You might also like

- Cusip Rfo 5221392Document12 pagesCusip Rfo 5221392Chemtrails Equals Treason100% (2)

- ACCA AAA MJ19 Notes PDFDocument156 pagesACCA AAA MJ19 Notes PDFOmer ZaheerNo ratings yet

- Momentum Factor Basics and Robeco SolutionDocument7 pagesMomentum Factor Basics and Robeco Solutionbodo0% (1)

- Investing in Junk Bonds: Inside the High Yield Debt MarketFrom EverandInvesting in Junk Bonds: Inside the High Yield Debt MarketRating: 3 out of 5 stars3/5 (1)

- Algorithmic Trading & DMA: An Introduction To Direct Access and Trading StrategiesDocument595 pagesAlgorithmic Trading & DMA: An Introduction To Direct Access and Trading Strategiesbig_pete__100% (6)

- The Sector Strategist: Using New Asset Allocation Techniques to Reduce Risk and Improve Investment ReturnsFrom EverandThe Sector Strategist: Using New Asset Allocation Techniques to Reduce Risk and Improve Investment ReturnsRating: 4 out of 5 stars4/5 (1)

- The Case For Low-Cost Index Fund Investing - Thierry PollaDocument19 pagesThe Case For Low-Cost Index Fund Investing - Thierry PollaThierry Polla100% (1)

- 5 Investment Books For 2021Document4 pages5 Investment Books For 2021Yassine MafraxNo ratings yet

- IPT Stocks 2012Document16 pagesIPT Stocks 2012reachernieNo ratings yet

- Building A Global Core-Satellite Portfolio: Executive SummaryDocument12 pagesBuilding A Global Core-Satellite Portfolio: Executive SummarydospxNo ratings yet

- Qis - Insights - Qis Insights Style InvestingDocument21 pagesQis - Insights - Qis Insights Style Investingpderby1No ratings yet

- HFTDocument257 pagesHFThengcheong100% (8)

- Natural Gas Market of EuropeDocument124 pagesNatural Gas Market of EuropeSuvam PatelNo ratings yet

- 9 Factors To Consider When Comparing McKinsey - Bain - BCG - Management ConsultedDocument7 pages9 Factors To Consider When Comparing McKinsey - Bain - BCG - Management ConsultedTarekNo ratings yet

- Investment Consulting Business PlanDocument9 pagesInvestment Consulting Business Planbe_supercoolNo ratings yet

- Civ2 Atty - Rabanes 1st MeetingDocument8 pagesCiv2 Atty - Rabanes 1st MeetingEleasar Banasen PidoNo ratings yet

- R. Driehaus, Unconventional Wisdom in The Investment ProcessDocument6 pagesR. Driehaus, Unconventional Wisdom in The Investment Processbagelboy2No ratings yet

- Assessment Paper and Instructions To Candidates:: FM320 - Quantitative Finance Suitable For All CandidatesDocument5 pagesAssessment Paper and Instructions To Candidates:: FM320 - Quantitative Finance Suitable For All CandidatesYingzhi XuNo ratings yet

- Smart Beta: The DefinitiveDocument12 pagesSmart Beta: The DefinitiveleofranklingNo ratings yet

- Blog - Quality For Uncertain TimesDocument6 pagesBlog - Quality For Uncertain TimesOwm Close CorporationNo ratings yet

- Morningstar ReportDocument30 pagesMorningstar ReportAJNo ratings yet

- The Case For Low-Cost Index-Fund Investing: Vanguard Research April 2019Document20 pagesThe Case For Low-Cost Index-Fund Investing: Vanguard Research April 2019budNo ratings yet

- Mason Hawkins 11q3letterDocument4 pagesMason Hawkins 11q3letterrodrigoescobarn142No ratings yet

- Market Timing Opportunities and RisksDocument19 pagesMarket Timing Opportunities and RisksJohn DargyNo ratings yet

- Delgado - Forex: The Fundamental Analysis.Document10 pagesDelgado - Forex: The Fundamental Analysis.Franklin Delgado VerasNo ratings yet

- Introduction To Financial Management Finance 240 Project 3Document4 pagesIntroduction To Financial Management Finance 240 Project 3JosephNo ratings yet

- Fpa Capital Fund Commentary 2017 q1Document12 pagesFpa Capital Fund Commentary 2017 q1superinvestorbulletiNo ratings yet

- Morningstar Manager Research - A Global Guide To Strategic Beta Exchange-Traded ProductsDocument62 pagesMorningstar Manager Research - A Global Guide To Strategic Beta Exchange-Traded ProductsSpartacusTraciaNo ratings yet

