Professional Documents

Culture Documents

Report On MCB Khwaza Khela Branch

Uploaded by

Umair Ahmed UmiOriginal Description:

Original Title

Copyright

Available Formats

Share this document

Did you find this document useful?

Is this content inappropriate?

Report this DocumentCopyright:

Available Formats

Report On MCB Khwaza Khela Branch

Uploaded by

Umair Ahmed UmiCopyright:

Available Formats

Internship Report on Muslim Commercial Bank.

(Khwaza khela Branch Swat)

CHAPTER 1 INTRODUCTION OF STUDY

1.1 BACKGROUND OF THE STUDY

It is a common practice at universities during the completion of the master and bachelor programs to attain practical experience in different fields. Government college of Management sciences Peshawar requires students to undergo an eight weeks internship program. The selection of the firm is based on the choice of the student. The institute requires an internship report based on the theoretical and practical learning of the student. The concern of this report is to study and analyze the performance of Muslim Commercial Bank Ltd (MCB) in the banking industry of Pakistan. Commercial banks are considered to be more competent and productive as they mobilize investment and provide better customer services. Muslim Commercial Bank is considered to be one of the prominent banks as far as its reputation and progress is concerned. Its name stands for a sign of trust and reputation.

1.2

PURPOSE OF STUDY

The purpose of the report has been to review and analyze the functions performed by the Operation Department of MCB. The report also explores the strengths and weaknesses of the MCB and also gives recommendation where any improvement can be possible.

1.3

SCOPE OF WORK

This report is concerned with the performance of the MCB Khwaza khela Branch. It enlightens the functions of Operation Department at the Khwaza khela branch however the financial analysis is based on the national operations of the bank

Internship Report on Muslim Commercial Bank. (Khwaza khela Branch Swat)

1.4

METHODOLOGY OF THE REPORT

The methodology for the collection of information and data was based on the two primary modes of data. Sources of Primary data: o Personal Observation. o Interviews of Personnel. Sources of Secondary data: o Previous internship Reports. o Brochures. o Annual Report. o Books. o Web site.

1.5

SCHEME OF THE REPORT

The report is arranged in the following sequence. PART I This Part has one chapter. Chapter 1: This is an introductory chapter which describes the background, purpose, scope, methodology and scheme of the report. PART II This Part includes the review of Muslim Commercial Bank. This Part is comprised of three chapters. Chapter 2:

Internship Report on Muslim Commercial Bank. (Khwaza khela Branch Swat)

This chapter encompasses a brief history of banking and over all banking sector in Pakistan. It also tells about the history of MCB, its vision and mission statement and the role of MCB in Pakistan. Chapter 3: This chapter goes in detail study about the policies adopted at the branch, the organizational structure, different types of services offered by the branch to its customers. Chapter 4: This chapter is the lengthiest chapter of the report. It precisely tells about the several departments working at MCB Khwaza khela Branch and their functions. The departments discussed are the Operation Department, Clearing Department, Remittance Department, Credit Department, Computer Department, Cash Department and Customer Services Department. In addition to these departments the different types of account and the procedure of the accounts have been discussed. PART III This Part also has two chapters and it is about the financial and SWOT analysis of MCB. Chapter 5: This chapter makes the financial analysis of MCB. Financial analysis is made on the national performance of the bank. Chapter 6: This chapter contains the SWOT Analysis of MCB. PART IV This Part contains one chapter. Chapter 7: This chapter gives the Finding and recommendations based on the analysis of the organization.

Internship Report on Muslim Commercial Bank. (Khwaza khela Branch Swat)

PART V This Part contains the conclusive chapter of the report. Chapter 8: This chapter is about the implementation plan that has been advised for MCB Khwaza khela Branch on the basis of the room of improvements.

Internship Report on Muslim Commercial Bank. (Khwaza khela Branch Swat)

CHAPTER 2 INTRODUCTION OF MUSLIM COMMERCIAL BANK

2.1 HISTORY OF BANKING

There are various views about the origin of the word Bank. One view is that it is derived from an Italian word banque which means bench the other point of view is that it has originated from the German word bancus which means a joint stock firm. As regards the growth of modern commercial bank, it can be traced to as early as 600BC, G Crowther in his famous book, an outline of Money has traced the history of modern English commercial banking. According to him, the present day banker has three ancestors; (1) the merchants (2) the goldsmiths and (3) the money lenders. The Merchants. The earliest stage in the growth of banking can be traced to the working of merchants. These merchants were traders in commodities. The trading activities were carried on by them from one place to another, it was risky for the traders to carry metallic money with themselves for payment. The traders with high reputation began to issue receipt which were accepted as titles of money. These receipt or letters of transfers also called hundi in indo Sub Continent were the

Internship Report on Muslim Commercial Bank. (Khwaza khela Branch Swat)

first mode of payments. The merchant banking thus forms the earliest stage in the evaluation of modern banking The Goldsmiths. The second stage in the growth of banking is normally traced to earlier goldsmiths. These goldsmiths also called Seths in India used to receive gold and silver for sage custody. The goldsmiths began to issue receipts for the metallic money (gold and silver) kept with them. These receipt with the passage of time a medium of exchange and a mean of payment. The goldsmiths, thus can rightly be termed as the forerunners of the modern bank note. The Money Lenders. The third stage in the development of banking arose when the goldsmiths became the money lenders. By experience the goldsmiths (who were called money lenders) came to know that they could keep a small proportion of the total deposits for meeting the demand of customers of cash and the rest they could easily lend. They allowed the depositors to drew over and above the money actually standing to their credit.

2.2 DEVELOPMENT OF MODERN BANKING

It is said that the first bank was established in Barcelona in Spain. Another statement tells that Venice and Genoa was the hub of financial transactions and the first bank was founded there in 14 th century. The first public bank that was formed was in Germany in later part of the time. The first central bank was formed in Geneva in 1578. bank of England was established in 1694. the modern commercial banking system actually developed in the nineteenth century.

Internship Report on Muslim Commercial Bank. (Khwaza khela Branch Swat)

In 1918 eleven clearing banks of today came into being. The effect of this historical development of banking in England has been fairly wide. Initially the emergence of a small number of banks with wide network of branches. Second, increase in the popularity of bank accounts and a large-scale use of checques. In 1946, the labor government nationalized the bank of England and transferred the existing stock to the nominee of British treasury. In 1955, the British Banks made a departure from traditional banking by undertaking hire-purchase finance for companies buying industrial plants and machinery and took interest on hire-purchase finance.

2.3

BANKING IN PAKISTAN

Before the partition of India and Pakistan in 1947, branches of British banks dominated banking in sub-continent. The first domestic banking institutions emerged in the 1940, immediately after Pakistan's independence from Britain. These institutions include the Australasia Bank (today, Allied Bank Limited), Habib Bank Limited, Muslim Commercial Bank, and the National Bank of Pakistan (NBP). The NBP was wholly owned by the government but prominent merchant families established the other three. On August 14, 1947 by an order called Monetary system and reserve order 1947 the main provisions of the Monetary system and reserve order 1947 were as follows (i) (ii) (iii) The reserve bank of India would be the sole currency note issuing authority in Pakistan till September 30, 1948. The Indian currency notes will remain legal tender in both Pakistan and India until September, 30, 1948. The reserve bank of India would transfer the assets of value equal to Pakistani currency to the government of Pakistan after September,30 1948.

Internship Report on Muslim Commercial Bank. (Khwaza khela Branch Swat)

(iv)

The government of Pakistan would also issue coins in the country after September 30, 1948. The coins issued by the government of India would remain legal tender in Pakistan for at least one year form the date of issue of Pakistani coins.

The Reserve bank of India would perform the full functions of central bank in Pakistan up to September 30, 1948.On 1st July 1948, the SBP was formed. From 1960 to 1970, a number of specialized development finance institutions (DFIs) such as Industrial Development Bank of Pakistan and the Agricultural Bank emerged. These DFIs were either controlled directly by the state or through the SBP, and were intended to concentrate on lending to long-term projects in specific priority sectors.

