You might also like

- MCCM 3Q2017 Market OutlookDocument75 pagesMCCM 3Q2017 Market OutlooksuperinvestorbulletiNo ratings yet

- Baron-Fund-2Q17 Quarterly Report 1Document116 pagesBaron-Fund-2Q17 Quarterly Report 1superinvestorbulletiNo ratings yet

- Crescat Capital Q3 2017 Quarterly LetterDocument23 pagesCrescat Capital Q3 2017 Quarterly LettersuperinvestorbulletiNo ratings yet

- Sequoia Fund Investor DayDocument28 pagesSequoia Fund Investor DaysuperinvestorbulletiNo ratings yet

- Pershing Square June 2017 LetterDocument33 pagesPershing Square June 2017 Lettersuperinvestorbulleti100% (1)

- WeitzFunds Semi-Annual 93017Document68 pagesWeitzFunds Semi-Annual 93017superinvestorbulletiNo ratings yet

- Hayden Capital Quarterly Letter 2017 Q2Document12 pagesHayden Capital Quarterly Letter 2017 Q2superinvestorbulletiNo ratings yet

- Tencents Wide Moat - Saber CapitalDocument55 pagesTencents Wide Moat - Saber CapitalsuperinvestorbulletiNo ratings yet

- Tilson Goog FBDocument50 pagesTilson Goog FBsuperinvestorbulletiNo ratings yet

- Pzena Commentary 2Q 2017Document3 pagesPzena Commentary 2Q 2017superinvestorbulletiNo ratings yet

- Fairholme Funds 2017 SemiannualDocument49 pagesFairholme Funds 2017 SemiannualsuperinvestorbulletiNo ratings yet

- Greenlight Capital - Full Second Quarter 2017 LetterDocument7 pagesGreenlight Capital - Full Second Quarter 2017 Lettersuperinvestorbulleti100% (2)

- Third Point Q2 2017 Investor Letter TPOIDocument9 pagesThird Point Q2 2017 Investor Letter TPOImarketfolly.comNo ratings yet

- Golden Door Q2 2017 Shareholder LetterDocument3 pagesGolden Door Q2 2017 Shareholder LettersuperinvestorbulletiNo ratings yet

- Auto Dealers - The Bug or The Windshield?Document17 pagesAuto Dealers - The Bug or The Windshield?superinvestorbulletiNo ratings yet

- Fpa Crescent Fund Contrarian Value q1 2017Document40 pagesFpa Crescent Fund Contrarian Value q1 2017superinvestorbulletiNo ratings yet

- 2Q17 Longleaf Partners Quarterly Summary Report All FundsDocument29 pages2Q17 Longleaf Partners Quarterly Summary Report All FundssuperinvestorbulletiNo ratings yet

- Six Impossible Things Before BreakfastDocument15 pagesSix Impossible Things Before BreakfastJesse100% (2)

- Ira Sohn - EBAY Dylan AdelmanDocument23 pagesIra Sohn - EBAY Dylan AdelmansuperinvestorbulletiNo ratings yet

- Two Decades of Winning by Not Losing - Steve RomickDocument16 pagesTwo Decades of Winning by Not Losing - Steve RomicksuperinvestorbulletiNo ratings yet

- Greenhaven Road Capital Q1 2017Document12 pagesGreenhaven Road Capital Q1 2017superinvestorbulletiNo ratings yet

- Adam Blum's 2017 Berkshire Hathaway Annual Meeting Notes May 6 2017Document21 pagesAdam Blum's 2017 Berkshire Hathaway Annual Meeting Notes May 6 2017superinvestorbulletiNo ratings yet

- Current Investment Ideas From Ariel's John RogersDocument3 pagesCurrent Investment Ideas From Ariel's John RogerssuperinvestorbulletiNo ratings yet

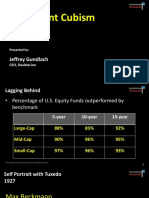

- Gundlach Sohn 2017Document31 pagesGundlach Sohn 2017Zerohedge95% (19)

- Olstein Capital Management - Seeking Solid Businesses Facing StrategicDocument6 pagesOlstein Capital Management - Seeking Solid Businesses Facing StrategicsuperinvestorbulletiNo ratings yet

- MCCM 1Q2017 MarketOutlookDocument89 pagesMCCM 1Q2017 MarketOutlooksuperinvestorbulletiNo ratings yet

- Ackman HHC PresentationDocument50 pagesAckman HHC PresentationZerohedge100% (4)