- BCG Notes FinalDocument10 pagesBCG Notes FinalHarsora UrvilNo ratings yet

- 2013 q2 Crescent Commentary Steve RomickDocument16 pages2013 q2 Crescent Commentary Steve RomickCanadianValueNo ratings yet

- Q2 2015 KAM Conference Call 07-07-15 FINALDocument18 pagesQ2 2015 KAM Conference Call 07-07-15 FINALCanadianValueNo ratings yet

- File 1Document10 pagesFile 1Alberto VillalpandoNo ratings yet

- Case For High Conviction InvestingDocument2 pagesCase For High Conviction Investingkenneth1195No ratings yet

- Practice Essentials Birds Eye View Income InvestingDocument11 pagesPractice Essentials Birds Eye View Income InvestingzencrackerNo ratings yet

- Tilson Funds Annual Report 2005Document28 pagesTilson Funds Annual Report 2005josepmcdalena6542No ratings yet

- MPT Theory & FDI AdvantagesDocument9 pagesMPT Theory & FDI AdvantagesAlinaVieruNo ratings yet

- Comparison of Five Popular StrategiesDocument12 pagesComparison of Five Popular StrategiesNam Dang ThanhNo ratings yet

- How to Make Money in Stocks: A Successful Strategy for Prosperous and Challenging TimesFrom EverandHow to Make Money in Stocks: A Successful Strategy for Prosperous and Challenging TimesNo ratings yet

- SAPM - Security AnalysisDocument7 pagesSAPM - Security AnalysisTyson Texeira100% (1)

- Stock Market Thesis StatementDocument7 pagesStock Market Thesis StatementCanIPaySomeoneToWriteMyPaperCanada100% (2)

- E2011 - Developing An Active Management System For Stock Market, 2011 (NAAM Conference)Document18 pagesE2011 - Developing An Active Management System For Stock Market, 2011 (NAAM Conference)Michael BarfußNo ratings yet

- BCG Notes ActivityDocument7 pagesBCG Notes ActivityIda TakahashiNo ratings yet

- Star Appliance Cost of Capital AnalysisDocument8 pagesStar Appliance Cost of Capital AnalysisGiga KutkhashviliNo ratings yet

- ETF Strategy Randy BullardDocument14 pagesETF Strategy Randy BullardRandy Bullard0% (1)

- Bahan Presentasi MipmDocument35 pagesBahan Presentasi MipmagustinaNo ratings yet

- Scivest Edu Market NeutralDocument29 pagesScivest Edu Market Neutralusag1rNo ratings yet

- The Case of Discount Dividend-Reinvestment and Stock - Purchase PlansDocument29 pagesThe Case of Discount Dividend-Reinvestment and Stock - Purchase Plansrooos123No ratings yet

- Value Investing The Use of Historical Financial Statement Information PDFDocument41 pagesValue Investing The Use of Historical Financial Statement Information PDFgargNo ratings yet

- A Project Report On Technical Analysis at Cement Sector in Share KhanDocument105 pagesA Project Report On Technical Analysis at Cement Sector in Share KhanBabasab Patil (Karrisatte)100% (1)

- A Project Report On Technical Analysis at Share KhanDocument105 pagesA Project Report On Technical Analysis at Share KhanBabasab Patil (Karrisatte)100% (3)

- Elton-Are Investors Rational 1Document36 pagesElton-Are Investors Rational 1Abey FrancisNo ratings yet

- The Morningstar Rating For Funds: BackgroundDocument2 pagesThe Morningstar Rating For Funds: BackgroundLast_DonNo ratings yet

- Analyzing Mutual Fund Performance Against Established Performance Benchmarks: A Test of Market EfficiencyDocument15 pagesAnalyzing Mutual Fund Performance Against Established Performance Benchmarks: A Test of Market EfficiencyChandu KamathNo ratings yet

- ALASKA Daily Gov-Corp Bond FundDocument2 pagesALASKA Daily Gov-Corp Bond FundDeadlyClearNo ratings yet

- SWOT AnalysisDocument10 pagesSWOT AnalysisRizwan KhanNo ratings yet

- Review of LiteratureDocument12 pagesReview of LiteratureRanjit Superanjit100% (1)

- What Is 'Fundamental Analysis': Intrinsic Value Macroeconomic Factors Current PriceDocument9 pagesWhat Is 'Fundamental Analysis': Intrinsic Value Macroeconomic Factors Current Pricedhwani100% (1)

- Equity Research On Paint and FMCG SectorDocument43 pagesEquity Research On Paint and FMCG SectornehagadgeNo ratings yet

- Acorn Investments - Systematic TradingDocument9 pagesAcorn Investments - Systematic TradingAdam butlerNo ratings yet

