You might also like

- As-22 Accounting For Taxes On Income - Brief NoteDocument5 pagesAs-22 Accounting For Taxes On Income - Brief NoteKaran KhatriNo ratings yet

- Financial Accounting - Want to Become Financial Accountant in 30 Days?From EverandFinancial Accounting - Want to Become Financial Accountant in 30 Days?Rating: 5 out of 5 stars5/5 (1)

- Accounting CheckDocument18 pagesAccounting Checkali razaNo ratings yet

- Chapter 14Document40 pagesChapter 14Ivo_NichtNo ratings yet

- Integrated Communication PlanDocument37 pagesIntegrated Communication PlanAnuruddha RajasuriyaNo ratings yet

- Corporate Accounting AssignmentDocument5 pagesCorporate Accounting AssignmentMd.Mahmudul HasanNo ratings yet

- Income Tax Accounting: Interacctgii BSA22A1 Online ModuleDocument17 pagesIncome Tax Accounting: Interacctgii BSA22A1 Online Module11 LamenNo ratings yet

- Deferred Income Tax PDFDocument2 pagesDeferred Income Tax PDFYeison Fabian Pirajan PachecoNo ratings yet

- Deferred Tax-Accounting Standard-22-Accounting For Taxes On IncomeDocument6 pagesDeferred Tax-Accounting Standard-22-Accounting For Taxes On IncomerlpolyfabsmaheshNo ratings yet

- Financial Reporting - Advanced - Tax Rate ReconciliationsDocument6 pagesFinancial Reporting - Advanced - Tax Rate ReconciliationsTami ChitandaNo ratings yet

- IAS 12 Income TaxesDocument4 pagesIAS 12 Income Taxeshae1234No ratings yet

- Module 2 Tax Accounting and BenefitsDocument12 pagesModule 2 Tax Accounting and BenefitsMon RamNo ratings yet

- Accounting Standard 22Document23 pagesAccounting Standard 22Rida TaarnnumNo ratings yet

- 02-IAS 12 Income TaxesDocument42 pages02-IAS 12 Income TaxesHaseeb Ullah KhanNo ratings yet

- Differences Between Taxable Income and Business IncomeDocument17 pagesDifferences Between Taxable Income and Business IncomeMegawati MediyaniNo ratings yet

- Tax ProjectDocument9 pagesTax ProjectMaaz SiddiquiNo ratings yet

- Income Tax 3Document12 pagesIncome Tax 3Mohammad AnikNo ratings yet

- Taxation BookDocument29 pagesTaxation BookbiggykhairNo ratings yet

- (ACYFAR 5) ReflectionDocument28 pages(ACYFAR 5) ReflectionAl ChuaNo ratings yet

- Deferred Tax Silvia IFRSBoxDocument10 pagesDeferred Tax Silvia IFRSBoxteddy matendawafaNo ratings yet

- How To Read A Financial ReportDocument192 pagesHow To Read A Financial Reportsonglo96100% (1)

- Taxguru - In-All About DEFERRED TAX and Its Entry in BooksDocument8 pagesTaxguru - In-All About DEFERRED TAX and Its Entry in Bookskumar45caNo ratings yet

- EbitdaDocument4 pagesEbitdaVenugopal Balakrishnan NairNo ratings yet

- AC13.4.1 Module 4 Income TaxesDocument23 pagesAC13.4.1 Module 4 Income TaxesRenelle HabacNo ratings yet

- Accounting Standard - 22Document25 pagesAccounting Standard - 22themeditator100% (1)

- IFRS-Deferred Tax Balance Sheet ApproachDocument8 pagesIFRS-Deferred Tax Balance Sheet ApproachJitendra JawalekarNo ratings yet

- IFRS News: Beginners' Guide: Nine Steps To Income Tax AccountingDocument4 pagesIFRS News: Beginners' Guide: Nine Steps To Income Tax AccountingVincent Chow Soon KitNo ratings yet

- Accounting For Deferred TaxesDocument47 pagesAccounting For Deferred TaxesSheda AshrafNo ratings yet

- Deferred TaxDocument5 pagesDeferred TaxRAKSHIT CHAUHANNo ratings yet

- Lesson 9 Tax Planning and StrategyDocument31 pagesLesson 9 Tax Planning and StrategyakpanyapNo ratings yet

- FARAP-4412 (Income Taxes)Document6 pagesFARAP-4412 (Income Taxes)Dizon Ropalito P.No ratings yet

