You might also like

- 2015 Dodge Ram Cab Lights Installation 82211190ABDocument7 pages2015 Dodge Ram Cab Lights Installation 82211190ABmt11280% (1)

- Proteccion Contra Sobretensiones PDFDocument84 pagesProteccion Contra Sobretensiones PDFgilbertomjcNo ratings yet

- Libro1 (Autoguardado)Document6 pagesLibro1 (Autoguardado)Ricardo Evaristo QuispeNo ratings yet

- HCMC Market Presentation Q3 2010 - enDocument42 pagesHCMC Market Presentation Q3 2010 - enmaykidNo ratings yet

- Lmo Io 390 A1a6Document407 pagesLmo Io 390 A1a6Daniel MkandawireNo ratings yet

- Actividades Del Día:: Reporte Diario de AvanceDocument2 pagesActividades Del Día:: Reporte Diario de Avancederwin huertaNo ratings yet

- Milestone Report: Late Milestones Milestones Up Next Completed MilestonesDocument1 pageMilestone Report: Late Milestones Milestones Up Next Completed MilestonesAlexandru BaciuNo ratings yet

- Actividades Del Día:: Reporte Diario de AvanceDocument2 pagesActividades Del Día:: Reporte Diario de Avancederwin huertaNo ratings yet

- New Microsoft Office Power Point PresentationDocument31 pagesNew Microsoft Office Power Point PresentationReshma GuptaNo ratings yet

- Actividades Del Día:: Reporte Diario de AvanceDocument2 pagesActividades Del Día:: Reporte Diario de Avancederwin huertaNo ratings yet

- Defiance Cap - The Week That Just Passed Mar 19, 2010Document6 pagesDefiance Cap - The Week That Just Passed Mar 19, 2010WallstreetableNo ratings yet

- Actividades Del Día:: Reporte Diario de AvanceDocument2 pagesActividades Del Día:: Reporte Diario de Avancederwin huertaNo ratings yet

- The Oil Market Through The Lens of The Latest Oil Price CycleDocument22 pagesThe Oil Market Through The Lens of The Latest Oil Price CycleAnkit BirharuaNo ratings yet

- Actividades Del Día:: Reporte Diario de AvanceDocument2 pagesActividades Del Día:: Reporte Diario de Avancederwin huertaNo ratings yet

- SUBSEA 7 SA (Oil & Gas Services & Equip) : Earnings & Estimates Market DataDocument1 pageSUBSEA 7 SA (Oil & Gas Services & Equip) : Earnings & Estimates Market DataSahil GoelNo ratings yet

- Relationship Between Gold Price and Crude Oil Price With Respect To Current Economic SituationDocument13 pagesRelationship Between Gold Price and Crude Oil Price With Respect To Current Economic SituationGenga EswariNo ratings yet

- GraphsDocument3 pagesGraphsJohn Paul GroomNo ratings yet

- Reza SiregarDocument35 pagesReza SiregarKhoirul AnwarNo ratings yet

- Final Porfolio PaperDocument15 pagesFinal Porfolio PaperDeep DualNo ratings yet

- Nyse MS 2002Document28 pagesNyse MS 2002Gautam TandonNo ratings yet

- Key Number Community 1 Cahto Tribe of The Laytonville Rancheria 2 Sherwood Valley Rancheria of Pomo Indians 3 Round Valley Indian TribesDocument1 pageKey Number Community 1 Cahto Tribe of The Laytonville Rancheria 2 Sherwood Valley Rancheria of Pomo Indians 3 Round Valley Indian TribesmongoNo ratings yet

- Actividades Del Día:: Reporte Diario de AvanceDocument2 pagesActividades Del Día:: Reporte Diario de Avancederwin huertaNo ratings yet

- Metabo SBE 660 SBE 750 ManualDocument36 pagesMetabo SBE 660 SBE 750 ManualdinescNo ratings yet

- Template - Trends - Loop9 JUN 2016 (TOC)Document1 pageTemplate - Trends - Loop9 JUN 2016 (TOC)designselvaNo ratings yet

- FRP Pipe Supports, Anchors and GuidesDocument8 pagesFRP Pipe Supports, Anchors and Guidesgerardo herrera valenzuelaNo ratings yet

- CAT Formulas Masterbook SummaryDocument60 pagesCAT Formulas Masterbook SummaryPallabh BhuraNo ratings yet

- AlphaBets Investor Letter - October 2018Document5 pagesAlphaBets Investor Letter - October 2018Anish TeliNo ratings yet

- Strengthening Stability, Maintaining GrowthDocument17 pagesStrengthening Stability, Maintaining GrowthBella FeliciaNo ratings yet

