You might also like

- Clearing Up Confusion Over Calculation of Free Cash FlowDocument6 pagesClearing Up Confusion Over Calculation of Free Cash FlowSohini Mo BanerjeeNo ratings yet

- Game Rules 2012Document19 pagesGame Rules 2012hiknikNo ratings yet

- Unit 2 Structure and BondingDocument61 pagesUnit 2 Structure and BondingAbdulrahman Rashid AlbusaidiNo ratings yet

- BCl3 / Boron TrichlorideDocument2 pagesBCl3 / Boron TrichlorideSAFC-GlobalNo ratings yet

- Capex Final - Ingles 2Document8 pagesCapex Final - Ingles 2Julio Brayan Berrocal Majerhua100% (1)

- lean spare parts management A Complete Guide - 2019 EditionFrom Everandlean spare parts management A Complete Guide - 2019 EditionNo ratings yet

- Calculation For Heat of CombustionDocument2 pagesCalculation For Heat of CombustionFauziah MuniraNo ratings yet

- Diborane: Click To Edit Master Subtitle StyleDocument36 pagesDiborane: Click To Edit Master Subtitle StyleSaumya GoelNo ratings yet

- The Problem With Waiting TimeDocument8 pagesThe Problem With Waiting Timemano7428No ratings yet

- Internet Use Guide for StudentsDocument5 pagesInternet Use Guide for StudentsMichelle SahoriNo ratings yet

- FMEADocument14 pagesFMEAAndreea FeltAccessoriesNo ratings yet

- 1 - Life Cycle Inventory of Portland Cement ManufactureDocument68 pages1 - Life Cycle Inventory of Portland Cement ManufactureAnonymous LEVNDh4No ratings yet

- Integrated Risk and Earned Value Management: 2007 NDIA Systems Engineering Conference San Diego, CADocument13 pagesIntegrated Risk and Earned Value Management: 2007 NDIA Systems Engineering Conference San Diego, CAcristinaNo ratings yet

- 2016 Valero Annual Report WebDocument34 pages2016 Valero Annual Report WebPuneet MittalNo ratings yet

- Flex Sim BrochureDocument4 pagesFlex Sim BrochureArielovimagNo ratings yet

- Estimation of Offshore Brazilian Natural Gas Break-Even PricesDocument10 pagesEstimation of Offshore Brazilian Natural Gas Break-Even PricesMarcelo Varejão CasarinNo ratings yet

- 1.4 Stocked Maintenance, Repair and Operating Materials (Mro) Inventory Value As A Percent of Replacement Asset Value (Rav)Document4 pages1.4 Stocked Maintenance, Repair and Operating Materials (Mro) Inventory Value As A Percent of Replacement Asset Value (Rav)cks100% (1)

- Study On Modeling and Simulation of Logistics Sorting System Based On FlexsimDocument3 pagesStudy On Modeling and Simulation of Logistics Sorting System Based On FlexsimSoli UdinNo ratings yet

- AIMMS Tutorial BeginnersDocument46 pagesAIMMS Tutorial Beginnerstryinghard18No ratings yet

- Optimize Process Safety with FMEADocument19 pagesOptimize Process Safety with FMEADamodaran RajanayagamNo ratings yet

- Calculating Wrench Time: Statistical Activity SurveysDocument7 pagesCalculating Wrench Time: Statistical Activity Surveysgopalakrishnannrm1202100% (1)

- Life in The Future (Will)Document3 pagesLife in The Future (Will)sgumoNo ratings yet

- Natural Gas Transmission Systems - CPADocument8 pagesNatural Gas Transmission Systems - CPAmike BarrazaNo ratings yet

- SMRP Metric 1.4 Stocked Value Per RAV 050321 FCDocument2 pagesSMRP Metric 1.4 Stocked Value Per RAV 050321 FClobitodelperuNo ratings yet

- Developing The Project PlanDocument8 pagesDeveloping The Project PlanStephanie BucogNo ratings yet

- 7 Key Stages CAPEX ProcessDocument9 pages7 Key Stages CAPEX ProcessІрина ТурецькаNo ratings yet

- Cost Estimation and RiskDocument1 pageCost Estimation and RiskBramJanssen76No ratings yet

- Sust Capex-Aluminium Julaug2016Document4 pagesSust Capex-Aluminium Julaug2016HiddenDNo ratings yet