- Deferred Tax (Basics)Document14 pagesDeferred Tax (Basics)TsekeNo ratings yet

- Accounting For Income Tax: Technical KnowledgeDocument45 pagesAccounting For Income Tax: Technical KnowledgeCharlene de LaraNo ratings yet

- Income Taxes: Basic ConceptsDocument7 pagesIncome Taxes: Basic ConceptsTrisha Mae Mendoza MacalinoNo ratings yet

- Accounting For VAT in Th... Accounting Center, Inc.Document4 pagesAccounting For VAT in Th... Accounting Center, Inc.Martin EspinosaNo ratings yet

- IAS 12 TaxesDocument16 pagesIAS 12 TaxesSARASVATHYDEVI SUBRAMANIAMNo ratings yet

- Historical Perspective: 23 Subsequently BecameDocument10 pagesHistorical Perspective: 23 Subsequently BecameSella DestikaNo ratings yet

- Equity, Financial Position and Cash FlowsDocument9 pagesEquity, Financial Position and Cash FlowsAbigail Elsa Samita Sitakar 1902113687No ratings yet

- Assignment - Accounting For IncomeDocument15 pagesAssignment - Accounting For IncomeGarang AtomditNo ratings yet

- Accounting For Income Tax: Technical KnowledgeDocument42 pagesAccounting For Income Tax: Technical KnowledgeAngela Miles DizonNo ratings yet

- Standards of AccountsDocument14 pagesStandards of Accountsaanu1234No ratings yet

- Corporate Tax PlanningDocument9 pagesCorporate Tax PlanningMd ChotaNo ratings yet

- Chapter 3 Deferred TaxDocument47 pagesChapter 3 Deferred TaxHammad Ahmad100% (1)

- Deferred Tax AnalysisDocument12 pagesDeferred Tax AnalysisBHAT SHARMA AND ASSOCIATESNo ratings yet

- FAR 4116 CleanDocument7 pagesFAR 4116 Cleanruel c armillaNo ratings yet

- Income TaxDocument13 pagesIncome TaxMohammad AnikNo ratings yet

- Accounting For Taxes On IncomeDocument25 pagesAccounting For Taxes On IncomeSUMANSHU_PATELNo ratings yet

- Accounting For Income TaxDocument5 pagesAccounting For Income TaxMa. Kristine GarciaNo ratings yet

- Accounting For Taxes On IncomeDocument24 pagesAccounting For Taxes On IncomeKRISHNAKUMARNo ratings yet

- Income Taxes (Ias - 12) : Page 1 of 25Document25 pagesIncome Taxes (Ias - 12) : Page 1 of 25ErslanNo ratings yet

- Accounting Adjustments in Financial StatementsDocument26 pagesAccounting Adjustments in Financial Statementsshaannivas100% (1)

- Adjustments For Final AccountsDocument48 pagesAdjustments For Final AccountsArsalan QaziNo ratings yet

- Module 04 Income Tax Compliance RevisedDocument25 pagesModule 04 Income Tax Compliance RevisedSly BlueNo ratings yet

- Topic 5 Tutorial SolutionsDocument16 pagesTopic 5 Tutorial SolutionsKitty666No ratings yet

- BCOM - BCOM Accounting 3Document322 pagesBCOM - BCOM Accounting 3Ntokozo Siphiwo Collin DlaminiNo ratings yet

- Net Income NI Definition Uses and How To Calculate ItDocument4 pagesNet Income NI Definition Uses and How To Calculate IthieutlbkreportNo ratings yet

- Pas 12Document29 pagesPas 12Justine VeralloNo ratings yet

- Accounting Standard - 22 PPT PresentationDocument25 pagesAccounting Standard - 22 PPT PresentationHimanshu Agrawal0% (1)

- Costing FinalDocument46 pagesCosting FinalKaran KhatriNo ratings yet

- Section: 139 (Appointment of Auditors)Document19 pagesSection: 139 (Appointment of Auditors)Karan KhatriNo ratings yet

- The Eurocurrency Market: Essays in International Finan CE No. 125, December 1977Document53 pagesThe Eurocurrency Market: Essays in International Finan CE No. 125, December 1977Karan KhatriNo ratings yet

- Regionalism Versus Multilateralism: Jagdish BhagwatiDocument22 pagesRegionalism Versus Multilateralism: Jagdish BhagwatiKaran KhatriNo ratings yet

- Name: STD: Div: Roll No.: Subject: Topic: Name of CollegeDocument18 pagesName: STD: Div: Roll No.: Subject: Topic: Name of CollegeKaran KhatriNo ratings yet

- Definition of Balance of PaymentsDocument29 pagesDefinition of Balance of PaymentsKaran KhatriNo ratings yet

