You might also like

- Creating An Automated Stock Trading System in ExcelDocument19 pagesCreating An Automated Stock Trading System in Excelgeorgez111100% (2)

- Jana Partners LetterDocument12 pagesJana Partners LetterSimone Sebastian100% (2)

- Leadership Risk: A Guide for Private Equity and Strategic InvestorsFrom EverandLeadership Risk: A Guide for Private Equity and Strategic InvestorsNo ratings yet

- Greenlight Q1 15Document6 pagesGreenlight Q1 15marketfolly.com100% (2)

- ThirdPoint Q1 16Document9 pagesThirdPoint Q1 16marketfolly.comNo ratings yet

- Energy Trading And Risk Management A Complete Guide - 2020 EditionFrom EverandEnergy Trading And Risk Management A Complete Guide - 2020 EditionNo ratings yet

- Opko Health - Lakewood Short ThesisDocument48 pagesOpko Health - Lakewood Short ThesisCanadianValueNo ratings yet

- Progress Ventures Newsletter 3Q2018Document18 pagesProgress Ventures Newsletter 3Q2018Anonymous Feglbx5No ratings yet

- ISI Evercore OFS InitiationDocument425 pagesISI Evercore OFS Initiationstw10128No ratings yet

- Ackman Letter May 2016Document14 pagesAckman Letter May 2016ZerohedgeNo ratings yet

- Newell Brands Inc Oct 10Document14 pagesNewell Brands Inc Oct 10Anonymous Ecd8rC100% (2)

- Pershing Square 3Q-2016 Investor LetterDocument16 pagesPershing Square 3Q-2016 Investor LettersuperinvestorbulletiNo ratings yet

- LJPC Vol 2 Q and A Final 2.0Document13 pagesLJPC Vol 2 Q and A Final 2.0Art Doyle100% (3)

- WVE (Wave Life Sciences) : All Pump, No Action... Hitting RESET (PT: $16), Part 1 in A Multipart Series On WVE (SHORT)Document17 pagesWVE (Wave Life Sciences) : All Pump, No Action... Hitting RESET (PT: $16), Part 1 in A Multipart Series On WVE (SHORT)Art DoyleNo ratings yet

- Pfenex Inc (PFNX) ThesisDocument5 pagesPfenex Inc (PFNX) Thesisjulia skripka-serryNo ratings yet

- Pershing Square Second-Quarter Investor LetterDocument23 pagesPershing Square Second-Quarter Investor LetterNew York PostNo ratings yet

- GLD.031 Major Capital Projects (Minerals)Document35 pagesGLD.031 Major Capital Projects (Minerals)rebolledojf100% (3)

- Equity Investments PPT PresentationDocument80 pagesEquity Investments PPT PresentationRupal Rohan Dalal100% (1)

- XON Part 1Document28 pagesXON Part 1Anonymous Ht0MIJNo ratings yet

- Conviction Short Report On HK: 0633 China All Access by Triam ResearchDocument74 pagesConviction Short Report On HK: 0633 China All Access by Triam ResearchTriam ResearchNo ratings yet

- Eric Khrom of Khrom Capital 2012 Q4 LetterDocument5 pagesEric Khrom of Khrom Capital 2012 Q4 LetterallaboutvalueNo ratings yet

- Greenlight Capital Open Letter To AppleDocument5 pagesGreenlight Capital Open Letter To AppleZim VicomNo ratings yet

- James Montier WhatGoesUpDocument8 pagesJames Montier WhatGoesUpdtpalfiniNo ratings yet

- Third Point Q3 Investor LetterDocument8 pagesThird Point Q3 Investor Lettersuperinvestorbulleti100% (1)

- Exercises in Statement of Financial PositionDocument5 pagesExercises in Statement of Financial PositionQueen ValleNo ratings yet

- The Executive Guide to Boosting Cash Flow and Shareholder Value: The Profit Pool ApproachFrom EverandThe Executive Guide to Boosting Cash Flow and Shareholder Value: The Profit Pool ApproachNo ratings yet

- Corsair Q2 14Document3 pagesCorsair Q2 14marketfolly.comNo ratings yet

- Survival of the Fittest for Investors: Using Darwin’s Laws of Evolution to Build a Winning PortfolioFrom EverandSurvival of the Fittest for Investors: Using Darwin’s Laws of Evolution to Build a Winning PortfolioNo ratings yet

- Engineering Economy QuestionsDocument134 pagesEngineering Economy QuestionsJE Genobili100% (4)

- CLO Liquidity Provision and the Volcker Rule: Implications on the Corporate Bond MarketFrom EverandCLO Liquidity Provision and the Volcker Rule: Implications on the Corporate Bond MarketNo ratings yet

