You might also like

- Bfin-121 Week 1-9Document21 pagesBfin-121 Week 1-9Ruxylle Zean Elias67% (21)

- Deluxe SolutionDocument6 pagesDeluxe SolutionR K Patham100% (1)

- MTA 2020-2024 Capital Program - Full ReportDocument240 pagesMTA 2020-2024 Capital Program - Full ReportNew York Daily NewsNo ratings yet

- Maximizing Cash Inflows Through Collection MethodsDocument57 pagesMaximizing Cash Inflows Through Collection MethodsMadelle Q. PradasNo ratings yet

- Summary of Five-Year Eurobond Terms Available To R.J. ReynoldsDocument8 pagesSummary of Five-Year Eurobond Terms Available To R.J. ReynoldsRyan Putera Pratama ManafeNo ratings yet

- CDS Presentation With References PDFDocument42 pagesCDS Presentation With References PDF2401824No ratings yet

- Thruway AuditDocument15 pagesThruway AuditjspectorNo ratings yet

- MTA Financial Outlook 2012Document3 pagesMTA Financial Outlook 2012Meghan GlynnNo ratings yet

- 2020-2024 Capital Plan Letter To Chairperson FoyeDocument2 pages2020-2024 Capital Plan Letter To Chairperson FoyeGersh KuntzmanNo ratings yet

- MTA Audit Report 2013Document8 pagesMTA Audit Report 2013rbrooksvvNo ratings yet

- Financial Outlook For The Metropolitan Transportation AuthorityDocument8 pagesFinancial Outlook For The Metropolitan Transportation AuthorityjspectorNo ratings yet

- Release 2011-07-27 2012 Budget and Capital ProgramDocument3 pagesRelease 2011-07-27 2012 Budget and Capital ProgramElizabeth BenjaminNo ratings yet

- MTA Funding Letter To Governor CuomoDocument2 pagesMTA Funding Letter To Governor CuomoDavid MeyerNo ratings yet

- New York State Dedicated Highway and Bridge Trust Fund CrossroadsDocument18 pagesNew York State Dedicated Highway and Bridge Trust Fund CrossroadsNews10NBCNo ratings yet

- Are Public Private Transaction The Future Infrastructure FinanceDocument6 pagesAre Public Private Transaction The Future Infrastructure FinanceNafis El-FariqNo ratings yet

- 2016 Proposed Budget For Port AuthorityDocument104 pages2016 Proposed Budget For Port AuthorityThe Capitol PressroomNo ratings yet

- Fee Changes ReportDocument18 pagesFee Changes ReportmelissacorkerNo ratings yet

- Fiscal Decentralization Reform in Cambodia: Progress over the Past Decade and OpportunitiesFrom EverandFiscal Decentralization Reform in Cambodia: Progress over the Past Decade and OpportunitiesNo ratings yet

- House Hearing, Innovative Finance, 2010-03Document8 pagesHouse Hearing, Innovative Finance, 2010-03ehllNo ratings yet

- La Credit ReportDocument31 pagesLa Credit ReportSouthern California Public RadioNo ratings yet

- Metropolitan Transportation Authority, New York Joint Criteria TransitDocument7 pagesMetropolitan Transportation Authority, New York Joint Criteria Transitapi-227433089No ratings yet

- HSR Compilation Report July 2011Document19 pagesHSR Compilation Report July 2011Aaron FukudaNo ratings yet

- MTA 2020-2024 Capital Program - Full Report PDFDocument240 pagesMTA 2020-2024 Capital Program - Full Report PDFNew York Daily NewsNo ratings yet

- Media Statement - How Much It Costs To Run County Governments - Final FinalDocument2 pagesMedia Statement - How Much It Costs To Run County Governments - Final FinalInternational Budget Partnership KenyaNo ratings yet

- DOT FY16 BudgetFactSheetDocument5 pagesDOT FY16 BudgetFactSheetShane FerroNo ratings yet

- The PlanDocument82 pagesThe PlanMetro Los AngelesNo ratings yet

- Letter From Don HornerDocument6 pagesLetter From Don HornerHonolulu Star-AdvertiserNo ratings yet

- Office of The State ComptrollerDocument4 pagesOffice of The State ComptrollerflippinamsterdamNo ratings yet

- O'Keefe Report: Complete VersionDocument62 pagesO'Keefe Report: Complete Versionwindsorcityblog1No ratings yet

- FY14 Overview MemoDocument3 pagesFY14 Overview MemokeithmontpvtNo ratings yet

- Mid Year Financial Status ReportDocument99 pagesMid Year Financial Status ReportBill RosendahlNo ratings yet