- SM Payal FinalDocument25 pagesSM Payal FinalKaran KhatriNo ratings yet

- Ali Enterprises: Sale and Service of Old Refrigerator, Ac & Washing MachinesDocument2 pagesAli Enterprises: Sale and Service of Old Refrigerator, Ac & Washing MachinesKaran KhatriNo ratings yet

- SM Payal FinalDocument25 pagesSM Payal FinalKaran KhatriNo ratings yet

- 12 - Chapter 3Document30 pages12 - Chapter 3Karan KhatriNo ratings yet

- Due Date For Payment of Service Tax & IntDocument3 pagesDue Date For Payment of Service Tax & IntKaran KhatriNo ratings yet

- Income From Business or ProfessionDocument7 pagesIncome From Business or ProfessionSwathi JayaprakashNo ratings yet

- Point of Taxation Rules: CA.J. BalasubramanianDocument13 pagesPoint of Taxation Rules: CA.J. BalasubramanianKaran KhatriNo ratings yet

- Measures of Central Tendency Dispersion and CorrelationDocument27 pagesMeasures of Central Tendency Dispersion and CorrelationFranco Martin Mutiso100% (1)

- Curriculum Vitae: Sagar ChhabriaDocument3 pagesCurriculum Vitae: Sagar ChhabriaKaran KhatriNo ratings yet

- TaxDocument27 pagesTaxKaran KhatriNo ratings yet

- DepreciationDocument5 pagesDepreciationKaran KhatriNo ratings yet

- CaroDocument19 pagesCaroKaran KhatriNo ratings yet

- Eco Payal FinalDocument27 pagesEco Payal FinalKaran KhatriNo ratings yet

- Let Us Think Big and Consolidate Our Skills, Energies and Strengths To Become Bigger and BetterDocument2 pagesLet Us Think Big and Consolidate Our Skills, Energies and Strengths To Become Bigger and BetterKaran KhatriNo ratings yet

- CaroDocument4 pagesCaroKaran KhatriNo ratings yet

- FA Final PayalDocument24 pagesFA Final PayalKaran Khatri100% (1)

- Introduction Scope of This SA230Document3 pagesIntroduction Scope of This SA230Karan KhatriNo ratings yet

- Audit of General Insurance CompanyDocument35 pagesAudit of General Insurance CompanyKaran KhatriNo ratings yet

- Costing FinalDocument46 pagesCosting FinalKaran KhatriNo ratings yet

- DK EDC Policy BriefDocument17 pagesDK EDC Policy Briefimranfalak1990No ratings yet

- Cos Cost Records Audit Amendment Rules 2014 Changes SummaryDocument77 pagesCos Cost Records Audit Amendment Rules 2014 Changes SummaryKaran KhatriNo ratings yet

- Research DesignDocument35 pagesResearch DesignHarshad MenatNo ratings yet

- Cos Cost Records Audit Amendment Rules 2014 Changes SummaryDocument2 pagesCos Cost Records Audit Amendment Rules 2014 Changes SummaryKaran KhatriNo ratings yet

- Material Flow Analysis Adapted To An Industrial Area: Cristina Sendra, Xavier Gabarrell, Teresa VicentDocument10 pagesMaterial Flow Analysis Adapted To An Industrial Area: Cristina Sendra, Xavier Gabarrell, Teresa VicentramiraliNo ratings yet

- Collaborative Co-Working SpacesDocument11 pagesCollaborative Co-Working Spacesvarada ghalsasiNo ratings yet

- Payout Policy: © 2019 Pearson Education LTDDocument7 pagesPayout Policy: © 2019 Pearson Education LTDLeanne TehNo ratings yet

- Services Proforma Invoice Template WordDocument2 pagesServices Proforma Invoice Template WordVân Anh PhạmNo ratings yet

- ILS Examination For Budget AssistantDocument7 pagesILS Examination For Budget AssistantTahinay KarlNo ratings yet

- Evaluating The Influence of Aluminum Formwork Technology On ConstructionDocument5 pagesEvaluating The Influence of Aluminum Formwork Technology On ConstructionSeid Abdurahman SeidNo ratings yet

- PrinciplesofFinance WEBDocument643 pagesPrinciplesofFinance WEBGLADYS JAMES100% (2)

- MoCredito OrganizedDocument16 pagesMoCredito Organizedkago khachanaNo ratings yet

- Principles of Marketing 1 Customer Relationship: Senior High SchoolDocument12 pagesPrinciples of Marketing 1 Customer Relationship: Senior High SchoolPauuwieeeeNo ratings yet

