You might also like

- The Campaigner - There Are No Lone Assassins (July 1981)Document69 pagesThe Campaigner - There Are No Lone Assassins (July 1981)Elder Futhark100% (1)

- Sport Facility Operations ManagementDocument298 pagesSport Facility Operations ManagementElder Futhark100% (2)

- American Institutional Penetration Into Greek Military & Political Policymaking Structures (June 1947-October 1949)Document25 pagesAmerican Institutional Penetration Into Greek Military & Political Policymaking Structures (June 1947-October 1949)Elder FutharkNo ratings yet

- Stabilization, Debt and IMF Intervention - Development Trade-Offs in Ecuador and PeruDocument11 pagesStabilization, Debt and IMF Intervention - Development Trade-Offs in Ecuador and PeruElder FutharkNo ratings yet

- China Naval Modernization - Implications For U.S. Navy Capabilities (2011)Document75 pagesChina Naval Modernization - Implications For U.S. Navy Capabilities (2011)Elder FutharkNo ratings yet

- PreSocratic Greek PhilosophyDocument25 pagesPreSocratic Greek PhilosophyAngelo Shaun Franklin0% (1)

- Who Gains From Growth - Living Standards in 2020 (Resolution Foundation)Document56 pagesWho Gains From Growth - Living Standards in 2020 (Resolution Foundation)Elder FutharkNo ratings yet

- The Clash of Civilizations (S.P. Huntington 1993)Document28 pagesThe Clash of Civilizations (S.P. Huntington 1993)Elder FutharkNo ratings yet

- The Methodology of Mass DestructionDocument25 pagesThe Methodology of Mass DestructionElder FutharkNo ratings yet

- Firearms - Final - 05-2013 Pew Research CenterDocument63 pagesFirearms - Final - 05-2013 Pew Research Centerwolf woodNo ratings yet

- Civil-Military Relations (Greece & Turkey)Document81 pagesCivil-Military Relations (Greece & Turkey)Elder FutharkNo ratings yet

- Napoleon S Nightmare - Guerrilla Warfare in Spain (1808-1814)Document25 pagesNapoleon S Nightmare - Guerrilla Warfare in Spain (1808-1814)Elder FutharkNo ratings yet

- The Situation of Freedom of Expression - Turkey and The EUDocument43 pagesThe Situation of Freedom of Expression - Turkey and The EUElder FutharkNo ratings yet

- War Powers Resolution - Presidential ComplianceDocument29 pagesWar Powers Resolution - Presidential ComplianceElder FutharkNo ratings yet

- Osama Bin Laden File02Document2 pagesOsama Bin Laden File02Paul CokerNo ratings yet

- Russia's Syrian Stance - Principled Self-Interest (Sept-2012)Document4 pagesRussia's Syrian Stance - Principled Self-Interest (Sept-2012)Elder FutharkNo ratings yet

- The American Army in The BalkansDocument54 pagesThe American Army in The BalkansElder FutharkNo ratings yet

- Global Counterinsurgency - Strategic Clarity For The LongWar (DANIEL S. ROPER)Document17 pagesGlobal Counterinsurgency - Strategic Clarity For The LongWar (DANIEL S. ROPER)Elder FutharkNo ratings yet

- The Concept of Anomic Suicide For Introductory Sociology CoursesDocument23 pagesThe Concept of Anomic Suicide For Introductory Sociology CoursesElder Futhark100% (1)

- The IMF, The World Bank, and U.S. Foreign Policy in Ecuador, 1956-1966Document34 pagesThe IMF, The World Bank, and U.S. Foreign Policy in Ecuador, 1956-1966Elder FutharkNo ratings yet

- Minorities in Turkey - Nigar Karimova and Edward Deverell (2001)Document24 pagesMinorities in Turkey - Nigar Karimova and Edward Deverell (2001)Elder FutharkNo ratings yet

- Deterring Iran - 1968-1971 - The Royal Navy, Iran, and The Disputed Persian Gulf IslandsDocument13 pagesDeterring Iran - 1968-1971 - The Royal Navy, Iran, and The Disputed Persian Gulf IslandsElder FutharkNo ratings yet

- RUSSIA 2010 & What It Means For The WorldDocument348 pagesRUSSIA 2010 & What It Means For The WorldElder FutharkNo ratings yet

- Ethnic Kurds, Endogenous Identities, and Turkey's DemocratizationDocument20 pagesEthnic Kurds, Endogenous Identities, and Turkey's DemocratizationElder FutharkNo ratings yet

- Financial Crisis in The European Union - The Cases of Greece and Ireland (2011)Document85 pagesFinancial Crisis in The European Union - The Cases of Greece and Ireland (2011)Elder FutharkNo ratings yet

- Gestalt PsychologyDocument188 pagesGestalt PsychologyElder FutharkNo ratings yet

- The Ugly Truth About Milton Friedman - Nancy SpannausDocument2 pagesThe Ugly Truth About Milton Friedman - Nancy SpannausElder Futhark100% (1)