2.4 HISTORY OF MUSLIM COMMERCIAL BANK

Muslim Commercial Bank (MCB) unfolds 62 years of growth. MCB is not an overnight success story. The bank started corporate life in Calcutta on July 9, 1947. After the partition of the Indo-Pak Subcontinent, the bank moved to Dhaka from where it commenced business in August 1948. In 1956, the Bank transferred its registered office to Karachi, where the Head Office is presently located. Thus, the bank inherits a 62-years legacy of trust in its customers and the citizens of Pakistan. 2.4.1 Nationalization In 1974 the Government felt a harsh need of nationalization of banks and financial institutions and nationalization act was introduced. Under this act MCB was the first bank, which was nationalized. In the same

Internship Report on Muslim Commercial Bank. (Khwaza khela Branch Swat)

year Premier Bank was merged with MCB and it started work as a government bank. This nationalization affected the bank badly. 2.4.2 Privatization

All the financial institutions and banks did not show good performance after nationalization, and again the government felt a big need to privatize these banks. In 1991 the bank was privatize during Nawaz Sharifs government. The government of Pakistan transferred the management of the bank to National group, one of the leading groups in the field of business. They were sold 25% shares. Now this group is having 50% of the total shares. Government is having 25% shares and general public is also having the same shares.

2.5

MCB Today.

Today MCB is one of the leading banks of Pakistan with a deposit base of about Rs. 280 billions and total assets of around Rs. 443,616 millions. The Bank has a customer base of approximately 4 million and a nationwide distribution network of 1,047 branches, including 8 Islamic banking branches and 7 overseas branches , and over 300 ATMs, and having 10,160 own permanent employees. During the last fifteen years, the Bank has concentrated on growth through improving service quality, investment in technology and people, utilizing its extensive branch network, developing a large and stable deposit base.

2.6

VISION

AND

MISSION

STATEMENT

OF

MUSLIM COMMERCIAL BANK.

VISION: To be the leading financial services provider, partnering with our customers for a more prosperous and secure future.

Internship Report on Muslim Commercial Bank. (Khwaza khela Branch Swat)

10

MISSION: We are a team of committed professionals, providing innovative and efficient financial solutions to create and nurture longterm relationships with our customers. In doing so, we ensure that our shareholders can invest with confidence in us.

Internship Report on Muslim Commercial Bank. (Khwaza khela Branch Swat)

11

References Nasir, Saeed M. (2010) Money Banking & finance. Lahore: Khan Faizan, Report on BoK, MBA (F), 2006-08(A/N) Balance Sheet of MCB (Dec 31, 2011) (On-line) Available. http://WWW.MCB.Com <Accessed on July 16, 2009>. Ahmad Zeeshan , Report On MCB, MBA (F), Session 2006-2011.

Internship Report on Muslim Commercial Bank. (Khwaza khela Branch Swat)

12

CHAPTER 3 OVERVIEW OF MCB KHWAZA KHELA BRANCH

The MCB Khwaza khela Branch is headed by the manager. He is the responsible person for any activity that is happening inside the premises of the branch. He looks over different issues in the branch. There is also sub manager knows as Operation Manager. The operation manager is responsible for the operation side of the branch. There are also many officers who include the remittances, clearing, on-line, cash department and credit officer, but all the activities of the officers are linked with the operation manager except the credit officer.

3.1

PROCESS FLOW

The MCB Khwaza khela branch is headed by the Branch Manager. Several staff officers are delegated different responsibilities. The organizational structure is a combination of line and staff hierarchy. The branch manager is assisted by the Manager Operation. Several other officers like the head of cash department and remittance department coordinate with the Manager Operation. Credit department is not as busier as the remittance and other departments while the credit officer does not assist the manager operation. Though the branch does not deal in letter of credits and foreign exchange, but it is over burden. There are not routine transactions in the credit department therefore only one officer is responsible for the department. While operation department is over burden, that is why several other workers from remittance department

Internship Report on Muslim Commercial Bank. (Khwaza khela Branch Swat)

13

or contract workers assist the department. Internees are often assigned with the operation for help. The customer service department is responsible for assistance of customer related issues. The officer of the department is known as Customer Service Officer (CSO). The officer deals and helps the account holder as well as the walk in customers The details of all the departments are given in a later chapter of the report.

3.2 ORGANIZATIONAL STRUCTURE at Head office

Board Of Directors

President & CEO

Secretary

Division Heads

Computer Division Account Division

Marketing Division

H R M Division Credit Management Division Business Development Division

Legal Affair Division Inspection and Audit Division

Training & Research Division Treasury Division

R&D Division

R T C Division

Internship Report on Muslim Commercial Bank. (Khwaza khela Branch Swat)

14

STRUCTURE AT THE CIRCLE OFFICE

G. M

(Regional Head)

R M Peshawar

R M Mardan

R M Kohat

Credit In charge Financial Controller

Internal Control Unit (ICU)

Quality Service Assurance

(Q S A)

Cash Mgt Officer Staff Officer

Internship Report on Muslim Commercial Bank. (Khwaza khela Branch Swat)

15

STRUCTURE AT MCB KHWAZA KHELA BRANCH

Internship Report on Muslim Commercial Bank. (Khwaza khela Branch Swat)

16

Branch Manager Mr. Tasbih Ullah Khan

Manager Operation Sajid

Credit Officer Qasim Faroqi

Clearing Officer

Remittances Officer

Computer Department

Cash Department

Customer Services Officer

3.3

SERVICES OFFERED AT THE MCB

Muslim Commercial Bank offers different kind of services to its customers. The Bank charges its customer according to the schedule of charges. However, it also offers some complimentary services for free. Some of the services, offered at MCB Khwaza khela Branch are as follows: 1. 2. 3. 3.3.1 Credit Cards ATM Cards. Lockers

credit cards

MCB provides two kinds of Credit Cards. The first one is known as Visa Cards and the second one is called Master Card. 3.3.1.1 MCB VISA Card Whenever customer needs cash, he/she can use MCB VISA with a PIN (Personal identification Number) at ATMs to withdraw an amount up to 50% of his available credit limit. MCB VISA card is not just another

Internship Report on Muslim Commercial Bank. (Khwaza khela Branch Swat)

17

credit card. It not only provides conventional credit card services in a manner that is superior in comparison, but goes an extra mile. MCB VISA is accepted at all ATMs across Pakistan as at 27 million acceptance locations worldwide. MCB VISA is a name synonymous with unique, innovative and state of the art services making it the most secure affordable and rewarding card. MCB offers two types of VISA card. a. Classic Card The joining fee of classic card is Rs. 250 and annual fee is 250 rupees. The supplementary annual fee is 250 rupees. Here it should be noted that to avail the facility of credit card the person must have an account in the banks branch. b. Gold Card

The joining fee of Gold card is 350 rupees; while the annual fee is 350 rupees and the supplementary annual fee are 350 rupees. Monthly payments are made as follows: For paying cash over the counter at any MCB Branch, the bank will charge Rs.100 on cash payment. Sending a checques/pay order/draft in the name of MCB, VISA. Bank will charge Rs.250 on all checques that are returned unpaid. Telegraphic Transfer: Payment is credited to the customers account when bank receives the funds. Documents Required for Credit Card: Copy of National Identity Card Personal bank statement for last 6 months If Partnership Firm, Partnership Deed/Bank letter If Proprietorship, Bank Letter

Internship Report on Muslim Commercial Bank. (Khwaza khela Branch Swat)

18

For salaried people, Salary Slip should be attached. 3.3.1.2 MCB MASTER CARD. MCB master card is simply a credit facility to its clients. The card holders have a facility to shop to a particular limit from over 12 millions merchants welcoming the card with in the country and globally as well. The card was introduced in the year 1995, and now offered more flexible services to its holders. The main feature of the card is as under. MCB is the 1st bank in Pakistan introduced enhanced feathers of photograph on the card limiting fraud. It has over 3000 outlets in Pakistan. Provides 24 hours customers services. Cash advance facilities are available in Pakistan and world wide. 3.3.2 ATM Cards