- 3.2.4 PracticeDocument2 pages3.2.4 PracticeKyrieSwerving100% (1)

- Letter of Transmittal BUS201Document25 pagesLetter of Transmittal BUS201Afrin ZahraNo ratings yet

- Accrued Income: College of Business Studies BS Accountancy Midterm ExaminationDocument4 pagesAccrued Income: College of Business Studies BS Accountancy Midterm ExaminationPineda, King Moises PangilinanNo ratings yet

- Template of Welcome Care PackageDocument2 pagesTemplate of Welcome Care PackageDanicaNo ratings yet

- FFMFM Section1 Group2Document21 pagesFFMFM Section1 Group222204 NIDASH PRASHARNo ratings yet

- Project Report Lecico FinalDocument52 pagesProject Report Lecico FinalMoustafa HelmyNo ratings yet

- Thesis On Exchange Rate DeterminationDocument5 pagesThesis On Exchange Rate DeterminationYolanda Ivey100% (2)

- M1 Case AnalysisDocument27 pagesM1 Case AnalysisWILYN MAE JIEN GASATAN100% (1)

- OD4493 Solar Farm Developers in The US Industry ReportDocument41 pagesOD4493 Solar Farm Developers in The US Industry Reportkulzinder kaurNo ratings yet

- FIN 390 DeVry University Fixed Income Securities in Apple Inc Research PaperDocument3 pagesFIN 390 DeVry University Fixed Income Securities in Apple Inc Research PaperEassignmentsNo ratings yet

- Basel 3Document287 pagesBasel 3boniadityaNo ratings yet

- Knowledge Value Chain' Framework For Tendering in Construction Organisations: Quantity Surveying PerspectiveDocument157 pagesKnowledge Value Chain' Framework For Tendering in Construction Organisations: Quantity Surveying PerspectiveBimsara MalithNo ratings yet

- Purchase Order: Page 1 of 24Document24 pagesPurchase Order: Page 1 of 24Joyal ThomasNo ratings yet

- The Concept of Money in IslamDocument2 pagesThe Concept of Money in IslamhvjcfgchvghmjbhnNo ratings yet

- Case Study Engro FoodsDocument5 pagesCase Study Engro FoodsMaryam KhanNo ratings yet

- Chapter 5 Summary - Catharina ChrisidaputriDocument3 pagesChapter 5 Summary - Catharina ChrisidaputriCatharina CBNo ratings yet

- Topic 1 - Audit of Cash Transactions and BalancesDocument6 pagesTopic 1 - Audit of Cash Transactions and BalancesChelsea PagcaliwaganNo ratings yet

- CRUCIGRAMADocument1 pageCRUCIGRAMAPatricia BeltranNo ratings yet

- Income Tax Notification No - SO858 25-03-2009Document25 pagesIncome Tax Notification No - SO858 25-03-2009Sanjay AjudiaNo ratings yet

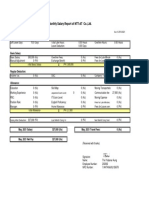

- Thiri Yadanar Aung - Salary Slip - May 2021Document1 pageThiri Yadanar Aung - Salary Slip - May 2021thiriNo ratings yet

- Stock Price Number of Shares Outstanding Stock A $ 4 0 2 0 0 Stock B $ 7 0 5 0 0 Stock C $ 1 0 6 0 0Document8 pagesStock Price Number of Shares Outstanding Stock A $ 4 0 2 0 0 Stock B $ 7 0 5 0 0 Stock C $ 1 0 6 0 0likaNo ratings yet

- Tax Strategies: The Essential Guide to All Things Taxes, Learn the Secrets and Expert Tips to Understanding and Filing Your Taxes Like a ProFrom EverandTax Strategies: The Essential Guide to All Things Taxes, Learn the Secrets and Expert Tips to Understanding and Filing Your Taxes Like a ProRating: 4.5 out of 5 stars4.5/5 (43)

- Small Business Taxes: The Most Complete and Updated Guide with Tips and Tax Loopholes You Need to Know to Avoid IRS Penalties and Save MoneyFrom EverandSmall Business Taxes: The Most Complete and Updated Guide with Tips and Tax Loopholes You Need to Know to Avoid IRS Penalties and Save MoneyNo ratings yet

- How to get US Bank Account for Non US ResidentFrom EverandHow to get US Bank Account for Non US ResidentRating: 5 out of 5 stars5/5 (1)