- Third Point Q109 LetterDocument4 pagesThird Point Q109 LetterZerohedgeNo ratings yet

- Performance of Private Equity-Backed IPOs. Evidence from the UK after the financial crisisFrom EverandPerformance of Private Equity-Backed IPOs. Evidence from the UK after the financial crisisNo ratings yet

- Third Point Q1 LetterDocument10 pagesThird Point Q1 LetterZerohedge100% (1)

- Rev. Fr. Emmanuel Lemelson Calls On Congress, Office of Inspector General To Investigate SEC FailuresDocument20 pagesRev. Fr. Emmanuel Lemelson Calls On Congress, Office of Inspector General To Investigate SEC FailuresamvonaNo ratings yet

- Why We'Re Long J.C. Penney-T2 PartnersDocument18 pagesWhy We'Re Long J.C. Penney-T2 PartnersVALUEWALK LLCNo ratings yet

- Pershing Square Q2 10 Investor LetterDocument8 pagesPershing Square Q2 10 Investor Lettereric695No ratings yet

- Tianhe PDFDocument67 pagesTianhe PDFValueWalkNo ratings yet

- Q1 2020 ThirdPoint-InvestorLetterDocument11 pagesQ1 2020 ThirdPoint-InvestorLetterlopaz777No ratings yet

- Meson Capital Partners - Odyssey Marine ExplorationDocument66 pagesMeson Capital Partners - Odyssey Marine ExplorationCanadianValueNo ratings yet

- CONN Job? Substantial Downside LikelyDocument19 pagesCONN Job? Substantial Downside LikelyCopperfield_Research100% (1)

- Chegg - A Textbook Story of FictionDocument43 pagesChegg - A Textbook Story of FictionCopperfield_Research100% (5)

- Loeb HLFDocument9 pagesLoeb HLFZerohedge100% (1)

- Third Point Q2 2010 Investor LetterDocument9 pagesThird Point Q2 2010 Investor Lettereric695No ratings yet

- STAADocument17 pagesSTAABlack Stork Research60% (5)

- Bill Ackman Ira Sohn Freddie Mac and Fannie Mae PresentationDocument111 pagesBill Ackman Ira Sohn Freddie Mac and Fannie Mae PresentationCanadianValueNo ratings yet

- Kyle Bass Presentation Hayman Global Outlook Pitfalls and Opportunities For 2014Document20 pagesKyle Bass Presentation Hayman Global Outlook Pitfalls and Opportunities For 2014ValueWalk100% (1)

- Greenlight GMDocument15 pagesGreenlight GMZerohedge100% (1)

- Aig Best of Bernstein SlidesDocument50 pagesAig Best of Bernstein SlidesYA2301100% (1)

- How To Save The Bond Insurers Presentation by Bill Ackman of Pershing Square Capital Management November 2007Document145 pagesHow To Save The Bond Insurers Presentation by Bill Ackman of Pershing Square Capital Management November 2007tomhigbieNo ratings yet

- Lemelson Capital Featured in HFMWeekDocument32 pagesLemelson Capital Featured in HFMWeekamvona100% (1)

- The Purpose of This CourseDocument6 pagesThe Purpose of This CourseSasha GrayNo ratings yet

- Q3 2021 - Investor LetterDocument2 pagesQ3 2021 - Investor LetterMessina04No ratings yet

- Advanced Battery Technologies, Inc.: Here HereDocument35 pagesAdvanced Battery Technologies, Inc.: Here HerePrescienceIGNo ratings yet

- Third Point Q3 2011Document5 pagesThird Point Q3 2011thereader2100% (1)

- Pershing Square 1Q17 Shareholder Letter May 11 2017 PSHDocument11 pagesPershing Square 1Q17 Shareholder Letter May 11 2017 PSHmarketfolly.comNo ratings yet

- Investing in Credit Hedge Funds: An In-Depth Guide to Building Your Portfolio and Profiting from the Credit MarketFrom EverandInvesting in Credit Hedge Funds: An In-Depth Guide to Building Your Portfolio and Profiting from the Credit MarketNo ratings yet

- Process and Asset Valuation A Complete Guide - 2019 EditionFrom EverandProcess and Asset Valuation A Complete Guide - 2019 EditionNo ratings yet

- Investing in Fiji’s Real Estate: Current Issues and OpportunitiesFrom EverandInvesting in Fiji’s Real Estate: Current Issues and OpportunitiesNo ratings yet

- Third Point Q1 2014 Investor LetterDocument13 pagesThird Point Q1 2014 Investor LetterCanadianValueNo ratings yet