ATM stands for Automated Teller Machine. ATM cards are issued on the request of the customer and are only for Pak Rupees account holders. ATM card provides the customers with round the clock access to their accounts even after the banking hours. MCB provides the following types of ATM cards. Here it should be noted that to avail the facility of ATM card the person must have account and balance in account. Issuance of ATM Card: All activities related to ATM cards are performed by Operation department. The operation Manager collects the request for ATM cards by getting the form filled by the customer. A file is preserved to record

Internship Report on Muslim Commercial Bank. (Khwaza khela Branch Swat)

19

all the ATM cards applications. A list is then made of these requests and is sent to the Karachi Head Office (card division). When the bank receives the cards, the concerned officer arranges them in alphabetical order of customers names. A file is maintained to record the names and account numbers of the customers whose cards have been received by the bank. Customers are called at their phone numbers then to collect their cards or they are earlier at the time of filling application notified about the collection date. The customer can collect their cards from the bank when they are ready. It should be noted that the card is kept in the custody of operation manager while the PIN code is kept in the custody of supervisor of the branch. a. Classic Card

The joining fee of classic card is Rs. 250 and annual fee is 250 rupees. The supplementary annual fee is 250 rupees. The maximum limit of withdrawal on the classic card is Rs. 10000. In 24 hours. b. Gold Card

The joining fee of Gold card is 350 rupees; while the annual fee is 350 rupees and the supplementary annual fee are 350 rupees. The maximum limit of withdrawal on the gold card is Rs. 25000 in 24 hours. 3.3.2.1 Functions of ATM card: ATM card has following functions: Cash Withdrawal. It can be used to check the account balance. Transfer balance from one account to another account. Withdrawals through credit cards.

Internship Report on Muslim Commercial Bank. (Khwaza khela Branch Swat)

20

3.4 LOCKER SERVICE At the MCB Khwaza khela branch, safe keeping service is also provided to customers. When a customer rent locker, the relation between the Bank and the Renter is that of a Licensor and Licensee. To acquire a locker, He/ she must be an account holder at the Bank. The customer must attach a copy of ID card with the locker rental form. 3.4.1 Locker Rent year 2012 are: Small size lockers are rented for Rs.3,500 p.a. Medium size locker is rented for Rs. 4200. p.a Large lockers are rented for Rs.5000. p.a Locker purchase fee is Rs.2000 If key is lost by the customer or for any other damage to the locker, Bank charge Rs.5000 One locker is rented to one person only. 3.4.2 Rules and Regulations and are automatically renewed from year to year. Lockers may be hired in two or more names but the Renter must give explicit instructions to Bank for mode of operation. A Renter may at his own risk appoint another person to have access to his locker by completing the requisite authority form available on application at the Bank. Letters, telegrams, and telephonic messages implying to authorize a third party access to the lockers are not accepted. The rent of locker is determined by the Bank. New charges for

Lockers are rented for a period of one year in the first instance

Internship Report on Muslim Commercial Bank. (Khwaza khela Branch Swat)

21

The Renter can not use Locker for the deposit of any liquid or anything of explosive, dangerous or offensive nature. In the event of non-payment of rent when due, the Renter forfeits all rights to the use of the locker. If the key of the locker is lost by the Renter, the Bank must be notified without delay. In such an event any expenses to which the Bank may be put in breaking open the locker and substituting a fresh lock and key will be hand over to the Renter. The Bank has a lien on the contents of the locker for all rent due form the renter to the Bank and also for all expenses to which the Bank may be put in breaking open the locker and substituting a fresh lock and key. Bank is entitled to sell the contents of the locker so to recover such expenses. Bank has the authority to Debit the account that Renter may have with the bank, without previous reference to Renter, all dues recoverable from him in respect of the locker. 3.4.3 Termination of Rental In order to terminate the rental, notice must be given one month prior to the expiry date of the rental. The locker with its key must be surrendered to the Bank before closing hours of the bank on the expiry date of the rental. 3.4.4 Death of Renter

In the event of the death of a sole Renter of a locker or of the last surviving Joint Renter of a locker, the Bank may at its option permit the legal representative of the deceased sole Renter, to inspect the contents of the locker. On the production of Probate letter of Administration, the Executor or Administration named, have power to

Internship Report on Muslim Commercial Bank. (Khwaza khela Branch Swat)

22

deal with the contents of the locker and is deemed to be the Renter of such locker in the place of the original Renter. References: Brochures of MCB Visa Card Sajjad Muhammad, Report of MCB, MBA (F), 2006-08 Gul, Naveed, S. Report on MCB, MBA (F), 2010-08 Schedule of Bank Charges 2010-11. Interview with the Manager Operation. Locker opening form.

Internship Report on Muslim Commercial Bank. (Khwaza khela Branch Swat)

23

CHAPTER 4 PROFILE OF DIFFERENT DEPARTMENTS

Every organization is divided into definite departments. Each department performs different kind of job and requires staff with specialized skill to handle the particular job. This increases the efficiency of workers and makes the job of the employees easier. There are several aspects on which departmentalization in an organization can be based. The division can be made on the basis of functions, product, customers or geographical location. The Khwaza khela Branch of MCB is comprised of several departments. The division is made on the based of functions and job they perform. Hence it can be concluded that MCB has adapted to the policy of functional departmentalization. The main departments at the MCB Khwaza khela Branch are mentioned below, also included is the detailed study at the specific function these departments perform. (1) Operation Department. (2) Clearing Department. (3) Remittance Department. (4) Credit Department. (5) Computer Department. (6) Cash Department. (7) Customer Services Department (CS)

4.1 OPERATION DEPARTMENT.

The operation department is one of the most important departments at any commercial bank. This department is responsible for the entire

Internship Report on Muslim Commercial Bank. (Khwaza khela Branch Swat)

24

operation and function of the branch. This department is controlled by the operation manager, who is senior and experienced employees of the bank, for the post of operation manager the employee should be at least, O G I or II having service in bank of minimum 10 years. The operation manager ensures the smooth and error free working in branch. He/she is responsible for the rectification of the entire audit objection imposed by the Internal Control Unit (ICU). The tasks of the operation manager are under. Feeding of newly opened accounts in to system Issuance of checque book. Custodian of security stationery. Dealing with the claim of the customers. Issuance of PIN code of ATMs Card to customers. Supervision of heavy amount transactions. Supervising the working of the rest of the departments.

4.2 CLEARING DEPARTMENT.

Clearing system is a device that enables bankers to settle checques and other instruments, drawn on each other. System is of immense value in saving a lot of labor, time and expenditure there by increasing the efficiency of the banking system. SBP provides the services of clearing house, to all the schedule banks in Pakistan. SBP has its branches in all big cities nationwide and clearing in these cities is supervised by SBP. In cities with no SBP coverage, the clearing is supervised by NBP. Brief Working of Clearing Department

Internship Report on Muslim Commercial Bank. (Khwaza khela Branch Swat)

25

The Checques received by a bank drawn on other banks are sorted bank wise. A schedule is prepared for checques drawn on each bank. The checques along with the schedule are presented in the clearinghouse where they are delivered to the representative of the various banks. Thus each bank receives from other banks checques drawn upon it and delivers to other bank checques drawn upon them. The first one is the inward clearing and the other is the outward clearing. The net difference is settled by Dr and Cr, to their banks account with the supervising bank. Inward and Outward Clearing. Checques collections for credit cards and reporting to Credit Center. Collections of outstation checques. Honoring of checques, orders and drafts sent by other branches/banks.