- Quadrennial Defense Review Report 2006Document113 pagesQuadrennial Defense Review Report 2006phegleydNo ratings yet

- Global Security Concerns - Anticipating The 21st CenturyDocument231 pagesGlobal Security Concerns - Anticipating The 21st CenturyElder FutharkNo ratings yet

- United States Strategic Bombing Survey - Japan's Struggle To End The WarDocument59 pagesUnited States Strategic Bombing Survey - Japan's Struggle To End The WarElder FutharkNo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (894)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Emaar Economic City: Dubai On The Red SeaDocument46 pagesEmaar Economic City: Dubai On The Red SeaHarsh JaswaniNo ratings yet

- Email AdresseDocument35 pagesEmail AdresseBdirinabdirina MiloudNo ratings yet

- 2023 Saudi State of Fashion Report-2Document72 pages2023 Saudi State of Fashion Report-2Chloe M ZizianNo ratings yet

- Project Failure Factors and Their Impact On The Performance of Construction Projects in The Oil & Gas Industry in Saudi ArabiaDocument99 pagesProject Failure Factors and Their Impact On The Performance of Construction Projects in The Oil & Gas Industry in Saudi ArabiaABDULAZIZ DAIFALLANo ratings yet

- Current account statement in Saudi RiyalsDocument6 pagesCurrent account statement in Saudi RiyalsSyedFarhanNo ratings yet

- Lista de Descarga MSK - Sea MV Maersk Newcastle 242N Dep CrcalDocument28 pagesLista de Descarga MSK - Sea MV Maersk Newcastle 242N Dep CrcalAndrea MuñozNo ratings yet

- New Microsoft Excel WorksheetDocument16 pagesNew Microsoft Excel Worksheetoday bakour2No ratings yet

- Information About All CompaniesDocument11 pagesInformation About All Companiesرفال الجهنيNo ratings yet

- Economic and Investment Monitor Q1 2023 EnglishDocument57 pagesEconomic and Investment Monitor Q1 2023 EnglishNirmal MenonNo ratings yet

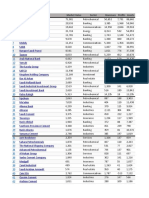

- Top 100 Saudi CompaniesDocument12 pagesTop 100 Saudi CompaniesMurad Al AliatNo ratings yet

- GBE Report On Apparel Retailing in Saudi ArabiaDocument56 pagesGBE Report On Apparel Retailing in Saudi ArabiaNikita Sanghvi100% (1)

- Updated Company Emails Saudi ArabiaDocument1 pageUpdated Company Emails Saudi Arabiaget.aishaaNo ratings yet

- Globalization Impacts in Saudi ArabiaDocument4 pagesGlobalization Impacts in Saudi ArabiaFaisal Al HumaidanNo ratings yet

- Also SeeDocument4 pagesAlso SeeMustafa Kaizan100% (1)

- Hotel Sector of Saudi ArabiaDocument17 pagesHotel Sector of Saudi Arabiamaliwal123No ratings yet

- Resilience of Saudi Arabia's Economy To Oil Shocks - Effects of Economic ReformsDocument48 pagesResilience of Saudi Arabia's Economy To Oil Shocks - Effects of Economic ReformsAtif KhanNo ratings yet

- Aramco Direct Indirect P.O Log at BFIMDocument10 pagesAramco Direct Indirect P.O Log at BFIMrhnscalNo ratings yet

- KFUPMDocument54 pagesKFUPMahmedhamdiNo ratings yet

- SaudiDocument52 pagesSaudiTarun AggarwalNo ratings yet

- Water Job List-Nov-2016Document27 pagesWater Job List-Nov-2016Sekhil DevNo ratings yet

- Business EnvironmentDocument54 pagesBusiness EnvironmentAbdulaziz HbllolNo ratings yet

- Saudi Saipem Rig MovesDocument13 pagesSaudi Saipem Rig MovesTahir Iqbal. Kharpa RehanNo ratings yet

- The IPO of Saudi Aramco Some Fundamental Questions OIES Energy InsightDocument10 pagesThe IPO of Saudi Aramco Some Fundamental Questions OIES Energy InsightsamNo ratings yet

- Franchising andDocument11 pagesFranchising andmohhmameddNo ratings yet

- Panda and Hyper Panda LeafletDocument32 pagesPanda and Hyper Panda Leafletblack2night100% (2)

- SME in SaudiDocument9 pagesSME in Saudiabusaleh33No ratings yet

- Project ProposalDocument9 pagesProject Proposalmoses chegeNo ratings yet

- Saudi IT CompaniesDocument3 pagesSaudi IT CompaniesNasir MalikNo ratings yet

- JLL Real Estate Market Overview Ksa q1 2020Document6 pagesJLL Real Estate Market Overview Ksa q1 2020faisalNo ratings yet

- Financial Sector Development Program Delivery PlanDocument100 pagesFinancial Sector Development Program Delivery PlanHadeel NoorNo ratings yet