- Taxes for Small Businesses QuickStart Guide: Understanding Taxes for Your Sole Proprietorship, StartUp & LLCFrom EverandTaxes for Small Businesses QuickStart Guide: Understanding Taxes for Your Sole Proprietorship, StartUp & LLCRating: 4 out of 5 stars4/5 (5)

- Tax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesFrom EverandTax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesNo ratings yet

- How to Pay Zero Taxes, 2020-2021: Your Guide to Every Tax Break the IRS AllowsFrom EverandHow to Pay Zero Taxes, 2020-2021: Your Guide to Every Tax Break the IRS AllowsNo ratings yet

- Taxes for Small Business: The Ultimate Guide to Small Business Taxes Including LLC Taxes, Payroll Taxes, and Self-Employed Taxes as a Sole ProprietorshipFrom EverandTaxes for Small Business: The Ultimate Guide to Small Business Taxes Including LLC Taxes, Payroll Taxes, and Self-Employed Taxes as a Sole ProprietorshipNo ratings yet

- U.S. Taxes for Worldly Americans: The Traveling Expat's Guide to Living, Working, and Staying Tax Compliant AbroadFrom EverandU.S. Taxes for Worldly Americans: The Traveling Expat's Guide to Living, Working, and Staying Tax Compliant AbroadNo ratings yet

- The Panama Papers: Breaking the Story of How the Rich and Powerful Hide Their MoneyFrom EverandThe Panama Papers: Breaking the Story of How the Rich and Powerful Hide Their MoneyRating: 4 out of 5 stars4/5 (52)

- Bookkeeping: Step by Step Guide to Bookkeeping Principles & Basic Bookkeeping for Small BusinessFrom EverandBookkeeping: Step by Step Guide to Bookkeeping Principles & Basic Bookkeeping for Small BusinessRating: 5 out of 5 stars5/5 (5)

- Lower Your Taxes - BIG TIME! 2023-2024: Small Business Wealth Building and Tax Reduction Secrets from an IRS InsiderFrom EverandLower Your Taxes - BIG TIME! 2023-2024: Small Business Wealth Building and Tax Reduction Secrets from an IRS InsiderNo ratings yet

- The Tax and Legal Playbook: Game-Changing Solutions To Your Small Business Questions 2nd EditionFrom EverandThe Tax and Legal Playbook: Game-Changing Solutions To Your Small Business Questions 2nd EditionRating: 5 out of 5 stars5/5 (27)

- What Your CPA Isn't Telling You: Life-Changing Tax StrategiesFrom EverandWhat Your CPA Isn't Telling You: Life-Changing Tax StrategiesRating: 4 out of 5 stars4/5 (9)

- Founding Finance: How Debt, Speculation, Foreclosures, Protests, and Crackdowns Made Us a NationFrom EverandFounding Finance: How Debt, Speculation, Foreclosures, Protests, and Crackdowns Made Us a NationNo ratings yet

- The Hidden Wealth of Nations: The Scourge of Tax HavensFrom EverandThe Hidden Wealth of Nations: The Scourge of Tax HavensRating: 4 out of 5 stars4/5 (11)

- Decrypting Crypto Taxes: The Complete Guide to Cryptocurrency and NFT TaxationFrom EverandDecrypting Crypto Taxes: The Complete Guide to Cryptocurrency and NFT TaxationNo ratings yet

- Tax-Free Wealth For Life: How to Permanently Lower Your Taxes And Build More WealthFrom EverandTax-Free Wealth For Life: How to Permanently Lower Your Taxes And Build More WealthNo ratings yet

- Deduct Everything!: Save Money with Hundreds of Legal Tax Breaks, Credits, Write-Offs, and LoopholesFrom EverandDeduct Everything!: Save Money with Hundreds of Legal Tax Breaks, Credits, Write-Offs, and LoopholesRating: 3 out of 5 stars3/5 (3)

- Beat Estate Tax Forever: The Unprecedented $5 Million Opportunity in 2012From EverandBeat Estate Tax Forever: The Unprecedented $5 Million Opportunity in 2012No ratings yet

- Taxes for Small Businesses 2023: Beginners Guide to Understanding LLC, Sole Proprietorship and Startup Taxes. Cutting Edge Strategies Explained to Lower Your Taxes Legally for Business, InvestingFrom EverandTaxes for Small Businesses 2023: Beginners Guide to Understanding LLC, Sole Proprietorship and Startup Taxes. Cutting Edge Strategies Explained to Lower Your Taxes Legally for Business, InvestingRating: 5 out of 5 stars5/5 (3)

- Taxes Have Consequences: An Income Tax History of the United StatesFrom EverandTaxes Have Consequences: An Income Tax History of the United StatesNo ratings yet