4.3 REMITTANCE DEPARTMENT.

This department of the commercial banks is responsible for the issuance of Demand Draft (DD), Pay order, Telegraphic Transfer (TT), Mail Transfer (MT). Demand Draft is a written order issued by one branch to another branch of the same bank to pay a certain some of money to the person named in the instrument. Every customer whether account holder or not can avail this facility by paying bank charges and the amount of draft and can get the demand draft. Normally the D D is crossed at the time of its issuance, so the payment of the instrument is paid just like the crossed checque. Pay order, is issued with in the city payment, or if the bank want to make payment to any person, for this purpose pay order is issued, it

Internship Report on Muslim Commercial Bank. (Khwaza khela Branch Swat)

26

should be noted that this instrument is drawn upon the issued branch not on any other like demand draft. Telegraphic Transfer, this mean of transfer of fund has diminished due to online banking service, but still this mean of transfer of fund is used to far-flung areas branches or where the on-line facility is not available, here an written advise is send through FAX machine to the respondent branch having the complete account detail of the person in favor of whom the fund is transferred. Mail Transfer is also used to the branches in remote area of no on-line facility, here the amount of fund is transferred just like the T T but it is through post/ mail to the responding branch.

4.4 CREDIT DEPARTMENT.

Lending produces the profit for a bank. It is the most important function of a bank. It generates the banks own profits. The money that a bank lends to someone is already somebody elses deposit. All the banks do is pay less interest to deposit holders and earn more from lending customer. The difference generates profit to the bank. The credit department of the branch sanctions the following types of loans/ credit. 4.4.1 a. b. c. Loans Running Finance Facility Demand Finance Facility Personal Loans MCB advances three types of loans

4.4.1.1 Running Finance Facility This facility is allowed to current account holders only, under this type of loan the customer is given a limit on his account, which runs on the debit side when he/she withdraws money. The interest is calculated

Internship Report on Muslim Commercial Bank. (Khwaza khela Branch Swat)

27

only on the portion of money which has actually been used by the account holder on daily basis and is payable at the end of every quarter. This facility is allowed to the account holder for the period of one year from the date of sanction of the loan, while it could be renewed upon the request of the customer and also the financial position of the account holder. 4.4.1.2 Demand Finance Facility It is a terminating loan in which full sum of the sanctioned loan is credited to the customers account on the day the loan is sanctioned. The difference between the running finance and demand finance is that in running finance the customer is given a limit and he can withdrawals up to that limit according to his need and he can return the money whenever he/she wish and the interest is charged on the money which has been used actually. However, in demand finance facility, after the loan is sanctioned and the money is withdrawals by the customer, the customer repays the loan and the interest amount in monthly installments. While the interest is calculated on the principal amount of loan whether is used or not by the customer. The monthly installment consists the portion of principal amount plus the portion of interest. 4.4.1.3 Personal Loans MCB Personal loan provides with the financial advantages of sufficient fund for holiday, buying a car, refurnishing house and purchasing new T,V, they can also finance better education for children. The client can choose tenure of one to three years for the repayment of loan. Its distinction features includes Bank to Bank balance transfer.

Internship Report on Muslim Commercial Bank. (Khwaza khela Branch Swat)

28

Loan protector shield insurance coverage of balance loan and in case of death or permanent and total disability. Availability of early repayment option. ELIGIBILITY FOR FINANCE FACILITY Loan is only sanction when 100% cash back guarantee is provided to the bank. The following types of securities are accepted for sanction of loan. Government Bonds Special Saving Certificate (SSC), Defense Saving Certificate (DSC) Cash Deposit at the same bank. Foreign bank Guarantees.

4.5 CASH DEPARTMENT

Cash Department deals in receive and Payment of cash. At the cash counter, customers deposit the money and withdrawals cash. The money is deposited either in account or may be for the payment of credit card bill etc while bank makes payments only against the checques. Checques are received and presented for transfer or collection purpose. The employees at cash department also handle the utility bills and credit Card payments. 4.5.1 Cash Collection Cash collection is accompanied by cash deposit slip. The slip contains the account number; title of account and denomination of cash deposited both in words and in figures followed by the signature of the

Internship Report on Muslim Commercial Bank. (Khwaza khela Branch Swat)

29

depositor. The received cash is counted and is verified with the deposit slip. Entries for cash deposits are recorded before handling over receipts to the customer. Customers copy of the deposit slip is handed over to the depositor. Before cash deposit slip is released, it is matched and validated with the entries in the register for cash collection. 4.5.2 Cash Payment Amount of payment of cash in a single transaction is fixed. Payments beyond a certain limits are supported to be approved by an appropriate authority. Before payment, the checques must be checked for post dated payees name, crossing, amount both in words and in figures and authentication of alterations. Tellers verify signatures on checques before payment. In case of illiterate account holder the customer is identified through the photograph available in the banks record and thumb impression attested under the full signature of the teller who is authorized to approve the transaction. The money is kept in the vault which is built along with the cash department. Cash counter is also termed as teller counter. The Department is supervised by a Chief Teller. Every Cashier is provided with a specific amount of money in the morning from the vault. The cashier makes payments to the customers from that money at the end of the day the cashiers check their balances and the remaining amounts is placed back in the vault. Cash handling is sensitive work. Every body at the branch is not allowed to enter the cash department premises. The names of the authorized personnel who are allowed in cash department are mentioned on the entrance door of the cash department. Internees are not allowed to enter the cash department with out the proper permission from the branch manager or chief teller.

Internship Report on Muslim Commercial Bank. (Khwaza khela Branch Swat)

30

4.6 COMPUTER DEPARTMENT

Computer department is the place where the computer Part of the bank is located. This is a very sensitive department of the Bank and only authorized personnel are allowed to enter this Part. The computer department consists of the server of the branch and it regulates all the information that is feed by employees into their computers. Back-up for all the computer systems is maintained in this Part. Every employee is given their personal code which they feed into the system when they work the code is consist on the employee no and password. This code is the identification of an employee. This code is recorded at the computer department and it records every transaction made by any code at any time. Other than recording every transaction the computer department also performs the following functions. Hardware and Software trouble shooting. Installation of new hardware and software. Start of day procedure and end of day procedure i.e. downloading all the data from Karachi Head Office in the morning and, sending all the data back at the end of the day Keeping inventory of all the hardware installed Contacting dealers for maintenance of computers. Taking back-ups on daily basis. Training computer users. The setup of computer department includes the following functions. Setting servers files. Sitting communication and networking equipments. Handling the printers setup in the branch. Maintaining the back-up tape devices.

Internship Report on Muslim Commercial Bank. (Khwaza khela Branch Swat)

31

In other words maintaining every technical aspect of the bank comes in the responsibilities of the data center. Well trained personnel have been employed to look after the operations in computer department. The MCB Khwaza khela Branch is also assisted by the MCB Islamabad Branch in the data center department. Highly qualified recruits from MCB Islamabad Branch make their visits to the MCB Khwaza khela Branch for assistance.

4.7 Customer Service Department

Customer Service Department is the department in the branch which is directly involve in the service and care of customers. This department consist a female officer known as Customer Service Officer (CSO); she serves the account holders and walk in customers. The officer is responsible to attend customers at first hand and solve their problems.

4.8 ACCOUNTS OFFERED

MCB has introduced varied type of accounts to meet different class of customers requirement. It offers accounts in Pak Rupee only. Some of the accounts offered at MCB Khwaza khela Branch are discussed below. Types of Accounts MCB Khwaza khela Branch offers the following local currency accounts. (i) (ii) (iii) (iv) (v) 4.8.1 Current Account. Khushali Bachat Account. Basic Banking Account. Smart Saving Account. P L S Saving Current Account

The salient features of the accounts are described below:

Internship Report on Muslim Commercial Bank. (Khwaza khela Branch Swat)

32

MCB current account allows customers to deposit and withdraw cash at their own convenience. It is best suited for those customers who make huge amount regularly transactions of money in their accounts. The account holder will have to maintain a minimum balance of Rs.10, 000 in this account on the other hand if in any current account the balance is goes down from this amount Rs.50 will be deducted monthly. Bank does not pay any interest on this account. The features promoted for this account by MCB are as follows: Is opened from Rs.10, 000. Non-interest bearing checking account. No Zakat deduction as per the rules of SBP. Standing instructions for regular payments. Any other standing instructions. Running finance facility/Over draft facility. Free 24-hour balance inquiry facility on Phone. Free 24-hour withdrawal facilities through ATM network. Unlimited checques writing. 4.8.2 Khushali Bachat Account (KBA) MCB pays close attention to the low income people and for this purpose many initiatives have been taken in this regards, Khushali Bachat Account is one of these. This type of account is for low income house holders, this account can be opened with one thousand rupees; there is no restriction on regular deposit and withdrawals, however large amount could not be withdrawals at a time. MCB pays half yearly profit on KBA but the rate for the profit is not predetermined. Main features of KBA are