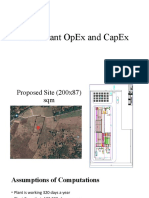

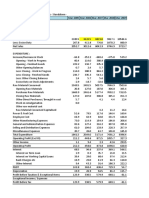

- AAC Plant OpEx and CapEx Rev2Document8 pagesAAC Plant OpEx and CapEx Rev2Kevin CariñoNo ratings yet

- Practical Reliability Tools For Refineries and Chemical PlantsDocument9 pagesPractical Reliability Tools For Refineries and Chemical PlantsDana Guerrero100% (1)

- Capitalize Six Drivers Successful Capex Saving StrategiesDocument12 pagesCapitalize Six Drivers Successful Capex Saving StrategiesMine BentachNo ratings yet

- SAP PM External Services ManualDocument25 pagesSAP PM External Services ManualPramod ShettyNo ratings yet

- Managing small and medium capital projects on time and budgetDocument8 pagesManaging small and medium capital projects on time and budgetKevin DrummNo ratings yet

- Developing an MPM Framework Using ANP for Maintenance Performance Indicator SelectionDocument14 pagesDeveloping an MPM Framework Using ANP for Maintenance Performance Indicator SelectionAlejandro100% (1)

- Cost plan template for elemental renewal and maintenance worksDocument5 pagesCost plan template for elemental renewal and maintenance worksMuhammadWaqarButt100% (1)

- Meridium APM Now: Cloud-Based Asset Performance ManagementDocument2 pagesMeridium APM Now: Cloud-Based Asset Performance ManagementSANDRA TORRESNo ratings yet

- Benchmarking Oil and Gas IBPDocument7 pagesBenchmarking Oil and Gas IBPDhanes PratitaNo ratings yet

- IFRS Vs German GAAP Similarities and Differences - Final2 PDFDocument87 pagesIFRS Vs German GAAP Similarities and Differences - Final2 PDFBrian TranNo ratings yet

- A Virtual Reality in FlexsimDocument10 pagesA Virtual Reality in FlexsimTimothae ZacharyyNo ratings yet

- LCE Risk-Based Asset Management ReportDocument11 pagesLCE Risk-Based Asset Management ReportPola7317No ratings yet

- Aromatics Study - CPADocument4 pagesAromatics Study - CPAmike BarrazaNo ratings yet

- Movie Materials PDFDocument1 pageMovie Materials PDFMatias SilvaNo ratings yet

- Developing Leaders in Your CompanyDocument2 pagesDeveloping Leaders in Your CompanySyElfredGNo ratings yet

- CMMSDocument9 pagesCMMSHanna Rizanti KartinaNo ratings yet

- Porter's Analysis of Oil & Gas Sector: Competitive Rivalry (LOW) Competitive Rivalry (LOW)Document2 pagesPorter's Analysis of Oil & Gas Sector: Competitive Rivalry (LOW) Competitive Rivalry (LOW)Imran KhanNo ratings yet

- Drive Maintenance Performance with Data MetricsDocument63 pagesDrive Maintenance Performance with Data MetricsMónica Rada Urbina100% (1)

- Capital-Expenditures - Guide To Managing CapexDocument84 pagesCapital-Expenditures - Guide To Managing CapexEder Andres Rodriguez Cotua100% (1)

- Life Cycle Cost AnalysisDocument7 pagesLife Cycle Cost AnalysisDenilson MarinhoNo ratings yet

- Quick Start Guide to Analyzing Investment Project Risk with @RISKDocument12 pagesQuick Start Guide to Analyzing Investment Project Risk with @RISKaalba005No ratings yet

- Process CostingDocument20 pagesProcess CostingJanak DandNo ratings yet

- MBR OPEX - The Theory of Running CostsDocument6 pagesMBR OPEX - The Theory of Running CostsJeremy DudleyNo ratings yet

- Aurora Cost Allocation MethodDocument57 pagesAurora Cost Allocation MethodFelicidade Da SilvaNo ratings yet

- Cmms CSDP TrainingDocument44 pagesCmms CSDP TrainingRudyard ZednanrefNo ratings yet

- Project Cost-Time-Risk Diagram for Planning and Risk ManagementDocument8 pagesProject Cost-Time-Risk Diagram for Planning and Risk ManagementGuillermo BandaNo ratings yet