- Berkshire Hathaway Presentation-Whitney Tilson-Kase Capital-5!4!17Document30 pagesBerkshire Hathaway Presentation-Whitney Tilson-Kase Capital-5!4!17superinvestorbulletiNo ratings yet

- RethinkX ReportDocument77 pagesRethinkX Reportsuperinvestorbulleti100% (4)

- Grey Owl Capital Investor Letter Q1Document6 pagesGrey Owl Capital Investor Letter Q1superinvestorbulletiNo ratings yet

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (890)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Purisima Vs Phil TobaccoDocument4 pagesPurisima Vs Phil TobaccoJohnde Martinez100% (1)

- Topic 2 MCQ Fraud Examination MCQ TestsDocument9 pagesTopic 2 MCQ Fraud Examination MCQ TestswincatsNo ratings yet

- New Water RatesDocument83 pagesNew Water RatesScott FisherNo ratings yet

- Form 1. Application For Travel and Accommodation Assistance - April 2019Document4 pagesForm 1. Application For Travel and Accommodation Assistance - April 2019chris tNo ratings yet

- Saln Gerry MalgapoDocument2 pagesSaln Gerry MalgapogerrymalgapoNo ratings yet

- Eddie BurksDocument11 pagesEddie BurksDave van BladelNo ratings yet

- Counter-Affidavit Denies Charges of Coercion and ThreatsDocument3 pagesCounter-Affidavit Denies Charges of Coercion and ThreatsRio LorraineNo ratings yet

- Money Laundering and Global Financial CrimesDocument178 pagesMoney Laundering and Global Financial CrimesenoshaugustineNo ratings yet

- Ong Yong vs. TiuDocument21 pagesOng Yong vs. TiuZen DanielNo ratings yet

- Kotak Mahindra Bank Limited FY 2020 21Document148 pagesKotak Mahindra Bank Limited FY 2020 21Harshvardhan PatilNo ratings yet

- Nepal p4-6Document3 pagesNepal p4-6Ayushonline442No ratings yet

- Joseph Shine Vs Union of India UOI 27092018 SCSC20182709181534102COM599179Document102 pagesJoseph Shine Vs Union of India UOI 27092018 SCSC20182709181534102COM599179kukoo darlingNo ratings yet

- Rebounding Drills SampleDocument12 pagesRebounding Drills SampleJeff Haefner95% (20)

- Newton's Second Law - RevisitedDocument18 pagesNewton's Second Law - RevisitedRob DicksonNo ratings yet

- Factsheet Alcohol and Risk TakingDocument2 pagesFactsheet Alcohol and Risk TakingDanny EnvisionNo ratings yet

- Nelson Mandela's Leadership and Anti-Apartheid StruggleDocument34 pagesNelson Mandela's Leadership and Anti-Apartheid StruggleAmmara Khalid100% (1)

- Chiavi Quaderno Degli EserciziDocument2 pagesChiavi Quaderno Degli EsercizimoisesNo ratings yet

- A Brief History of Human RightsDocument7 pagesA Brief History of Human RightsBo Dist100% (1)

- View Generated DocsDocument1 pageView Generated DocsNita ShahNo ratings yet

- Fast Cash LoansDocument4 pagesFast Cash LoansFletcher GorisNo ratings yet

- Rosit vs. Davao DoctorsDocument12 pagesRosit vs. Davao DoctorsWilfredNo ratings yet

- Fernandez v. Kalookan Slaughterhouse, Inc., G.R. No. 225075 PDFDocument10 pagesFernandez v. Kalookan Slaughterhouse, Inc., G.R. No. 225075 PDFBrylle Vincent LabuananNo ratings yet

- Rhetorical Analysis Final PaperDocument5 pagesRhetorical Analysis Final Paperapi-534733744No ratings yet

- Khách Ngân Hàng 2Document3 pagesKhách Ngân Hàng 2Phan HươngNo ratings yet

- Padua Vs PeopleDocument1 pagePadua Vs PeopleKlaire EsdenNo ratings yet

- Court Upholds Petitioner's Right to Repurchase LandDocument176 pagesCourt Upholds Petitioner's Right to Repurchase LandLuriza SamaylaNo ratings yet

- Pre SpanishDocument2 pagesPre SpanishStephanie BolanosNo ratings yet

- Pacific Farms V Esguerra (1969)Document3 pagesPacific Farms V Esguerra (1969)Zan BillonesNo ratings yet

- SPPTChap 006Document16 pagesSPPTChap 006iqraNo ratings yet

- 1Document4 pages1sushi100% (1)