Internship Report on Muslim Commercial Bank. (Khwaza khela Branch Swat)

33

Is opened from Rs. 1,000. No monthly deduction. No restriction on deposit and withdrawals. Profit is paid on half yearly basis. Account holder can avail ATM and other banking facilities. No Running finance/ Over draft is allowed. Free 24-hour withdrawal facilities through ATM network. 4.8.3 Basic Banking Account MCB considers the Students one of the important part of its customer strategy, and special care is given to students. For this purpose a special type of account have been lunched i.e. Basic Banking Account (BBA). BBA can be opened with a minimum amount of one thousand rupees, for opening the account the student would have to present student ID card National I D Card and written request from the concerned institution. No profit is paid and there is no deduction on BBA, maximum withdrawal is from Rs 1500 up to Rs 2000, at a time. Online and ATM facilities are given to the account holder. Main features of BBA are as Is opened from Rs 1000. Is especially for students. No profit is given. No deduction on least balance. ATM and Online facility. Free 24-hour withdrawal facility through ATM network. No Running finance/ over draft facility. Maximum withdrawal is from Rs 1500 up to 2000. 4.8.4 Smart saving Account

Internship Report on Muslim Commercial Bank. (Khwaza khela Branch Swat)

34

Salaried and small income group is also the target customer of MCB, and for this purpose Smart Saving Account has been introduced. Smart Saving Account is opened with a minimum amount of one thousand rupees; the account holder would have to show his/ her pay slip along with the national ID card. Profit is given on this type of account on half year basis, while there is no restriction of the deposit and withdrawals, no running finance facility is given to the account holder. There is also no deduction on the least balance. Main features of the account are as. Is opened from Rs.1000 Is especially for salaried persons. Profit is given after six months. Zakat deduction on 1st Ramadan. No deduction on least balance. 4.8.5 Profit & loss sharing (PLS) Accounts. Another type of account is Profit and loss sharing account (PLS). No interest is paid on this account but it is maintained on the basis of sharing of profit and loss. These accounts are opened mainly by those customers whose banking transactions are not frequent and numerous. Lower and middle income groups, small traders, professionals, farmers and other salaried classes usually make such deposits. Funds can be deposited frequently through cash, checques, demand drafts, pay orders, telegraphic transfers and other such instruments. Main features of the account are as. Is opened from Rs. 5,000. No monthly deduction.

Internship Report on Muslim Commercial Bank. (Khwaza khela Branch Swat)

35

Zakat deduction on 1st Ramadan. No restriction on deposit and withdrawals. Profit is paid on half yearly basis. Account holder can avail ATM and other banking facilities. No Running finance/ Over draft is allowed. Free 24-hour withdrawal facilities through ATM network.

4.9

ACCOUNT RELATED ISSUES

There are several issues which affects the status and legitimacy of the account. They are given stepwise. 4.9.1 Account Opening

Account opening determines relationship between banker and customer. Bank practice maximum concern before opening of an account. Official procedure for opening an account with the bank is given below. Formal Request Account opening form is provided by the bank to its customers. It contains information about the customer, the business or profession he/she works in, income status, addresses and contact numbers etc. Reference The applicant is asked to provide an apposite reference. The individual who gives the reference should be a customer or a bank employee. Specimen Signature Signature serves as an authority of customer drawn on bank. The customer is asked to give specimen signature on a card known as Specimen Signature Card. For illiterate persons, along with two recent photos, left-hand thumb impression for men and right hand thumb impression for women is taken. Signatures of the customers are then

Internship Report on Muslim Commercial Bank. (Khwaza khela Branch Swat)

36

scanned and saved in the computer for signature verification for future reference. Regulations of Account Opening The following rules and regulations are taken into account when an account is opened. When the bank and the applicant accept mutual position and accept all the rules, the account is opened. Against submission of the Banks prescribed application form, duly introduced in the manner provided and on supply of documents required, an account may be opened. Bank has the right to refuse opening an account without giving any reason. Account maintenance fare is charged in rupee for PKR accounts and foreign currency accounts are charged in foreign currency. Current and PLS saving accounts are charged according to the Banks schedule of charges when minimum balance falls below the balance requirement. 4.9.2 Deposits

The bank receives deposits on the following conditions. The Bank accepts checques, drafts, and other instruments, payable to the depositor for collection; entirely at depositors risk. When counting of cash deposited is done after the customer has left the counter and if the amount indicated on the pay-in slip differs from that of the actual cash count, the Bank count is final and conclusive. 4.9.3 Withdrawals Withdrawals at MCB are made in the following pattern.

Internship Report on Muslim Commercial Bank. (Khwaza khela Branch Swat)

37

Checques and other payment instruments are to be signed according to the specimen signature provided to the Bank and amendment are to be legitimated by the drawer full signature. Rupee savings, High Yield Deposits and all types of accounts can not be overdrawn. Cash withdrawals from accounts are subject to availability of currency notes. 4.9.4 Issuance of Cheque Books MCB has started a new system for issuing the checque books to its customers. Checque books are not issued at the time of account opening, this is because MCB issues checque books to its customers after the confirmation of all the information provided by the customer to the bank, and this done through the sending of letter of thanks to the customer by post, when the customer receives the letter and bring it to the branch, it shows that the address and the information provided by the customer are true and correct. Procedure After opening the account with the bank and receiving letter of thanks, customer is asked to fill a checque book request form, provided by the bank the form contains the account numbers, customers names, number of leaves needed by the customer and date of collection of checque book by the customer After getting the checque book request forms the signature of the customer is verified by the verification officer, the officer verifies the signatures, already scanned in the computer at the time of account opening. After verification of signatures, the requisition is given to the operation manager and the operation manager issues the checque book to the customer. Usually 25 or 50-leaf checque book is issued to the individuals and 100-leaf checque book is issued for the companies.

Internship Report on Muslim Commercial Bank. (Khwaza khela Branch Swat)

38

4.9.5 Return on Account The return on accounts is given as: Profit on certain deposits is applied twice a year for periods ending June and December. The profit is announced after respective profit computation is completed for each period according to applicable regulations. Interest on foreign currency account is applied half yearly in June and December on minimum balance during each calendar month. Interest rates on foreign currency savings and term deposits are normally fixed at the beginning of each half-year but the bank has the liberty to fix them on a monthly basis. 4.9.6 Statement Of Account

Bank present account statements to its customer for understanding. In these statements the Bank ensures that all debit and credit entries are correct. In case of error, the bank passes adjusting entries to rectify error without notice. The bank is not liable for any loss or damage due to such errors. The Bank does not require any earlier authorization from the account holder for debiting the account for any expenses, fees, commissions, interest, zakat, tax, stamp duty, excise duty etc. that have come up out of any dealings with the bank. 4.9.7 Account Closure

When an account is closed, the unused checques are returned to the bank immediately. It is made sure to the bank in writing that idle checques have been destroyed. The Bank also can close an account and terminate any other type of relationship with the customer without assigning any reason or prior notice.

Internship Report on Muslim Commercial Bank. (Khwaza khela Branch Swat)

39

References Interviews & working with the respective departments officers. Account Opening Form of MCB. (On-line) Available http://WWW.MCB.Com <Accessed on July 16, 2012>

CHAPTER 5 FINANCIAL ANALYSIS

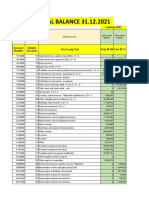

Analysis of an organization discovers its potential areas of improvement and evaluates its performance of the past period. It identifies the possible solutions to problems faced inside the bank and gives an insight of the opportunities which can be exploited to reap benefits. Financial Analysis The financial analysis is based on the national performance of MCB. The different Ratios calculations (figures) have been taken from the annual audited balance sheet for the year ended December 30, 2011.