- CVP Analysis Break-Even Point ProfitDocument6 pagesCVP Analysis Break-Even Point ProfitMark Aldrich Ubando0% (1)

- CVP AnalysisDocument12 pagesCVP AnalysisKamini Satish SinghNo ratings yet

- Rajasthan Public Service CommissionDocument5 pagesRajasthan Public Service CommissionPooja MeenaNo ratings yet

- EbookProvider - Co.cc You Can WinDocument12 pagesEbookProvider - Co.cc You Can WinJyoti BishnoiNo ratings yet

- Axis PDFDocument1 pageAxis PDFGaurav JainNo ratings yet

- Amit Bhuwania Resume JPDocument1 pageAmit Bhuwania Resume JPGaurav JainNo ratings yet

- Kei PDFDocument3 pagesKei PDFGaurav JainNo ratings yet

- Amit Bhuwania Resume JPDocument1 pageAmit Bhuwania Resume JPGaurav JainNo ratings yet

- ICRA Annual Report 2011-12Document138 pagesICRA Annual Report 2011-12Gaurav JainNo ratings yet

- Kei PDFDocument3 pagesKei PDFGaurav JainNo ratings yet

- Abhay SinghDocument2 pagesAbhay SinghGaurav JainNo ratings yet

- KeiDocument38 pagesKeiGaurav JainNo ratings yet

- Salary Receipt: Received From Shri Salary Received As Driver of His Car During The Period, January 2019 To February 2019Document1 pageSalary Receipt: Received From Shri Salary Received As Driver of His Car During The Period, January 2019 To February 2019Gaurav JainNo ratings yet

- Nicholas A. J. Hastings (Auth.) - Physical Asset Management (2010, Springer London)Document77 pagesNicholas A. J. Hastings (Auth.) - Physical Asset Management (2010, Springer London)Darel Muhammad KamilNo ratings yet

- Abhay SinghDocument2 pagesAbhay SinghGaurav JainNo ratings yet

- DupontDocument88 pagesDupontGaurav JainNo ratings yet

- Fee Strcuture 2019 20Document1 pageFee Strcuture 2019 20Gaurav JainNo ratings yet

- Commercial PaperDocument4 pagesCommercial PaperGaurav JainNo ratings yet

- RBI Guidelines On Stress TestingDocument29 pagesRBI Guidelines On Stress TestingbankamitNo ratings yet

- THS19130724 1 6Document1 pageTHS19130724 1 6Gaurav JainNo ratings yet

- Cement GlobalDocument40 pagesCement Globalkvk0812No ratings yet

- SSRN Id1087583Document29 pagesSSRN Id1087583Gaurav JainNo ratings yet

- Priyanka Chouhan Resume SummaryDocument3 pagesPriyanka Chouhan Resume SummaryGaurav JainNo ratings yet

- Rating Report - Shri Laxmi Narayan Industries (NSIC)Document6 pagesRating Report - Shri Laxmi Narayan Industries (NSIC)Gaurav JainNo ratings yet

- GMAT Club Math Book v3 - Jan-2-2013Document126 pagesGMAT Club Math Book v3 - Jan-2-2013prabhakar0808No ratings yet

- Study Tips for Your Best GMAT ExamDocument38 pagesStudy Tips for Your Best GMAT ExamGaurav JainNo ratings yet

- Experienced Credit Analyst Seeks New OpportunitiesDocument3 pagesExperienced Credit Analyst Seeks New OpportunitiesGaurav JainNo ratings yet

- FCFDocument6 pagesFCFffccllNo ratings yet

- Decision-Making For Investors: Theory, Practice, and PitfallsDocument20 pagesDecision-Making For Investors: Theory, Practice, and PitfallsGaurav JainNo ratings yet

- Description Mar-07 Mar-08 Mar-09 Mar-10: Yes Yes Yes YesDocument12 pagesDescription Mar-07 Mar-08 Mar-09 Mar-10: Yes Yes Yes YesGaurav JainNo ratings yet

- ASCE 7-98 Code Wind Loading AnalysisDocument34 pagesASCE 7-98 Code Wind Loading AnalysisPipim Pogi100% (1)

- Lead Allocation Case: InstructionsDocument17 pagesLead Allocation Case: Instructionsqwerty9876543210% (3)