- Darren Weekly Report 47Document6 pagesDarren Weekly Report 47DarrenNo ratings yet

- GDP: Growth: Real GDP: Yoy: Select This Link and CLDocument6 pagesGDP: Growth: Real GDP: Yoy: Select This Link and CLadityaNo ratings yet

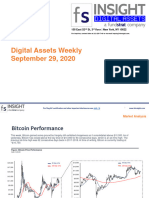

- FSIDigitalAsset WeeklyDocument15 pagesFSIDigitalAsset WeeklyabidzarrNo ratings yet

- 2015 Dodge Ram Cab Lights Installation 82211190ABDocument7 pages2015 Dodge Ram Cab Lights Installation 82211190ABhansenfarms.chNo ratings yet

- Vol 25, Issue No 16, DataBankDocument32 pagesVol 25, Issue No 16, DataBankSenthil KumarNo ratings yet

- Sustainability 12 08142 v2Document12 pagesSustainability 12 08142 v2Bahiru BelachewNo ratings yet

- General Schematic - CR30-XDocument9 pagesGeneral Schematic - CR30-XPatou PatriceNo ratings yet

- Contract DocumentDocument45 pagesContract DocumentEngineeri TadiyosNo ratings yet

- Cross Asset Technical VistaDocument20 pagesCross Asset Technical VistaanisdangasNo ratings yet

- SN13134 SDDocument6 pagesSN13134 SDrigono1664No ratings yet

- Performance (Net) : Lakefront PartnersDocument6 pagesPerformance (Net) : Lakefront Partnersfindgood100% (2)

- Commodity Chartbook 20101028Document8 pagesCommodity Chartbook 20101028andrewbloggerNo ratings yet

- Global Markets MinesweeperDocument4 pagesGlobal Markets MinesweeperanisdangasNo ratings yet

- For Web - Economic Survey 2075 Full Final For WEB - 20180914091500 PDFDocument286 pagesFor Web - Economic Survey 2075 Full Final For WEB - 20180914091500 PDFIsmith PokhrelNo ratings yet

- MCA Trend Assistant 32171300a-EnDocument5 pagesMCA Trend Assistant 32171300a-EnFábio LeiteNo ratings yet

- Area Yield ProductionDocument26 pagesArea Yield ProductionmumbaideepikaNo ratings yet

- CIMB-Principal Bond FundDocument2 pagesCIMB-Principal Bond FundAnonymous EA18Sp3Y0No ratings yet

- Watch CabinetDocument29 pagesWatch CabinetBán ZoltánNo ratings yet

- Research Speak 25-6-2010Document12 pagesResearch Speak 25-6-2010A_KinshukNo ratings yet

- Cross Asset: Technical VistaDocument18 pagesCross Asset: Technical VistaanisdangasNo ratings yet

- MSV-2 Storm Valve DrawingDocument4 pagesMSV-2 Storm Valve DrawingEdwin DamasenaNo ratings yet

- Proyecto FinalDocument5 pagesProyecto FinalHéctor MontoyaNo ratings yet

- SR&ED Work Schedule Associated R&D Dec 10 08Document4 pagesSR&ED Work Schedule Associated R&D Dec 10 08metroroadNo ratings yet

- Stud Dimension-150 Rating FlangesDocument2 pagesStud Dimension-150 Rating FlangesVijay Kumar SinghNo ratings yet

- Generic Project Plan Template On ExcelDocument3 pagesGeneric Project Plan Template On Excelsmtdrkd100% (36)

- Catalog - Full SoportesDocument14 pagesCatalog - Full SoportesWERNER SILVA ALVAREZNo ratings yet

- Quiz 4Document28 pagesQuiz 4Ray Allen Bionson RomeloNo ratings yet

- RSAT A-D AnswersDocument20 pagesRSAT A-D AnswersZa KiraNo ratings yet

- Bonds 2 Questions UweDocument1 pageBonds 2 Questions UweAshok ShresthaNo ratings yet

- Modificado 1Document1 pageModificado 1YENEF KENEDY SOTO SOLANONo ratings yet

- Contac T Custome R Asset Schedule Paymenthi S Insurance Recipien T Logs History OthersDocument2 pagesContac T Custome R Asset Schedule Paymenthi S Insurance Recipien T Logs History OthersKastepa DepariNo ratings yet

- The Stock Market in MarchDocument2 pagesThe Stock Market in MarchJohn Paul GroomNo ratings yet