5.1

FINANCIAL ANALYSIS

Financial analysis of an organization expresses the performance of the bank for over a period of time. Different ratios analyze the banks capabilities. Varied relations are drawn on the basis of this analysis. Financial ratios have their own importance in analyzing the organizations performance. An increase or decrease in one ratio does not mean anything good or bad. It is always linked to another one that

Internship Report on Muslim Commercial Bank. (Khwaza khela Branch Swat)

40

is more important. Considering the example of higher interest, if the bank wants to have most of the deposits of the market, it has to offer higher interest rates. This would bring the deposits, thus deposits will increase, but on the other hand it will have to pay higher interest as well, thus decreasing the profit ratio. Relativity is the prime factor in evaluation of ratios. The financial ratios of the MCB reflect that the banks deposits have increased and it has also increased the profits. Advances have been made which have resulted in the fall of cash. The overall financial position shows that the bank is growing and is on upward direction in profitability as well. The financial Analysis is as follows. Different values come out from the calculations for year ended 2011. 5.1.1 LIQUIDITY RATIOS 5.1.1.1Working Capital Ratio Current Assets-current Liabilities

440000000 420000000

Working Capital Ratio (RS in '000')

Current Asstes Current Laibilities

426352171 394461394

2011 41172321 2011 42635217 Current Assets Current Liabilities 1 38517985 0

2010 39095552 2010 394461394 355365842

400000000 380000000 360000000 340000000 320000000 300000000

385179850

355365842

A measure of liquidity calculated by subtracting current liability from the current assets of the firm. This figure is not useful for comparing the performance of different firms, but it is quite useful for internal control.

Internship Report on Muslim Commercial Bank. (Khwaza khela Branch Swat)

41

5.1.1.2 Current Ratio Current Assets/Current Liabilities 2011 1.107 2010 1.110 2011 42635217 Current Assets Current Liabilities 1 38517985 0 2010 394461394 355365842

Current Ratio(Rs in '000')

440000000 420000000 400000000 380000000 360000000 340000000 320000000 300000000

Current Asstes Current Laibilities

426352171

394461394 385179850

355365842

The Current ratio,

one of the most commonly cited financial ratios, measurers the firms ability to meet its short-term obligations. In the year 2010 the ratio is 1.110, while the following year it comes to 1.107

5.1.1.3 Cash Ratio Cash/Current Liabilities 2011 0.103 Cash Current Liabilities 2010 0.112 2011 39631172 38517985 0 2010 39683883 355365842

Cash Ratio (Rs in '000')

450000000 400000000 350000000 300000000 250000000 200000000 150000000 100000000 50000000 0 39631172

Cash

Current Laibilities

385179850 355365842

39683883

This ratio measures the ability of the firms to meet the current liability by its most liquid asset that is cash in hand. 5.1.2 TURN OVER RATIOS. 5.1.2.1 Assets Turn over Interest Revenue/Total Assets 2011 0.090 2010 0.077

Assets turn over Ratio (Rs in' 000')

Interest Revenue 500000000 450000000 400000000 350000000 300000000 250000000 200000000 150000000 100000000 50000000 0 40043824 31786595 44361590 4 Total Assets

41048551 7

Internship Report on Muslim Commercial Bank. (Khwaza khela Branch Swat)

42

Interest Revenue Total Assets

2011 40043824 44361590 4

2010 31786595 410485517

The Assets turn over ratio tells us the relative efficiency with which a firm utilizes its total assets to generate interest revenue. From the calculation above the ratio of MCB has shown improvement. 5.1.3 DEBT RATIO. 5.1.3.1 Total Debt Ratio Total Liabilities/Total Assets 2011 0.868 2010 0.866 2011 38517985 Total Liabilities Total Assets 0 44361590 4 2010 355365842 410485517

500000000 450000000 400000000 350000000 300000000 250000000 200000000 150000000 100000000 50000000 0 Total Debt Ratio (Rs in '000') Total Liabilities 443615904 385179850 355365842 Total Assets 410485517

The bebt ratio measures the proportion of total assets financed by the creditors. The high this ratio, the greater the amount of other peoples money being used in an attempt to generate profits. 5.1.4 PROFITABILITY RATIO

Gross Profit Margin (Rs in '000')

Gross Profit Interest Revenue

2011 28483084 40043824

2010 23921062 31786595

Gross Profit 45000000 40000000 35000000 30000000 25000000 20000000 15000000 28483084

Interest Revenve

40043824

5.1.4.1 Gross Profit Margin Goss Profit (Fund Based Income)/Interest Revenue 2011 71.130 2010 75.255

31786595 23921062

10000000 5000000 0

Internship Report on Muslim Commercial Bank. (Khwaza khela Branch Swat)

43

This ratios measure the percentage of each interest Rupee remaining after the firm has paid for its interest paid, the higher the gross profit margin, the better, and the lower the relative cost of merchandise sold. 5.1.4.2 Operating Profit Margin Operating Profit Margin Operating Profit/Interest Revenue*100 2011 64.648 2010 76.678

45000 40000 35000 30000 25000 25887 31786 24373 Operating Profit Margin (Rs in 'Millions') Operating Profit 40043 Interest Revenue

2011 2010 Operating Profit 25887 24373 Interest Revenue 40043 31786 Measures the percentage of each interest Rupee remaining after all costs and expenses other than

20000 15000 10000 5000 0

interest and taxes are deducted, the pure profits earned on each Interest Rupee. 5.1.4.3 Profit Before Tax Ratio Profit Before Tax/Total Income*100 2011 63.799 2010 70.164

40000 35000 30000 25000 20000 15000 10000 5000 0 21867 21308

Profit Before Tax Ratio ( Rs in 'Millions')

Net Profit Before Tax 34275 30369 Total Income

2011 2010 Net Profit Before Tax 21867 21308 Total Income 34275 30369 This ratio measures the amount of profit earned by the firm before the Tax. 5.1.4.4 Return on equity Net Profit after Tax/Owner's equity *100 2011 2010

Return on Equity (Rs in'000')

Net Profit After Tax Ow ner's Equity

60000000 50000000 40000000 30000000 20000000 10000000 0 15374600

52244865 45414158

15265562

Internship Report on Muslim Commercial Bank. (Khwaza khela Branch Swat)

44

29.43

33.61 2011 15374600 52244865 2010 15265562 45414158

Net Profit After Tax Owner's Equity

The return on equity measures the return earned on the owners investment in the firm. Generally the higher this return, the better off are the owners.

5.1.4.5 Return On Assets Net Profit After Tax/Total Assets*100 2011 3.466 Net Profit After Tax Total Assets 2010 3.719 2011 15374600 44361590 4 2010 15265562 410485517

500000000 450000000 400000000 350000000 300000000 250000000 200000000 150000000 100000000 50000000 0 15374600 15265562

Retun on Assets (Rs in '000')

Net Profit After Tax Total Assets

443615904

410485517

This ratio is also called return on investment, Measures the firms overall effectiveness in generating profits with its available assets, the time interest earned ratio, measures the firms ability to make contractual interest payments. The higher the value of this ratio, the better able the firm to fulfill its interest obligations.

5.1.4.7 Net Profit Margin Net Profit/ Interest Revenue 2011 2010

45000000 40000000 35000000 30000000 25000000 20000000 15000000 10000000 5000000 0

Net profit Margin (Rs in '000) Net Profit Interest Revenve

40043824

31786595

15374600

15265562

Internship Report on Muslim Commercial Bank. (Khwaza khela Branch Swat)

45

38.394

48.025 2011 1537460 2010 15265562 31786595

Net Profit Interest Revenue

0 4004382 4

The net profit margin measures the percentage of each Interest. The net profit margin measures the percentage of each interest Rupee remaining after all costs and expenses, including interest and taxes, have been deducted. The higher the firms net profit margin, the better the net profit margin will be. References: Annual Balance Sheet (Dec 31,2011) Of MCB. Gitman, Lawrence, J. 2001 Managerial Finance 9th Patparganj, Dehli India. Edition Chapter 4. James C. Van Horne & John M. Wachowicz, Jr. Fundamentals of

Financial Management.11th. Edition Chapter 6.