- Critique of Canberra Capital MetroDocument14 pagesCritique of Canberra Capital MetroEric ChangNo ratings yet

- HYMONEDITSEconomic Benefits of Sales Tax Measure News ReleaseDocument3 pagesHYMONEDITSEconomic Benefits of Sales Tax Measure News ReleaseMetro Los AngelesNo ratings yet

- Dawson Creek 2016 Draft Financial PlanDocument151 pagesDawson Creek 2016 Draft Financial PlanJonny WakefieldNo ratings yet

- Atlantic City Emergency Manager ReportDocument55 pagesAtlantic City Emergency Manager ReportPress of Atlantic CityNo ratings yet

- Budget 2014 Release1Document5 pagesBudget 2014 Release1Steve ForsethNo ratings yet

- Joint Legislative Public Hearing Notice and Testimonies For TransportaIon InfoDocument96 pagesJoint Legislative Public Hearing Notice and Testimonies For TransportaIon InfoNew York SenateNo ratings yet

- BenchmarkingDocument7 pagesBenchmarkingMelai NudosNo ratings yet

- Metro Proposed Budget FY 2016-17Document68 pagesMetro Proposed Budget FY 2016-17Metro Los AngelesNo ratings yet

- Capital Spending Report Nov2010Document23 pagesCapital Spending Report Nov2010nreismanNo ratings yet

- MtafloormemoDocument3 pagesMtafloormemoElizabeth Benjamin100% (1)

- C A Huge Debt Burden: P ON Pakistan's EconomyDocument5 pagesC A Huge Debt Burden: P ON Pakistan's EconomySaira SairNo ratings yet

- Lakeport City Council - Final BudgetDocument119 pagesLakeport City Council - Final BudgetLakeCoNewsNo ratings yet

- Knapik Press Release: Knapik Secures Funding in Supplemental Budget For Victory Theatre Restoration EffortDocument4 pagesKnapik Press Release: Knapik Secures Funding in Supplemental Budget For Victory Theatre Restoration EffortMike KnapikNo ratings yet

- IDC Historic Rehabilitation Tax Credit Report - March 16, 2011Document16 pagesIDC Historic Rehabilitation Tax Credit Report - March 16, 2011robertharding22No ratings yet

- A Position Paper On The Proposed Transfer of CMGP To DPWH: By: Anthea C. Bermudo and Cassie Anne L. BuenafeDocument4 pagesA Position Paper On The Proposed Transfer of CMGP To DPWH: By: Anthea C. Bermudo and Cassie Anne L. BuenafeKyla Marie B. FRANCONo ratings yet

- Article Published On 2017Document2 pagesArticle Published On 2017ANNA BIANCA GONo ratings yet

- 1-31-2024 Cover Letter Gdc-Ftacigfinplan FinalDocument3 pages1-31-2024 Cover Letter Gdc-Ftacigfinplan Finalcwilson2No ratings yet

- PJW Assessment WhitePaperDocument6 pagesPJW Assessment WhitePaperMetro ForwardNo ratings yet

- PMF A8 Poland's A2 MotorwayDocument6 pagesPMF A8 Poland's A2 MotorwaySanjeet Kumar100% (1)

- Final AssignmentDocument6 pagesFinal AssignmentZANGINA Nicholas NaaniNo ratings yet

- Resolution No. R2020-27: Proposed ActionDocument10 pagesResolution No. R2020-27: Proposed ActionThe UrbanistNo ratings yet

- Ansonia, CT - S&P Rating Report August 2016Document6 pagesAnsonia, CT - S&P Rating Report August 2016The Valley IndyNo ratings yet

- Annual Report On Funding Recommendations: Fiscal Year 2017Document19 pagesAnnual Report On Funding Recommendations: Fiscal Year 2017Stella Padilla 4 MayorNo ratings yet

- New Infrastructure Plan - ENDocument16 pagesNew Infrastructure Plan - ENSourav NandiNo ratings yet

- America-Transportation and Infrastructure FinanceDocument44 pagesAmerica-Transportation and Infrastructure FinanceDeo AvanteNo ratings yet

- California High Speed RailwayDocument7 pagesCalifornia High Speed RailwayMorricce KashNo ratings yet

- Executive Summary - Honolulu Rail Transit Financial Plan AssessmentDocument21 pagesExecutive Summary - Honolulu Rail Transit Financial Plan AssessmentCraig GimaNo ratings yet