- Aspects of the Dialogical Self: Extended proceedings of a symposium on the Second International Conference on the Dialogical Self (Ghent, Oct. 2002), including psycholonguistical, conversational, and educational contributionsFrom EverandAspects of the Dialogical Self: Extended proceedings of a symposium on the Second International Conference on the Dialogical Self (Ghent, Oct. 2002), including psycholonguistical, conversational, and educational contributionsMarie C BertauNo ratings yet

- Vectors FoundationDocument8 pagesVectors FoundationNaning RarasNo ratings yet

- Engineering Aspects of Food Emulsification and HomogenizationDocument325 pagesEngineering Aspects of Food Emulsification and Homogenizationfurkanturker61No ratings yet

- WPS Ernicu 7 R1 3 6 PDFDocument4 pagesWPS Ernicu 7 R1 3 6 PDFandresNo ratings yet

- Brosur Sy135cDocument9 pagesBrosur Sy135cDenny KurniawanNo ratings yet

- Personal Care Na Hair GuideDocument8 pagesPersonal Care Na Hair GuideIsabellaNo ratings yet

- Chinkon Kishin - Origens Shintoístas Do Okiyome e Do Espiritismo Na MahikariDocument2 pagesChinkon Kishin - Origens Shintoístas Do Okiyome e Do Espiritismo Na MahikariGauthier Alex Freitas de Abreu0% (1)

- M700-70 Series Programming Manual (M-Type) - IB1500072-F (ENG)Document601 pagesM700-70 Series Programming Manual (M-Type) - IB1500072-F (ENG)Mert SertNo ratings yet

- Psychoacoustics: Art Medium SoundDocument3 pagesPsychoacoustics: Art Medium SoundTheodora CristinaNo ratings yet

- Final Project Proposal Digital Stopwatch-1Document6 pagesFinal Project Proposal Digital Stopwatch-1Shahid AbbasNo ratings yet

- Your Song RitaDocument1 pageYour Song Ritacalysta felix wNo ratings yet

- MS-MS Analysis Programs - 2012 SlidesDocument14 pagesMS-MS Analysis Programs - 2012 SlidesJovanderson JacksonNo ratings yet

- General Science EnvironmentDocument28 pagesGeneral Science EnvironmentHamza MujahidNo ratings yet

- ElectrochemistryDocument24 pagesElectrochemistryZainul AbedeenNo ratings yet

- Exercise Questions (Materials) .: BFT 112 Introduction To EngineeringDocument1 pageExercise Questions (Materials) .: BFT 112 Introduction To EngineeringSK DarsyanaaNo ratings yet

- FINS 2624 Quiz 2 Attempt 2 PDFDocument3 pagesFINS 2624 Quiz 2 Attempt 2 PDFsagarox7No ratings yet

- Real Talk GrammarDocument237 pagesReal Talk GrammarOmar yoshiNo ratings yet

- Biology Standard XII Human Reproduction WorksheetDocument10 pagesBiology Standard XII Human Reproduction WorksheetPriya SinghNo ratings yet

- Adobe Scan 12 Aug 2022Document3 pagesAdobe Scan 12 Aug 2022surabhi kalitaNo ratings yet

- Making Soap From WoodDocument6 pagesMaking Soap From WoodmastabloidNo ratings yet

- Poisoning: Selenium in LivestockDocument4 pagesPoisoning: Selenium in Livestockdianarbk otuNo ratings yet

- Koh Pich Construction Company Cambodia-China Polytechnic University Daily Activities ReportDocument7 pagesKoh Pich Construction Company Cambodia-China Polytechnic University Daily Activities ReportNhoek RenNo ratings yet

- Specification IC DK112Document10 pagesSpecification IC DK112ROlando EskadabaichoNo ratings yet

- RLCraft v2.9 ChangelogDocument28 pagesRLCraft v2.9 ChangelogSơn TrươngNo ratings yet

- Etabloc Technical DataDocument108 pagesEtabloc Technical Dataedward ksbNo ratings yet

- Filtros MaquinasDocument34 pagesFiltros MaquinasAndres AlfonzoNo ratings yet

- Eb4069135 F enDocument13 pagesEb4069135 F enkalvino314No ratings yet

- Divide and Conquer (Closest Pair, Convex Hull, Strassen Matrix Multiply) DemoDocument27 pagesDivide and Conquer (Closest Pair, Convex Hull, Strassen Matrix Multiply) DemoAnand KumarNo ratings yet

- Student Pilot GuideDocument13 pagesStudent Pilot GuideAŞKIN FIRATNo ratings yet

- Module 1 Introduction To Ecology and The BiosphereDocument38 pagesModule 1 Introduction To Ecology and The BiosphereFrancis Rey Bactol PilapilNo ratings yet