Internship Report on Muslim Commercial Bank. (Khwaza khela Branch Swat)

46

CHAPTER 6 SWOT ANALYSIS

MCB has some unique factors like being the oldest bank of the country, which adds to its value. Its foreign background and the look of multinational institutions create attraction for people. The formal SWOT analysis constitutes of four different solid parts. The SWOT analysis comprise of the strengths it has, the weaknesses that are a part of it, the opportunities that it can exploit and the threats it faces from competitors. However it also encompasses generally the Khwaza khela Branch. Certain factors are already attached with the name of MCB, whose benefit or loss is automatically the part of MCB Khwaza khela Branch.

6.1

STRENGTHS

MCB benefit from a few points which ultimately makes its backing strengthened. Some of these points are as follows: Owned by very strong financial group (Mansha Group) The largest private sector bank in Pakistan with a network of 1047 branches domestically and 7 foreign branches and 01 E P Z. Since MCB is one of the oldest banks in Pakistan it started its operation in 1947 so it has sufficient operation experience. First bank to privatize which has now became the leader in market with the largest on-line and ATM network in country.

Internship Report on Muslim Commercial Bank. (Khwaza khela Branch Swat)

47

Sole provider of mobile banking. Bank emphasis on consumer needs and demands which is ensured in the branches through the Quality Service Assurance (QSA) department of the bank. MCB emphasis on the extension and improvement in service. Attractive and high rate of interest. Best and optional policies and attractive compensation packages for employees. Human Resource development and employment of new An efficient and experienced group of management. Easy access to the customers at their residential localities through large network of branches.

6.2

WEAKNESSES

Weaknesses, like strengths are a part of almost every organization. These weaknesses points out the potential areas of improvements and make the organizational behavior intelligent. A cumulative effort to overcome these flaws makes success possible. During the internship period the weaknesses that generally surfaced and were visible at MCB Khwaza khela Branch are described below. Slow down in advance growth in the short term as MCB focuses on quality customers in the market. Customers having accounts of small amount are not given the same services and dealing given to those of high amount. MCB keep on increasing the numbers of branches while the numbers of employee are not at the same pace which has lead to the shortage of employees. Unrest among employees due to continuous changes in the employees policies from management.

Internship Report on Muslim Commercial Bank. (Khwaza khela Branch Swat)

48

Managing group is also having huge investment in other sector like textile and cement industry etc, which may divide their attention.

6.3 OPPORTUNITIES

Success, more than anything is all about converting into opportunity what everybody else considers danger Opportunities, when exploited properly reap profits and earn success. They are almost always a matter of time. They are to be sought, picked and made use of, before any body else gets up and do so. Due to largest ATM network, MCB can expend its 24 hours cash facilities to other cities of the country in order to meet the growing market demand. Increasing focus/target on different types of customers MCB can open women branches especially in those areas where women class want to get involved but could not due to environmental restrictions. Growing policies of government on business and commerce sectors provides MCB an opportunity to efficiently meet with the businessmens requirements of instant cash and financing facilities. To further expend its branch network in business territories. MCB also has an opportunity to expend it new technological advancement like tele bank and online banking facilities in order to serve the customers more efficiently. To increase the number of branches in forging countries.

6.4 THREATS

Threats are the unseen, futuristic, probable events that can occur and prove dangerous in consequences. Every organization is faced by some

Internship Report on Muslim Commercial Bank. (Khwaza khela Branch Swat)

49

category of threats in its operations and functions. Opening new outlets, altering existing policies, designing fresh marketing strategies, bringing change in physical structure, almost every activity that an organization does, it faces some kind of threats, just like the benefits it seeks. MCB also faces some threats which can just prove minor assumed fears; as well as can become events with grave consequences. The prevailing condition indicates the following as the possible threats. Inconsistency in governments policies regarding to business and economic sector. Growing global technological advancement. Strict regulation by the government over credit facilities to the customers as well as meet the Prudential Regulation as by the SBP. Loss of confidence of prospective customers due to freezing of accounts in the past by the government. References: Gitman, Lawrence, J. 2001 Managerial Finance 9th Patparganj, Dehli India. Edition Chapter 4. James C. Van Horne & John M. Wachowicz, Jr. Fundamentals of

Financial Management 11th Edition Chapter 6.

Ahmad Zeeshan, Report On MCB, MBA (F), Session 2006-2011.

Internship Report on Muslim Commercial Bank. (Khwaza khela Branch Swat)

50

CHAPTER 7 FINDINGS AND RECOMMENDATIONS

Since the name and icon of MCB stands for sign of trust and reputation that is why the number of customers of MCB is growing day by day. Analyzing the banks performance in several departments and evaluating the strengths and weaknesses leads to some proposals. There are certain rooms of improvement which has been found during the period of internship.

1.

There Are Always Long Queues On The Cash Counter.

In MCB Khwaza khela branch there are long lines from the very beginning of day. At the cash counter the customers are some times starts to speak harsh wording due to the turning of numbers of each customers.

2.

The Attitude Of Employees Is Not Customers

Oriented.

In marketing it said that the customer is the king, and must be obeyed. But this concept is not used in the branch, the staff of the branch do not know any thing about the value of customer, however only the customers having huge balance is given the due attention.

3.

No Proper Setting Arrangement For Customers.

The setting arrangement is important for both the employees and for the customers as well. Often it was visible that during peak banking hours many customers use to stand anywhere they wanted to. This creates stress for the employees as well as for the customers.

Internship Report on Muslim Commercial Bank. (Khwaza khela Branch Swat)

51

4.

Technology Incorporated Is Not Up To Date.

Technology plays a crucial role in the present age, the technology used in the branch is not up to date the employees still working on the old computers, the internet connection which is used for the online transaction is the old dial up connection, which should be the Digital Subscriber Line (DSL).

5.

Insufficient Staff.

Another serious problem at the branch is the scarcity of staff, the staff working in the branch is enough as compare to any other branch but if we glance over the number of customers and the location of branch the staff is scare.

6.

No Formal Training And Development Program.

The MCB claims of training and educating its employees but practically speaking it should initiate a good employee training and development plan. This would help employees to know more about their specific job and its actual requirements.

7.

Employees Are Given Hard Targets.

Targets which are given to the employees should be in such a way that it can be accessible, but normally it has been observed that hard targets are given to the employees and are asked to be achieve in a short span of time.

8. Whole Concentration Is On The Upper Class Customers Only.

The whole concentration of the staff remains on the customers having huge amount of balance, while the customers having less amount in their accounts are neglected.

9. Employees Are Over Loaded.

Internship Report on Muslim Commercial Bank. (Khwaza khela Branch Swat)

52

The employees of the entire working department in the branch are over loaded, even any employee can not take a leave of a single day. 10. (ICU). In MCB the employees are tortured by the unit, if the member of the unit finds any error in the working of any employee, the employee is given a charge sheet, and is asked for explanation, and after that the case is hand over to the enquiry committee for further procedure, so this is a long way process and creates unrest among employees. Advice is seldom welcome and those who want it the most always like it the least Recommendations suggest improvements in areas which have room for polishing and progress. Criticizing several factors at MCB Khwaza khela Branch does not mean that these aspects are permanent flaws of the branch. Instead, it is intended that these mistakes be removed. For the confiscation of these errors, certain recommendations are forwarded. Employees Are Tortured By The Internal Control Unit

1. QUEUING MODELS FOR CASH COUNTERS

The long queues at cash counter give an awkward look. This problem can be solved by using the Queuing Model concept. These models are proposed to facilitate organizations control waiting lines. Through this approach, the bank can decide the best possible number of checkout stands. The number of checkouts should balance personnel cost and customer waiting time.