- TVL Empowerment Technologies q2 SpreadsheetDocument3 pagesTVL Empowerment Technologies q2 SpreadsheetChristian DelapenaNo ratings yet

- SQ-402 SCADA Add-In User GuideDocument23 pagesSQ-402 SCADA Add-In User Guidemojsic6313100% (1)

- Micro Drainage International ManualDocument349 pagesMicro Drainage International Manualmazzam75No ratings yet

- 04.CA (CL) - IT - (Module-2) - (4) Information Technology-SoftwareDocument29 pages04.CA (CL) - IT - (Module-2) - (4) Information Technology-Softwareilias khanNo ratings yet

- Specialisti: Employee RosterDocument4 pagesSpecialisti: Employee RosterDeborah GalangNo ratings yet

- EmTech Module - Q1 by Grascia - 2Document17 pagesEmTech Module - Q1 by Grascia - 2gRascia OnaNo ratings yet

- Oracle Fusion Middleware: User's Guide For Oracle Data Visualization 12c (12.2.1.1.0)Document84 pagesOracle Fusion Middleware: User's Guide For Oracle Data Visualization 12c (12.2.1.1.0)Abdelrhman SalahNo ratings yet

- Csi Bridge PDFDocument58 pagesCsi Bridge PDFrangga noparaNo ratings yet

- Y10 ICT Revision Checklist Mock Term3Document6 pagesY10 ICT Revision Checklist Mock Term3Mohamed RazeenNo ratings yet

- LBS DCA (S) OpenOffice - Org Calc NotesDocument50 pagesLBS DCA (S) OpenOffice - Org Calc NotesNIJEESH RAJ N100% (2)

- MS Office NotesDocument4 pagesMS Office NotesHIMANSHU KUMAR CHOUDHARYNo ratings yet

- Excel Logic Exercises On PaperDocument16 pagesExcel Logic Exercises On PapervitezixNo ratings yet

- Risa - FoundationDocument371 pagesRisa - Foundationtekla gom-lua groupNo ratings yet

- Proceedings of the Design Modelling Symposium Berlin 2009Document11 pagesProceedings of the Design Modelling Symposium Berlin 2009sharathr22No ratings yet

- Arena Project (Banking Transaction)Document13 pagesArena Project (Banking Transaction)Mostafa NasherNo ratings yet

- Introduction To Management Science Taylor 10th Edition Solutions ManualDocument9 pagesIntroduction To Management Science Taylor 10th Edition Solutions Manualpinderrhematicw05tNo ratings yet

- 8 WindPRO3.5-OptimizationDocument36 pages8 WindPRO3.5-OptimizationHéctor LodosoNo ratings yet

- Allama Iqbal Open University Computer Course DocumentsDocument7 pagesAllama Iqbal Open University Computer Course DocumentsreniNo ratings yet

- Cot 3 - Tle Ict Week 6Document6 pagesCot 3 - Tle Ict Week 6mzo9No ratings yet

- Module 2 - Excel Intro To Multiple WorksheetsDocument37 pagesModule 2 - Excel Intro To Multiple WorksheetsinggoNo ratings yet

- TCO Moodlerooms Read Me First User Guide - Total Cost of Ownership MoodleDocument13 pagesTCO Moodlerooms Read Me First User Guide - Total Cost of Ownership MoodleVanessa Ferrer VisbalNo ratings yet

- Analytical Chemistry Manual PDFDocument58 pagesAnalytical Chemistry Manual PDFVaishali RaneNo ratings yet

- LabVIEW TutorialDocument43 pagesLabVIEW Tutorialntdien923No ratings yet

- Computer Teaching BookDocument84 pagesComputer Teaching Bookaditya kumarNo ratings yet

- UML Activity DiagramDocument13 pagesUML Activity DiagramMuqaddas RasheedNo ratings yet

- It SbaDocument10 pagesIt Sbaanon_5224885850% (2)

- ICT Tools: Online Exam (Quiz) Through Google Forms: Dr.B.Surendranath ReddyDocument16 pagesICT Tools: Online Exam (Quiz) Through Google Forms: Dr.B.Surendranath ReddyRahul ShindeNo ratings yet

- Chapter 2 Key Elements in Engineering AnalysisDocument35 pagesChapter 2 Key Elements in Engineering AnalysisAkmal HafizhNo ratings yet