You might also like

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5782)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (890)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (72)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Joint Product CostingDocument3 pagesJoint Product CostingClint-Daniel AbenojaNo ratings yet

- 9303 PDFDocument3 pages9303 PDFEong Huat Corporation Sdn BhdNo ratings yet

- Business Plan Cafe ClassicDocument20 pagesBusiness Plan Cafe ClassicPratyushJoshiNo ratings yet

- Mcdonald and Dominos1111Document31 pagesMcdonald and Dominos1111Gulshan PushpNo ratings yet

- The New Standard for Retail MeasurementDocument2 pagesThe New Standard for Retail MeasurementPercy SuarezNo ratings yet

- Business LawDocument180 pagesBusiness LawNagashree RANo ratings yet

- Law On SALES Midterm ExamsDocument7 pagesLaw On SALES Midterm ExamsKitem Kadatuan Jr.100% (2)

- Basic Data 1/2 (Screen 1Document9 pagesBasic Data 1/2 (Screen 1DiptimayeeGuptaNo ratings yet

- India's Emerging Consumer Revolution and the Evolution of Sales ManagementDocument16 pagesIndia's Emerging Consumer Revolution and the Evolution of Sales Managementmaheshseth293No ratings yet

- Managing Products, Product Lines, Brands, PackagingDocument16 pagesManaging Products, Product Lines, Brands, PackagingAbhisek DeyNo ratings yet

- Sales Force MotivatorsDocument15 pagesSales Force MotivatorsAshirbadNo ratings yet

- Civrev02 MCQSDocument12 pagesCivrev02 MCQSmjpjoreNo ratings yet

- Group 7 Tutorial AnswersDocument27 pagesGroup 7 Tutorial AnswersKwang Yi Juin0% (1)

- MBA (Spring 13)Document39 pagesMBA (Spring 13)Affan WassafNo ratings yet

- Amy Muchko Resume 2Document2 pagesAmy Muchko Resume 2Amy MuchkoNo ratings yet

- (GR No. L-24069, Jun 28, 1968) La Fuerza V. Ca: DecisionDocument6 pages(GR No. L-24069, Jun 28, 1968) La Fuerza V. Ca: DecisionSocNo ratings yet

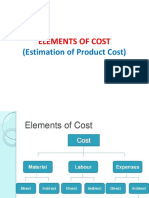

- Elements of CostDocument42 pagesElements of CostNinad MirajgaonkarNo ratings yet

- Evaluation of The Wholesale Market System For Fresh Fruits and Vegetables in Turkey A Case Study From Antalya Metropolitan MunicipalityDocument12 pagesEvaluation of The Wholesale Market System For Fresh Fruits and Vegetables in Turkey A Case Study From Antalya Metropolitan MunicipalityDharshanNo ratings yet

- Final Exam Review: 1. Identify Managers' Three Primary Responsibilities. A. Planning B. Directing C. ControllingDocument4 pagesFinal Exam Review: 1. Identify Managers' Three Primary Responsibilities. A. Planning B. Directing C. ControllingSandip AgarwalNo ratings yet

- Womens Shoe Store Business PlanDocument28 pagesWomens Shoe Store Business PlanShaikha S ADNo ratings yet

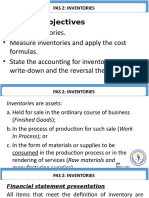

- PAS 2 Inventories Cost FormulasDocument14 pagesPAS 2 Inventories Cost FormulasDovelyn Dorin0% (1)

- Biggest GST FraudDocument2 pagesBiggest GST FraudNatrajNo ratings yet

- David Sm14 Inppt05 GEDocument50 pagesDavid Sm14 Inppt05 GERashidahNo ratings yet

- Loyalty User GuideDocument150 pagesLoyalty User Guidemanu_130381No ratings yet

- ICA Zesta Fabrics CaseDocument2 pagesICA Zesta Fabrics CasemiledNo ratings yet

- Streetphotography by Daniel HoffmannDocument94 pagesStreetphotography by Daniel Hoffmannhancillo100% (1)

- Amoria bond interview preparationDocument10 pagesAmoria bond interview preparationdaniel-lowe-5053No ratings yet

- B2B Marketing - Mohan Kuruvilla PDFDocument11 pagesB2B Marketing - Mohan Kuruvilla PDFlhgeekNo ratings yet

- CasesDocument5 pagesCasesJeffery ZeledonNo ratings yet

- Article 1632 - 1635Document3 pagesArticle 1632 - 1635lexscribisNo ratings yet