2. CUSTOMER ORIENTED ATTITUDE

The bank staff should be properly educated about the customers value. The bank should use the marketing approach, and customer satisfaction

Internship Report on Muslim Commercial Bank. (Khwaza khela Branch Swat)

53

should be taken into account. There should be no status discrimination between customers. The bank staff should be courteous to all customers. A customer is fascinated and brings other customers also to the bank if the service is efficient and courteous.

3. PROPER SEATING ARRANGEMENT

Customers, waiting for their turns, should be provided with proper seating arrangements. Often it was visible that during peak banking hours many customers use to stand anywhere they wanted to. This created stress for the employees as well as other customers waiting for their job getting done. A specific place should be reserved for the customers by placing chairs there. The staff should politely tell the customers to be seated till their work is ready. This would ease the job of the employees as well as clients wont bear the pain of being standing still and waiting.

4. INSUFFICIENT STAFF

Another crucial problem in MCB is the scarcity of staff, all the branches of MCB are over loaded due to high customers attractiveness, which not only create problem for the customers but also for the existence staff, while the quality and fairness of work is also affected. So MCB should hire more staff in order to cope with the issue, for this issue short and long term plan which has been given in the implementation plan may be used.

5. TRAINING AND DEVELOPMENT PROGRAM

The MCB claims of training and educating its employees but practically speaking it should initiate a good employee training and

Internship Report on Muslim Commercial Bank. (Khwaza khela Branch Swat)

54

development plan. This would help employees to know more about their specific job and its actual requirements.

7. PERFORMANCE APPRAISAL

The practice of performance appraisal should be made a serious and mature process which can identify an employees potential accurately. Giving unachievable tasks to employees discourages them and they dont strive for the achievements of those tasks. If targets which are practical given to employees and any bonus or reward are announced on the achievements, this would greatly influence the performance of employees. It can be possible only then that the employees will take their performance appraisal serious and would yearn for betterment.

8. MARKET SEGMENTATION

The general target market of MCB is the upper class of the society. The sales force is often busy in looking at probable clients with large amount of money. It can also prove costly when sometimes another potential customers gets deviated because of the less attention paid to him. Also concentration in one market segment bears high risk and can lead to huge losses if a deposit is withdrawn. The bank should also offer some products for potential customers with comparatively lowincome level. Most of the potential customers cannot fulfill the high balance requirements and high service charges. Bank should revise its policies on charges for services it provides. This will result in more satisfied and trustworthy relationship between clients and employees.

9. EQUITY CONCEPT

All the departments should be given with an equivalent load of work this would result in a friendly relation among employees as well as it

Internship Report on Muslim Commercial Bank. (Khwaza khela Branch Swat)

55

will boost the coordination between different departments. Another suggestion would be that the staff should be involved in the decision making process. So that they can make arguments about their status of work after accepting the new responsibilities. This would also clarify the issue between staff members and responsibilities and authorities will be properly delegated, resulting in the ending of the confusions about work and responsibilities. It would also give a feeling of own ness and security to the workforce of being very much a part of the bank.

10. FAIR INTERNEE SELECTION PROGRAM

A fair internees selection system should be established for selection of internees. Instead of sending CVs to Karachi Head Office, the applicants should be interviewed locally in the branch on some specific date. Aptitude and competence of the candidates should be considered a merit for selection instead of their references. Bank administration should give proper training to the internees. They should educate them about the purpose of all the functions they perform. MCB also give internship generally for six weeks and for the maximum of eight weeks. This is a problem for MCB itself. Thus during the six or eights weeks duration when an internee gets some know how about the banks operation, his/her time completes; and when he/she can be more useful than ever, he/she is asked to leave. If MCB increases its internship period for a quota of seats, it will help MCB in taking much use of internees it trains for work. MCB also does not pay any stipend to the internees, which lead to discouragement among the internees.

11. EMPLOYEES ARE TORTURED BY THE ICU.

The main job of the Internal Control Unit (ICU) is to ensure error less work in a branch. This unit critically checks the routine activities of a

Internship Report on Muslim Commercial Bank. (Khwaza khela Branch Swat)

56

branch on monthly basis. The recommendation for this finding is that if the ICU finds any error/ mistake it should be rectified on the spot instead creating such a big issue which create un rest among employees. References 1. Interview with the employees and personal observation.

Internship Report on Muslim Commercial Bank. (Khwaza khela Branch Swat)

57

CHAPTER 8 IMPLEMENTATION PLAN

Analyzing the banks performance in several departments and evaluating the strengths and weaknesses leads to some proposals. The implications of these suggestions are more important issue. MCB Khwaza khela Branch is generating profits and is targeting the market efficiently with its energetic management. Its location at the centre of business sector in Peshawar city is also adding to its easy accessibility by customers. Thus the outlook requirements of the bank are almost complete. The place for improvement in the bank is inside. The underlying problem of several other problems that was observed during the internship period was that MCB Khwaza khela Branch is and understaffed bank. It has enough vacant room for new employees. This hitch is the root cause of many other problems. Considering the prevailing circumstances at MCB Khwaza khela Branch and taking a broad overview of the possible solution, one would surely come up with the idea of employing fresh energetic workers. This would root out the above mentioned problems. Additionally an employee in the cash department would lessen the burden of the already working tellers as well as it would help in the reduction of long queues at the cash counter.

IMPLEMENTATION PLAN

Thus now when the basic area of problem is identified, the understaffing, several measures can be taken into account to deal with

Internship Report on Muslim Commercial Bank. (Khwaza khela Branch Swat)

58

this problem. There are two plans which are suggested for dealing for this problem. 8.1 8.2 Short Term Plan Long Term Plan

8.1

SHORT TERM PLAN

The short term plan is devised for employees who would be given the chance to serve in the bank for a limited period. This can be done in the following two methods. a: Longer Duration Internship Program The bank normally offers a 6 weeks internship program. At the maximum this duration stretches to 8 weeks. During this period the employees of the bank helps the internees to understand various procedures regarding different departments. After the coaching and teaching of these 6 or 8 weeks the internee is able to comprehend most of the functions of the bank and he or she is able to follow the appropriate procedure which is to be followed for the completion of that function. The bank can introduce a long internship program for its own benefit as well as these graduates. To keep the normal internees unaffected, it can reserve a special quota for these kinds of long duration internees. The selection can be made in the local branches. To get good recommendation on this kind of a report the applicant will be motivated and will work hard. This will help him in getting experience as well knowledge about the delicacies of practical job. Most of the organization requires earlier experience in the field, thus MCB can be helpful in developing the youth into a positive direction as well. Since the name of MCB already means trust, this will build many peoples career in good organizations. The bank will benefit in the shape of obtaining a motivated and energetic employee and that also at a lesser

Internship Report on Muslim Commercial Bank. (Khwaza khela Branch Swat)

59

cost than the normal employees. The cost would be less because since these would be fresh graduates seeking experience and recommendation, hence they can take as internees. b: Contract Workers

The bank can also employ contract workers also. If the bank wants to be careful in choosing a better lot among the pool of candidates for its operations, it can offer contract seats. Contracts seats will be for applicants who will be employed on contract basis. This program will be different than the long internship program as the above program will be just meant for fresh graduates and new applicants who will get recommendation and will be paid the internees stipend..

8.2

LONG TERM PLAN

The long term plan would be designed for the permanent employees of the bank, so that they can prove beneficial to the bank in future. This program would include picking up the most competent employee amongst the employees and sending him/her for further training and higher studies about the bank policies. Now the question arises that how can an employee be of any use to solve the problem of understaffing. The answer is that a more efficient, able, experienced and motivated employee can handle the job of several persons. The bank can make the selection amongst the employees on the basis of the performance the employees show and on achieving targets. When the selection about an employee is made, thus he/she will be send for a period of time to get training and education. More emphasis is to be given to the sensitivities and delicacies involved in the operations of different functions. He/she would be taught specifically the policies about the bank, the broader goal the bank want to achieve and the ways of cumulative efforts that are required.

Internship Report on Muslim Commercial Bank. (Khwaza khela Branch Swat)

60