 200536 Intermediate Financial Accounting Homework Solutions Chap 11jackmaloufNo ratings yet

- HSC Physics Space NotesDocument21 pagesHSC Physics Space NotesjackmaloufNo ratings yet

- AThe Impact of Sectarianism On The Relationship Among Christian Denominations in Australia PreDocument2 pagesAThe Impact of Sectarianism On The Relationship Among Christian Denominations in Australia PrejackmaloufNo ratings yet

- Business Studies Marketing NotesDocument13 pagesBusiness Studies Marketing Notesjackmalouf100% (1)

- MinorDocument1 pageMinorjackmaloufNo ratings yet

- Tute Questions Chap01Document1 pageTute Questions Chap01jackmaloufNo ratings yet

- Management TheoriesDocument10 pagesManagement TheoriesjackmaloufNo ratings yet

- Budget Book 2020 21Document163 pagesBudget Book 2020 21sjcemallikNo ratings yet

- Duke MBA Consulting Club Casebook 2017-2018: 20+ New Cases for Consulting InterviewsDocument365 pagesDuke MBA Consulting Club Casebook 2017-2018: 20+ New Cases for Consulting InterviewsThanh PhamNo ratings yet

- Financial Projections TemplateDocument17 pagesFinancial Projections Templatedeepscribd100% (1)

- 1.Bd InitialaDocument4,241 pages1.Bd InitialaCorovei EmiliaNo ratings yet

- Ratios Notes and ProblemDocument6 pagesRatios Notes and ProblemAniket WaneNo ratings yet

- Fiscal Policy in the RBC Model: Lump Sum FinanceDocument20 pagesFiscal Policy in the RBC Model: Lump Sum FinanceAnkit KariyaNo ratings yet

- Neill-Wycik Owner's Manual From 1970 PDFDocument30 pagesNeill-Wycik Owner's Manual From 1970 PDFNeill-WycikNo ratings yet

- 2015 HW2Document4 pages2015 HW2trollingandstalkingNo ratings yet

- PNB v. CADocument8 pagesPNB v. CAAlexandra Nicole SugayNo ratings yet

- Depp Cross Complaint Stsmped WMDocument31 pagesDepp Cross Complaint Stsmped WMAnonymous lAYtGBUqRNo ratings yet

- Ucc Security Agreement SampleDocument9 pagesUcc Security Agreement SampleEVI100% (23)

- Small Business Finance: Using Equity, Debt, and GiftsDocument40 pagesSmall Business Finance: Using Equity, Debt, and GiftsMahmoud AbdullahNo ratings yet

- Martinez v. CavivesDocument5 pagesMartinez v. CavivesPolo MartinezNo ratings yet

- Amen ProposalDocument34 pagesAmen ProposalGetu WeyessaNo ratings yet

- CH 05 Evaluating Financial PerformanceDocument42 pagesCH 05 Evaluating Financial Performancebia070386100% (1)

- Stop The Pirates NotesDocument1 pageStop The Pirates NotesNoah Body100% (4)

- Airborne Express Case StudyDocument49 pagesAirborne Express Case StudyNotesfreeBookNo ratings yet

- This Document Is Downloaded From Cityu Institutional Repository, Run Run Shaw Library, City University of Hong KongDocument23 pagesThis Document Is Downloaded From Cityu Institutional Repository, Run Run Shaw Library, City University of Hong KongDellNo ratings yet

- Nepal Debt Sustainability AnalysisDocument29 pagesNepal Debt Sustainability AnalysisSatis ChaudharyNo ratings yet

- (Elgar Original Reference) Philip Arestis, Malcolm C. Sawyer-Handbook of Alternative Monetary Economics-Edward Elgar Publishing (2007) PDFDocument535 pages(Elgar Original Reference) Philip Arestis, Malcolm C. Sawyer-Handbook of Alternative Monetary Economics-Edward Elgar Publishing (2007) PDFMateus Ramalho100% (3)

- ASF Securitisation Professionals - Slide Pack - 21 & 22 JuneDocument160 pagesASF Securitisation Professionals - Slide Pack - 21 & 22 Junep3tridishNo ratings yet

- Capital Letter in Your Answer Sheet Your Choice Based On The Principles ofDocument8 pagesCapital Letter in Your Answer Sheet Your Choice Based On The Principles ofXiu MinNo ratings yet

- Financial Statement Analysis - CPARDocument13 pagesFinancial Statement Analysis - CPARxxxxxxxxx100% (2)

- Fitch Monthly July 2014Document1 pageFitch Monthly July 2014jaycamerNo ratings yet

- Servicing Alignment Initiative - Overview For Fannie Mae ServicersDocument5 pagesServicing Alignment Initiative - Overview For Fannie Mae Servicersmoses_wong_2No ratings yet

- Contemporary Mathematics For Business and Consumers, Third EditionDocument6 pagesContemporary Mathematics For Business and Consumers, Third EditionAphelele JadaNo ratings yet

- Math 134 Tutorial 8 Annuities Due, Deferred Annuities, Perpetuities and Calculus: First PrinciplesDocument5 pagesMath 134 Tutorial 8 Annuities Due, Deferred Annuities, Perpetuities and Calculus: First PrinciplesJVA ACCOUNTINGNo ratings yet

- Band Agreement - 2021 (2) .Docx - 1Document8 pagesBand Agreement - 2021 (2) .Docx - 1Gerard Albert PanlilioNo ratings yet

- Belco Global Food PDFDocument14 pagesBelco Global Food PDFRahul Kashyap100% (1)

- ABMF 3174 Financial ManagementDocument23 pagesABMF 3174 Financial ManagementRayNo ratings yet