- Dividend Policy and Market MovementsDocument40 pagesDividend Policy and Market MovementsHoàng NamNo ratings yet

- Khan Project WorkDocument63 pagesKhan Project WorkmubasheerzaheerNo ratings yet

- Situation Index Handbook 2014Document43 pagesSituation Index Handbook 2014kcousinsNo ratings yet

- 6-Force Framework of Levers: How to multiply stock valueDocument72 pages6-Force Framework of Levers: How to multiply stock valueabhishekbasumallick0% (1)

- Equity Research On Paint and FMCG SectorDocument47 pagesEquity Research On Paint and FMCG SectornehagadgeNo ratings yet

- Olstein: Olstein All Cap Value FundDocument40 pagesOlstein: Olstein All Cap Value Funddan4everNo ratings yet

- BBA 3005 Corporate Finance (Assignment)Document17 pagesBBA 3005 Corporate Finance (Assignment)VentusNo ratings yet

- Tactical Asset Allocation Alpha and The Greatest Trick The Devil Ever PulledDocument8 pagesTactical Asset Allocation Alpha and The Greatest Trick The Devil Ever PulledGestaltUNo ratings yet

- SSRN Id3512994Document34 pagesSSRN Id3512994Mohit GuptaNo ratings yet

- TT18 Dissertation Vu 0Document90 pagesTT18 Dissertation Vu 0Mohit GuptaNo ratings yet

- Aarav's Chapel TalkDocument3 pagesAarav's Chapel TalkMohit GuptaNo ratings yet

- Alex Gillula SeniorDesignPaper - OptimalHedgeDocument46 pagesAlex Gillula SeniorDesignPaper - OptimalHedgeMohit GuptaNo ratings yet

- Mystic Documentation - Highly-constrained non-convex optimization and uncertainty quantification libraryDocument218 pagesMystic Documentation - Highly-constrained non-convex optimization and uncertainty quantification libraryMohit GuptaNo ratings yet

- Constrained Risk Budgeting OptimizationDocument36 pagesConstrained Risk Budgeting OptimizationMohit GuptaNo ratings yet

- S&P 500 Leaders Time-lag AnalysisDocument11 pagesS&P 500 Leaders Time-lag AnalysisMohit GuptaNo ratings yet

- Evaluation and Ranking of Market ForecastersDocument26 pagesEvaluation and Ranking of Market ForecastersAnonymous pb0lJ4n5jNo ratings yet

- SSRN Id2587199Document47 pagesSSRN Id2587199Mohit GuptaNo ratings yet

- Pfaff (Should Atention)Document121 pagesPfaff (Should Atention)thienthanctomNo ratings yet

- Ftut1 PDE SolverDocument166 pagesFtut1 PDE SolverMohit GuptaNo ratings yet

- Alex Gillula SeniorDesignPaper - OptimalHedgeDocument46 pagesAlex Gillula SeniorDesignPaper - OptimalHedgeMohit GuptaNo ratings yet

- Medium Term Simulations of The Full Kelly and Fractional Kelly Investment StrategiesDocument19 pagesMedium Term Simulations of The Full Kelly and Fractional Kelly Investment StrategiesftbearNo ratings yet

- Trend Without Hiccups - A Kalman Filter ApproachDocument35 pagesTrend Without Hiccups - A Kalman Filter ApproachMohit GuptaNo ratings yet

- Vba Alm 1-11-2012Document30 pagesVba Alm 1-11-2012Mohit GuptaNo ratings yet

- SSRN-id2371227 MoM HiSharpeRatioDocument57 pagesSSRN-id2371227 MoM HiSharpeRatioMohit GuptaNo ratings yet

- Etd 2727Document120 pagesEtd 2727Alex Sanz MendezNo ratings yet

- The Cross-Sectional Profitability of Technical Analysis - SSRN-id1656460Document42 pagesThe Cross-Sectional Profitability of Technical Analysis - SSRN-id1656460Mohit GuptaNo ratings yet

- UnscentedKF SNPDocument26 pagesUnscentedKF SNPMohit GuptaNo ratings yet

- Michael Dever WhitepaperDocument4 pagesMichael Dever WhitepaperMohit GuptaNo ratings yet

- Lucas Asset Pricing ExperimentDocument40 pagesLucas Asset Pricing ExperimentMohit GuptaNo ratings yet

- Slingshot HedgeDocument6 pagesSlingshot HedgeMohit GuptaNo ratings yet

- Zivot+Yollin R ForecastingDocument90 pagesZivot+Yollin R ForecastingLamchochiya MahaanNo ratings yet

- Forecasting 2011 - Time SeriesDocument95 pagesForecasting 2011 - Time SeriesMohit GuptaNo ratings yet