- Berenberg European AerospaceDefence Sector Report Jun 17 2014 330pgs (Initiations)Document330 pagesBerenberg European AerospaceDefence Sector Report Jun 17 2014 330pgs (Initiations)angadsawhneyNo ratings yet

- Jeremy Grantham-US Stocks Are Expensive-27.06.12Document6 pagesJeremy Grantham-US Stocks Are Expensive-27.06.12Shakir ChoudharyNo ratings yet

- Corsair Capital Q4 2011Document3 pagesCorsair Capital Q4 2011angadsawhneyNo ratings yet

- Financial Analysis of Pakistan State Oil For The Period July 2017-June 2020Document25 pagesFinancial Analysis of Pakistan State Oil For The Period July 2017-June 2020Adil IqbalNo ratings yet

- Fdi at Mideast InvestmentsDocument88 pagesFdi at Mideast InvestmentsmadhuNo ratings yet

- Rbi Committee On Housing Finance SecuritisationDocument91 pagesRbi Committee On Housing Finance SecuritisationmeenaldutiaNo ratings yet

- Risk Management Topics in Indian BankingDocument2 pagesRisk Management Topics in Indian Bankingmonabiswas100% (1)

- Alekseev Innokenty 2002Document66 pagesAlekseev Innokenty 2002Harpott GhantaNo ratings yet

- Investor perception on commodity futuresDocument15 pagesInvestor perception on commodity futuresharshildodiya4uNo ratings yet

- II-ResearchTemplatev1 20Document301 pagesII-ResearchTemplatev1 20'Izzad AfifNo ratings yet

- Oakland Raiders Las Vegas NFL Stadium Spreadsheet by Zennie AbrahamDocument11 pagesOakland Raiders Las Vegas NFL Stadium Spreadsheet by Zennie AbrahamZennie AbrahamNo ratings yet

- Balance Sheet of Tata Motors (In Rs. CR.) : Equity S Are Capita Reserves and Surp UsDocument7 pagesBalance Sheet of Tata Motors (In Rs. CR.) : Equity S Are Capita Reserves and Surp UsGaurav VarshneyNo ratings yet

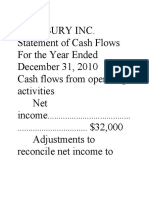

- Lansbury Inc cash flow analysisDocument10 pagesLansbury Inc cash flow analysis/// MASTER DOGENo ratings yet

- Source: Annual Accounts of BanksDocument6 pagesSource: Annual Accounts of BanksARVIND YADAVNo ratings yet

- Market Volume StopDocument14 pagesMarket Volume Stopvanthai06996No ratings yet

- Ind Assignment - Islamic Financial PlanningDocument15 pagesInd Assignment - Islamic Financial PlanningAtiqah AzmanNo ratings yet

- Document 5Document23 pagesDocument 5Chi ChengNo ratings yet

- Script - How To Survive RecessionDocument5 pagesScript - How To Survive RecessionMayumi AmponNo ratings yet

- Course Code ME-325: Engineering EconomicsDocument36 pagesCourse Code ME-325: Engineering EconomicsGet-Set-GoNo ratings yet

- GradedDocument6 pagesGradedYagnik prajapatiNo ratings yet

- Pathway To Financial Success: Autonomy Through Financial Education in IndiaDocument15 pagesPathway To Financial Success: Autonomy Through Financial Education in IndiaKirtyNo ratings yet

- Prject Report Financial Statement of NestleDocument14 pagesPrject Report Financial Statement of NestleSumia Hoque NovaNo ratings yet

- Techniques of Incorporating RiskDocument3 pagesTechniques of Incorporating RiskMac100% (2)

- Tutorial-Work-1-6-Questions 2014 PDFDocument25 pagesTutorial-Work-1-6-Questions 2014 PDFLi NguyenNo ratings yet

- b1 Solving Set 3 May 2018 - OnlineDocument4 pagesb1 Solving Set 3 May 2018 - OnlineGadafi FuadNo ratings yet

- Customer Satisfaction Towards Investing Chits in KsfeDocument41 pagesCustomer Satisfaction Towards Investing Chits in Ksfehariprasad kuloorNo ratings yet

- Accounting Chap 10 - Sheet1Document2 pagesAccounting Chap 10 - Sheet1Nguyễn Ngọc Mai100% (1)

- Chapter 9 Net Present Value and Other Investment Criteria: Use The Following Information To Answer Questions 1 Through 5Document12 pagesChapter 9 Net Present Value and Other Investment Criteria: Use The Following Information To Answer Questions 1 Through 5Tuấn HoàngNo ratings yet