- SMART Draft 2019 Strategic PlanDocument28 pagesSMART Draft 2019 Strategic PlanWill HoustonNo ratings yet

- 'Fiscally Irresponsible': Ortega Memo On RTADocument11 pages'Fiscally Irresponsible': Ortega Memo On RTATucsonSentinelNo ratings yet

- Draft Capital Improvement PlanDocument134 pagesDraft Capital Improvement PlanCape Cod TimesNo ratings yet

- Gateway Financial Plan 2021 Submittal LetterDocument4 pagesGateway Financial Plan 2021 Submittal LetterGersh KuntzmanNo ratings yet

- 2015 Proposed Modified Budget PDFDocument47 pages2015 Proposed Modified Budget PDFjspectorNo ratings yet

- King County Metro Budget 2021-2022 BriefDocument3 pagesKing County Metro Budget 2021-2022 BriefThe UrbanistNo ratings yet

- International Public Sector Accounting Standards Implementation Road Map for UzbekistanFrom EverandInternational Public Sector Accounting Standards Implementation Road Map for UzbekistanNo ratings yet

- IG LetterDocument3 pagesIG Letterjspector100% (1)

- Class of 2022Document1 pageClass of 2022jspectorNo ratings yet

- Cornell ComplaintDocument41 pagesCornell Complaintjspector100% (1)

- Joseph Ruggiero Employment AgreementDocument6 pagesJoseph Ruggiero Employment AgreementjspectorNo ratings yet

- Siena Poll March 27, 2017Document7 pagesSiena Poll March 27, 2017jspectorNo ratings yet

- Inflation AllowablegrowthfactorsDocument1 pageInflation AllowablegrowthfactorsjspectorNo ratings yet

- State Health CoverageDocument26 pagesState Health CoveragejspectorNo ratings yet

- Pennies For Charity 2018Document12 pagesPennies For Charity 2018ZacharyEJWilliamsNo ratings yet

- Federal Budget Fiscal Year 2017 Web VersionDocument36 pagesFederal Budget Fiscal Year 2017 Web VersionjspectorNo ratings yet

- Abo 2017 Annual ReportDocument65 pagesAbo 2017 Annual ReportrkarlinNo ratings yet

- 2017 08 18 Constitution OrderDocument27 pages2017 08 18 Constitution OrderjspectorNo ratings yet

- Hiffa Settlement Agreement ExecutedDocument5 pagesHiffa Settlement Agreement ExecutedNick Reisman0% (1)

- Film Tax Credit - Quarterly Report, Calendar Year 2017 2nd Quarter PDFDocument8 pagesFilm Tax Credit - Quarterly Report, Calendar Year 2017 2nd Quarter PDFjspectorNo ratings yet

- NYSCrimeReport2016 PrelimDocument14 pagesNYSCrimeReport2016 PrelimjspectorNo ratings yet

- SNY0517 Crosstabs 052417Document4 pagesSNY0517 Crosstabs 052417Nick ReismanNo ratings yet

- Teacher Shortage Report 05232017 PDFDocument16 pagesTeacher Shortage Report 05232017 PDFjspectorNo ratings yet

- Oag Sed Letter Ice 2-27-17Document3 pagesOag Sed Letter Ice 2-27-17BethanyNo ratings yet

- Opiods 2017-04-20-By Numbers Brief No8Document17 pagesOpiods 2017-04-20-By Numbers Brief No8rkarlinNo ratings yet

- Activity Overview: Key Metrics Historical Sparkbars 1-2016 1-2017 YTD 2016 YTD 2017Document4 pagesActivity Overview: Key Metrics Historical Sparkbars 1-2016 1-2017 YTD 2016 YTD 2017jspectorNo ratings yet

- Schneiderman Voter Fraud Letter 022217Document2 pagesSchneiderman Voter Fraud Letter 022217Matthew HamiltonNo ratings yet

- 2017 School Bfast Report Online Version 3-7-17 0Document29 pages2017 School Bfast Report Online Version 3-7-17 0jspectorNo ratings yet

- Youth Cigarette and E-Cigs UseDocument1 pageYouth Cigarette and E-Cigs UsejspectorNo ratings yet

- 16 273 Amicus Brief of SF NYC and 29 Other JurisdictionsDocument55 pages16 273 Amicus Brief of SF NYC and 29 Other JurisdictionsjspectorNo ratings yet