- MRTS Naive SystemWMDocument18 pagesMRTS Naive SystemWMMohit GuptaNo ratings yet

- DDE Links to Excel for Live TOS DataDocument14 pagesDDE Links to Excel for Live TOS DataMohit GuptaNo ratings yet

- Skinny Math 051613 Geo Brownian MotionDocument10 pagesSkinny Math 051613 Geo Brownian MotionMohit GuptaNo ratings yet

- UG BCom Pages DeletedDocument22 pagesUG BCom Pages DeletedVijeta SinghNo ratings yet

- 8 - 8 - 31 - 2023 12 - 00 - 00 Am - 2023Document2 pages8 - 8 - 31 - 2023 12 - 00 - 00 Am - 2023Larry GatlinNo ratings yet

- Advanced Accounting Jeter 5th Edition Solutions ManualDocument37 pagesAdvanced Accounting Jeter 5th Edition Solutions Manualgordonswansonepe0q100% (9)

- Fairstone Terms and Conditions PDFDocument10 pagesFairstone Terms and Conditions PDFGarrett GilesNo ratings yet

- A Brief History of BankingDocument42 pagesA Brief History of Bankingtasaduq70% (1)

- Problem Set5 KeyDocument7 pagesProblem Set5 Keygorski29No ratings yet

- MCWQS For All XamsDocument97 pagesMCWQS For All Xamsvini_anj3980No ratings yet

- Business Environment-Monetary & Fiscal PolicyDocument10 pagesBusiness Environment-Monetary & Fiscal Policymanavazhagan0% (1)

- Accounting As The Language of BusinessDocument2 pagesAccounting As The Language of BusinessjuliahuiniNo ratings yet

- Forex Pro Shadow ManualDocument18 pagesForex Pro Shadow ManualvickyNo ratings yet

- Covid-19 and Its Impact On Indian EconomyDocument8 pagesCovid-19 and Its Impact On Indian EconomyDr Shubhi AgarwalNo ratings yet

- Audit of Shareholders' Equity Practice Problems IDocument5 pagesAudit of Shareholders' Equity Practice Problems IAngel VenableNo ratings yet

- Meaning of Business: Art. 1767, New Civil Code of The Philippines Sec.2 B.P. 68 or Corporation Code of The PhilippinesDocument25 pagesMeaning of Business: Art. 1767, New Civil Code of The Philippines Sec.2 B.P. 68 or Corporation Code of The PhilippinesAnali BarbonNo ratings yet

- Excel Academy of CommerceDocument2 pagesExcel Academy of CommerceHassan Jameel SheikhNo ratings yet

- Mishkin Econ13e PPT 11Document39 pagesMishkin Econ13e PPT 11hangbg2k3No ratings yet

- Accounting For Decision Making or Management AU Question Paper'sDocument41 pagesAccounting For Decision Making or Management AU Question Paper'sAdhithiya dhanasekarNo ratings yet

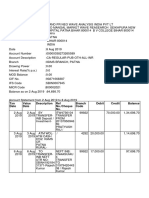

- TXN Date Value Date Description Ref No./Cheque No. Branch Code Debit Credit BalanceDocument3 pagesTXN Date Value Date Description Ref No./Cheque No. Branch Code Debit Credit BalanceNishi GuptaNo ratings yet

- FORM 10-K: United States Securities and Exchange CommissionDocument55 pagesFORM 10-K: United States Securities and Exchange CommissionJerome PadillaNo ratings yet

- AE 315 FM Sum2021 Week 3 Capital Budgeting Quiz Anserki B FOR DISTRIBDocument7 pagesAE 315 FM Sum2021 Week 3 Capital Budgeting Quiz Anserki B FOR DISTRIBArly Kurt TorresNo ratings yet

- Account Determination MM en USDocument81 pagesAccount Determination MM en USkamal_dipNo ratings yet

- IDBICapital Auto Sep2010Document73 pagesIDBICapital Auto Sep2010raj.mehta2103No ratings yet

- Summer Internship 2013-14: Amity Business School, Amity University, Lucknow Campus 1Document10 pagesSummer Internship 2013-14: Amity Business School, Amity University, Lucknow Campus 1Deepak Singh NegiNo ratings yet

- LMGTRAN Negotiable InstrumentsDocument36 pagesLMGTRAN Negotiable InstrumentsNastassja Marie DelaCruzNo ratings yet

- Haryana SSC Staff Selection ReceiptDocument1 pageHaryana SSC Staff Selection ReceiptAshu BansalNo ratings yet

- Keynesian is-LM ModelDocument45 pagesKeynesian is-LM ModelNorsurianaNo ratings yet