You might also like

- Wastebook 2014 (Print)Document114 pagesWastebook 2014 (Print)ThePoliticalHatNo ratings yet

- Who Ebola 15 Oct 2014Document12 pagesWho Ebola 15 Oct 2014thecynicaleconomistNo ratings yet

- Taxpayers and Tax Spenders Lipford Yandle WP1129 0Document31 pagesTaxpayers and Tax Spenders Lipford Yandle WP1129 0thecynicaleconomistNo ratings yet

- Life After Debt - Debtless by 2012, The U.S and The World Without US Treasury Bonds (FOIA Document)Document43 pagesLife After Debt - Debtless by 2012, The U.S and The World Without US Treasury Bonds (FOIA Document)Ephraim DavisNo ratings yet

- FINAL Final - MAP ReportDocument37 pagesFINAL Final - MAP ReportthecynicaleconomistNo ratings yet

- Final Coburn Job Training Report - 02082011Document79 pagesFinal Coburn Job Training Report - 02082011thecynicaleconomistNo ratings yet

- The American Welfare State How We Spend Nearly $1 Trillion A Year Fighting Poverty - and Fail, Cato Policy Analysis No. 694Document24 pagesThe American Welfare State How We Spend Nearly $1 Trillion A Year Fighting Poverty - and Fail, Cato Policy Analysis No. 694Cato Institute100% (1)

- Sen. Coburn's 2013 Waste BookDocument177 pagesSen. Coburn's 2013 Waste BookHelen TanseyNo ratings yet

- Congress Waste Book 2012Document202 pagesCongress Waste Book 2012Brightstar15No ratings yet

- America's New Post-RecessionEmployment ArithmeticDocument16 pagesAmerica's New Post-RecessionEmployment ArithmeticthecynicaleconomistNo ratings yet

- JEC Testimony - 9.20.2011 - Statement of Chris Edwards, Director of Tax Policy Studies, Cato InstituteDocument9 pagesJEC Testimony - 9.20.2011 - Statement of Chris Edwards, Director of Tax Policy Studies, Cato InstitutethecynicaleconomistNo ratings yet

- Wastebook 2011Document98 pagesWastebook 2011thecynicaleconomistNo ratings yet

- Gresham's Law of Green EnergyDocument7 pagesGresham's Law of Green EnergythecynicaleconomistNo ratings yet

- 06 21 Long Term Budget OutlookDocument108 pages06 21 Long Term Budget OutlookthecynicaleconomistNo ratings yet

- 2010 Senate Minority ReportDocument321 pages2010 Senate Minority Reportthecynicaleconomist100% (1)

- Warming Power of CO2 and H2O: Correlations With Temperature ChangesDocument11 pagesWarming Power of CO2 and H2O: Correlations With Temperature ChangesthecynicaleconomistNo ratings yet

- 2010 WastDocument85 pages2010 WastJeffrey DunetzNo ratings yet

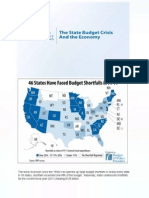

- The State Budget Crisis and The EconomyDocument5 pagesThe State Budget Crisis and The EconomythecynicaleconomistNo ratings yet

- Wealth Effects Stock Market Vs HousingDocument26 pagesWealth Effects Stock Market Vs HousingthecynicaleconomistNo ratings yet

- Wegelin & Co - Investment Commentary 272 - Too Big Not To FailDocument8 pagesWegelin & Co - Investment Commentary 272 - Too Big Not To FailthecynicaleconomistNo ratings yet

- 07-27 Debt Fiscal Crisis BriefDocument8 pages07-27 Debt Fiscal Crisis BriefthecynicaleconomistNo ratings yet

- Current Economic Conditions: Summary of Commentary OnDocument47 pagesCurrent Economic Conditions: Summary of Commentary OnPlan B EconomicsNo ratings yet

- Japan Government Bonds AdDocument1 pageJapan Government Bonds AdthecynicaleconomistNo ratings yet

- Great Myths of The Great DepressionDocument16 pagesGreat Myths of The Great DepressionEducators of Liberty100% (2)

- The Fiscal Burden of Illegal ImmigrationDocument7 pagesThe Fiscal Burden of Illegal ImmigrationthecynicaleconomistNo ratings yet

- Citizens Against Government Waste 2010 Pig Book SummaryDocument66 pagesCitizens Against Government Waste 2010 Pig Book SummaryThe West Virginia Examiner/WV WatchdogNo ratings yet

- New IMF Strategy Document Charts Launch of "Bancor" Global CurrencyDocument35 pagesNew IMF Strategy Document Charts Launch of "Bancor" Global Currencymurciano207No ratings yet