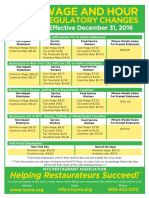

- Wage and Hour Regulatory Changes 2016Document2 pagesWage and Hour Regulatory Changes 2016jspectorNo ratings yet

- p12 Budget Testimony 2-14-17Document31 pagesp12 Budget Testimony 2-14-17jspectorNo ratings yet

- Darweesh Cities AmicusDocument32 pagesDarweesh Cities AmicusjspectorNo ratings yet

- Review of Executive Budget 2017Document102 pagesReview of Executive Budget 2017Nick ReismanNo ratings yet

- Voting Report CardDocument1 pageVoting Report CardjspectorNo ratings yet

- 2016 Local Sales Tax CollectionsDocument4 pages2016 Local Sales Tax CollectionsjspectorNo ratings yet

- Pub Auth Num 2017Document54 pagesPub Auth Num 2017jspectorNo ratings yet

- Solutions For End-of-Chapter Questions and Problems: Chapter TenDocument29 pagesSolutions For End-of-Chapter Questions and Problems: Chapter Tenester jofreyNo ratings yet

- Compromise, Arrangement & AmalgamationDocument12 pagesCompromise, Arrangement & AmalgamationKomal BhattadNo ratings yet

- Karely Ordaz SEI 2012-2013Document3 pagesKarely Ordaz SEI 2012-2013RecordTrac - City of OaklandNo ratings yet

- Spring 2016 - BNK619 - 4 - MC140401473Document13 pagesSpring 2016 - BNK619 - 4 - MC140401473Khalid MahmoodNo ratings yet

- Fund Raising & Overview of IPO: Sharing NTPC ExperienceDocument38 pagesFund Raising & Overview of IPO: Sharing NTPC ExperienceSamNo ratings yet

- APPLE DubaiDocument17 pagesAPPLE DubaiAaiyyat fatimaNo ratings yet

- Laporan Keuangan ESTI 2019 - Audited PDFDocument80 pagesLaporan Keuangan ESTI 2019 - Audited PDFmichele hazelNo ratings yet

- Wonder Book Corp. vs. Philippine Bank of Communications (676 SCRA 489 (2012) )Document3 pagesWonder Book Corp. vs. Philippine Bank of Communications (676 SCRA 489 (2012) )CHARMAINE MERICK HOPE BAYOGNo ratings yet

- Tacn1 HVTCDocument9 pagesTacn1 HVTCNgô Khánh HuyềnNo ratings yet

- MY Own CMADocument15 pagesMY Own CMASaorabh KumarNo ratings yet

- Ratio AnalysisDocument48 pagesRatio AnalysiskeerthiNo ratings yet

- Hybrid Financing:: Preferred Stock, Leasing, Warrants, and ConvertiblesDocument29 pagesHybrid Financing:: Preferred Stock, Leasing, Warrants, and ConvertiblesAli HussainNo ratings yet

- Conclusion: Rising CostsDocument2 pagesConclusion: Rising CostswahidNo ratings yet

- Breadtalk KEDocument8 pagesBreadtalk KEChanthirasekar சந்திரசேகர்No ratings yet

- International Financing: - by Prem Shankar (12IEC038)Document19 pagesInternational Financing: - by Prem Shankar (12IEC038)premNo ratings yet

- Research Methodology: IMS AND Bjectives Ntecedent EBTDocument23 pagesResearch Methodology: IMS AND Bjectives Ntecedent EBTsagorika7basuNo ratings yet

- Sarah Stone - Personal BankruptcyDocument2 pagesSarah Stone - Personal Bankruptcyapi-552019617No ratings yet

- 1995 - Stern and Stewart - EVADocument17 pages1995 - Stern and Stewart - EVAAbdulAzeemNo ratings yet

- CRAB Performance AnalysisDocument47 pagesCRAB Performance AnalysisZordanNo ratings yet

- SSRN Id1012937Document176 pagesSSRN Id1012937Nye LavalleNo ratings yet

- Cpar - BLT 09.14.13Document14 pagesCpar - BLT 09.14.13Charry Ramos100% (1)

- Bank of England Charters and Government FinancesDocument39 pagesBank of England Charters and Government FinancesNguyen Ha QuanNo ratings yet

- Smart Buy LawsuitDocument26 pagesSmart Buy LawsuitjspectorNo ratings yet

- CH12 13 14 - 2023Document34 pagesCH12 13 14 - 2023Siviwe DubeNo ratings yet

- Financial Planning & Wealth ManagementDocument20 pagesFinancial Planning & Wealth ManagementHetviNo ratings yet