You might also like

- PT. Anugerah Cahaya Cemerlang Lestari Directur (Zahren Mohamed) Jl. Minangkabau Ruko 6E, Jakarta Selatan 12970Document1 pagePT. Anugerah Cahaya Cemerlang Lestari Directur (Zahren Mohamed) Jl. Minangkabau Ruko 6E, Jakarta Selatan 12970Zamri MahfudzNo ratings yet

- Ota Update Procedure For Zenfone 4 & 5 & 6Document4 pagesOta Update Procedure For Zenfone 4 & 5 & 6Chan Kuan FooNo ratings yet

- Deep ConsumptionDocument2 pagesDeep ConsumptionZamri MahfudzNo ratings yet

- Fco GCV Adb 55-53 Nie-RrpDocument3 pagesFco GCV Adb 55-53 Nie-RrpZamri MahfudzNo ratings yet

- Presidential Regulation No 36 of 2010-1Document101 pagesPresidential Regulation No 36 of 2010-1Andre SimangunsongNo ratings yet

- Peta Perkembangan Izin Penggunaan Kawasan Hutan Provinsi Kalimantan Tengah (S/D September 2012)Document1 pagePeta Perkembangan Izin Penggunaan Kawasan Hutan Provinsi Kalimantan Tengah (S/D September 2012)Zamri MahfudzNo ratings yet

- Quantum Computer Website - SimulasiDocument1 pageQuantum Computer Website - SimulasiZamri MahfudzNo ratings yet

- PT. Anugerah Cahaya Cemerlang Lestari Directur (Zahren Mohamed) Jl. Minangkabau Ruko 6E, Jakarta Selatan 12970Document1 pagePT. Anugerah Cahaya Cemerlang Lestari Directur (Zahren Mohamed) Jl. Minangkabau Ruko 6E, Jakarta Selatan 12970Zamri MahfudzNo ratings yet

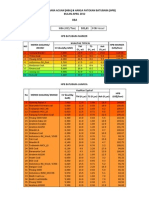

- Harga Batubara Acuan April 2012Document6 pagesHarga Batubara Acuan April 2012satuiku100% (1)

- Dzikir Doa Bada Sholat Fardhu FNLDocument10 pagesDzikir Doa Bada Sholat Fardhu FNLSuprianto MasterofArtNo ratings yet

- G-Resources (Martabe Project)Document11 pagesG-Resources (Martabe Project)Zamri MahfudzNo ratings yet

- HASIL EKSPLORASI MINERAL LOGAM KERJASAMA INDONESIA-JEPANG DAN KOREADocument14 pagesHASIL EKSPLORASI MINERAL LOGAM KERJASAMA INDONESIA-JEPANG DAN KOREAZamri MahfudzNo ratings yet

- Manual Del Modem Tl-wr842nd en InglesDocument130 pagesManual Del Modem Tl-wr842nd en InglesEduardito De Villa CrespoNo ratings yet

- PT Damasari Banten July 2013 (Compatibility Mode) - 1Document21 pagesPT Damasari Banten July 2013 (Compatibility Mode) - 1Zamri MahfudzNo ratings yet

- DP822H P.bzafllk MFL67441112Document24 pagesDP822H P.bzafllk MFL67441112Zamri MahfudzNo ratings yet

- HASIL EKSPLORASI MINERAL LOGAM KERJASAMA INDONESIA-JEPANG DAN KOREADocument14 pagesHASIL EKSPLORASI MINERAL LOGAM KERJASAMA INDONESIA-JEPANG DAN KOREAZamri MahfudzNo ratings yet

- Topo Graph IDocument1 pageTopo Graph IZamri MahfudzNo ratings yet

- Ageloc Galvanic Spa FaqDocument8 pagesAgeloc Galvanic Spa FaqZamri MahfudzNo ratings yet

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (890)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Building A Holistic Capital Management FrameworkDocument16 pagesBuilding A Holistic Capital Management FrameworkCognizantNo ratings yet

- Di OutlineDocument81 pagesDi OutlineRobert E. BrannNo ratings yet

- A Handbook On Private Equity FundingDocument109 pagesA Handbook On Private Equity FundingLakshmi811No ratings yet