- CMA Global Sovereign Credit Risk Report Q2 2010Document19 pagesCMA Global Sovereign Credit Risk Report Q2 2010thecynicaleconomistNo ratings yet

- Federal Spending by The Numbers 2010Document22 pagesFederal Spending by The Numbers 2010thecynicaleconomistNo ratings yet

- New FTC Staff DiscussionDocument47 pagesNew FTC Staff DiscussionAlex HowardNo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (894)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Lit Crit TextDocument8 pagesLit Crit TextFhe CidroNo ratings yet

- One Page AdventuresDocument24 pagesOne Page AdventuresPotato Knishes100% (1)

- Barangay Peace and Order and Public Safety Plan Bpops Annex ADocument3 pagesBarangay Peace and Order and Public Safety Plan Bpops Annex AImee CorreaNo ratings yet

- Prevention of Surgical Site Infections: Pola Brenner, Patricio NercellesDocument10 pagesPrevention of Surgical Site Infections: Pola Brenner, Patricio NercellesAmeng GosimNo ratings yet

- Rendemen Dan Skrining Fitokimia Pada Ekstrak DaunDocument6 pagesRendemen Dan Skrining Fitokimia Pada Ekstrak DaunArdya YusidhaNo ratings yet

- Us Errata Document 11-14-13Document12 pagesUs Errata Document 11-14-13H VNo ratings yet

- DQ RMGDocument23 pagesDQ RMGDhaval ChaplaNo ratings yet

- Cost Estimation of SlaughterhouseDocument25 pagesCost Estimation of Slaughterhousemohamed faahiyeNo ratings yet

- ECOSIADocument8 pagesECOSIAaliosk8799No ratings yet

- Microeconomics 5th Edition Hubbard Solutions Manual 1Document23 pagesMicroeconomics 5th Edition Hubbard Solutions Manual 1christina100% (48)

- Ganga Pollution CasesDocument3 pagesGanga Pollution CasesRuchita KaundalNo ratings yet

- 1154ec108nanoelectronics PDFDocument3 pages1154ec108nanoelectronics PDFLordwin CecilNo ratings yet

- En50443 - SC9XC - 11656 - Enq2e (Mod 7 10 10)Document32 pagesEn50443 - SC9XC - 11656 - Enq2e (Mod 7 10 10)Levente CzumbilNo ratings yet

- Thalassemia WikiDocument12 pagesThalassemia Wikiholy_miracleNo ratings yet

- Ted TalkDocument4 pagesTed Talkapi-550727300No ratings yet

- Yoga Nidra MethodDocument13 pagesYoga Nidra MethodPrahlad Basnet100% (2)

- Full Text 01Document72 pagesFull Text 01aghosh704No ratings yet

- SIDCSDocument8 pagesSIDCSsakshi suranaNo ratings yet

- Horlicks: Cooking Tips For HorlicksDocument4 pagesHorlicks: Cooking Tips For HorlickschhandacNo ratings yet

- Statistics of Design Error in The Process IndustriesDocument13 pagesStatistics of Design Error in The Process IndustriesEmmanuel Osorno CaroNo ratings yet

- Penyakit Palpebra Dan AdneksaDocument39 pagesPenyakit Palpebra Dan AdneksaayucicuNo ratings yet

- Excel - All Workout Routines Exercises Reps Sets EtcDocument10 pagesExcel - All Workout Routines Exercises Reps Sets EtcJanus Blacklight100% (1)

- As en 540-2002 Clinical Investigation of Medical Devices For Human SubjectsDocument8 pagesAs en 540-2002 Clinical Investigation of Medical Devices For Human SubjectsSAI Global - APACNo ratings yet

- BSN-2D 1st Semester ScheduleDocument2 pagesBSN-2D 1st Semester ScheduleReyjan ApolonioNo ratings yet

- Excipients As StabilizersDocument7 pagesExcipients As StabilizersxdgvsdgNo ratings yet

- Tracking SARDO StudentsDocument2 pagesTracking SARDO StudentsLean ABNo ratings yet

- Personal Development: Quarter 1 - Module 5: Developmental Tasks and Challenges of AdolescenceDocument16 pagesPersonal Development: Quarter 1 - Module 5: Developmental Tasks and Challenges of AdolescenceMary Joy CejalboNo ratings yet

- Design AI Platform Using Fuzzy Logic Technique To Diagnose Kidney DiseasesDocument9 pagesDesign AI Platform Using Fuzzy Logic Technique To Diagnose Kidney DiseasesTELKOMNIKANo ratings yet

- Greenhouse Effect: Greenhouse Gases and Their Impact On Global WarmingDocument9 pagesGreenhouse Effect: Greenhouse Gases and Their Impact On Global WarmingrabiulNo ratings yet

- Home & Garden 2015Document32 pagesHome & Garden 2015The Standard NewspaperNo ratings yet