- Debt Level and Firm Performance: A Study On Low-Cap Firms Listed On The Kuala Lumpur Stock ExchangeDocument17 pagesDebt Level and Firm Performance: A Study On Low-Cap Firms Listed On The Kuala Lumpur Stock ExchangeMaha Ben BrahimNo ratings yet

- Brahma Et Al. - 2020 - Board Gender Diversity and Firm Performance The UDocument16 pagesBrahma Et Al. - 2020 - Board Gender Diversity and Firm Performance The URMADVNo ratings yet

- Maruti Suzuki India LTDDocument8 pagesMaruti Suzuki India LTDRushikesh PawarNo ratings yet

- Bewakoof Brands - Financial Analysis DataDocument8 pagesBewakoof Brands - Financial Analysis DataDimple SundraniNo ratings yet

- Milestone Gears Private Limited Ratings ReaffirmedDocument4 pagesMilestone Gears Private Limited Ratings ReaffirmedPuneet367No ratings yet

- FOFA RatiosDocument11 pagesFOFA RatiosShilpa RajuNo ratings yet

- Fin 301 - Group Assignment - Group GDocument10 pagesFin 301 - Group Assignment - Group GAvishake SahaNo ratings yet

- Question and Answer - 53Document30 pagesQuestion and Answer - 53acc-expertNo ratings yet

- Chapter 8 - Financial AnalysisDocument36 pagesChapter 8 - Financial AnalysisSameh EldosoukiNo ratings yet

- Chapter 8Document19 pagesChapter 8Benny Khor100% (2)

- Financial Analysis of Ultra Tech CementDocument23 pagesFinancial Analysis of Ultra Tech Cementsanchit1170% (2)

- 16 x11 FinMan DDocument8 pages16 x11 FinMan DErwin Cajucom50% (2)

- Credit Management HandbookDocument48 pagesCredit Management HandbookNauman Rashid67% (6)

- Artha PediaDocument158 pagesArtha Pediagajen_yadavNo ratings yet

- Group 10 - Tata MotorsDocument30 pagesGroup 10 - Tata MotorsSayan MondalNo ratings yet

- Investment Appraisal QsDocument8 pagesInvestment Appraisal Qsnajah madihahNo ratings yet

- Finman Financial Ratio AnalysisDocument26 pagesFinman Financial Ratio AnalysisJoyce Anne SobremonteNo ratings yet

- Petronas Gas AnalysisDocument30 pagesPetronas Gas AnalysisViet Hung70% (10)

- Case Study Hero Cycles - Operating Breakevens - No Profit & No Loss SituationDocument8 pagesCase Study Hero Cycles - Operating Breakevens - No Profit & No Loss SituationRLDK409No ratings yet

- FRA ProjectDocument63 pagesFRA ProjectRisa SahaNo ratings yet

- Acc501 Quiz FileDocument19 pagesAcc501 Quiz Filedaredevil18050% (2)

- FM Project 1Document24 pagesFM Project 1Soumya MohapatraNo ratings yet

- Ratio Analysis: (School) (Course Title)Document14 pagesRatio Analysis: (School) (Course Title)aseni herathNo ratings yet

- Zameer Và C NG S, 2013. Determinants of Dividend Policy A Case of Banking Sector in Pakistan, Middle-East Journal of Scientific Research, ISSN 1990-9233 PDFDocument15 pagesZameer Và C NG S, 2013. Determinants of Dividend Policy A Case of Banking Sector in Pakistan, Middle-East Journal of Scientific Research, ISSN 1990-9233 PDFThi NguyenNo ratings yet

- Introduction To Foreign ExchangeDocument36 pagesIntroduction To Foreign Exchangedhruv_jagtap100% (1)

- Financial Analysis of DG Khan Cement Factory, Ratio AnalysisDocument57 pagesFinancial Analysis of DG Khan Cement Factory, Ratio AnalysisM Fahim Arshed50% (8)

- Accounting Final ProjectDocument21 pagesAccounting Final ProjectKeenNo ratings yet