You might also like

- Chapter Closing DistancesDocument11 pagesChapter Closing DistanceslambajituNo ratings yet

- Chapter 13 (S.ST classIII)Document4 pagesChapter 13 (S.ST classIII)lambajituNo ratings yet

- STD 3 GK-49-74Document30 pagesSTD 3 GK-49-74lambajituNo ratings yet

- Class3 Ch5 Ch6Document4 pagesClass3 Ch5 Ch6lambajituNo ratings yet

- Steps AICTE DBT PDFDocument2 pagesSteps AICTE DBT PDFMal ObNo ratings yet

- Program Was Issued An Academic Warning Vide Letter No. File No. - , You WereDocument1 pageProgram Was Issued An Academic Warning Vide Letter No. File No. - , You WerelambajituNo ratings yet

- Bank Nifty Data 5 April 2022Document2 pagesBank Nifty Data 5 April 2022lambajituNo ratings yet

- Chapter 1 My BodyDocument14 pagesChapter 1 My BodylambajituNo ratings yet

- CA-3 Ch7and8 NewDocument5 pagesCA-3 Ch7and8 NewYasumati BisenNo ratings yet

- Nifty CallDocument2 pagesNifty CalllambajituNo ratings yet

- IBPS Bank ExamDocument4 pagesIBPS Bank ExamlambajituNo ratings yet

- 61ph III DMRC ModelDocument1 page61ph III DMRC ModelEdwara CutinhoNo ratings yet

- Covering Letter For JobDocument1 pageCovering Letter For JoblambajituNo ratings yet

- Maths Quiz 27 August PDFDocument1 pageMaths Quiz 27 August PDFlambajituNo ratings yet

- Nifty 50 Data 5 April2022Document2 pagesNifty 50 Data 5 April2022lambajituNo ratings yet

- Lan & WanDocument3 pagesLan & WanlambajituNo ratings yet

- Exclusive Breast-Feeding Should Be Practised at Least For 6 Months Breast-Feeding Can Be Continued UptotwoyearsDocument4 pagesExclusive Breast-Feeding Should Be Practised at Least For 6 Months Breast-Feeding Can Be Continued UptotwoyearslambajituNo ratings yet

- DMRC Route Map PDFDocument1 pageDMRC Route Map PDFlambajituNo ratings yet

- Mod15-2 Advanced ExcelDocument20 pagesMod15-2 Advanced ExcellambajituNo ratings yet

- B.E. Sixth Semester Examination, May-2008 Digital System Design (CSE-308-C)Document16 pagesB.E. Sixth Semester Examination, May-2008 Digital System Design (CSE-308-C)lambajituNo ratings yet

- Digital System Design: Sixth Semester Examination, May-2009 (CSE-308-QDocument14 pagesDigital System Design: Sixth Semester Examination, May-2009 (CSE-308-QlambajituNo ratings yet

- LatexDocument35 pagesLatexapi-3720088No ratings yet

- DSD Latest Question PaperDocument12 pagesDSD Latest Question PaperlambajituNo ratings yet

- B.E. Digital System Design (EE-310-E) : Sixth Semester Examination, Dec-2009Document15 pagesB.E. Digital System Design (EE-310-E) : Sixth Semester Examination, Dec-2009lambajituNo ratings yet

- 18 Programmable LogicDocument30 pages18 Programmable LogiclambajituNo ratings yet

- FPGA Historical Perspective, Architectures, Programming TechnologiesDocument44 pagesFPGA Historical Perspective, Architectures, Programming TechnologiesILikeScribd5050No ratings yet

- Industrial Training Report Submission Guidelines For Engineering StudentsDocument6 pagesIndustrial Training Report Submission Guidelines For Engineering StudentsSuprateek GuliaNo ratings yet

- Eecs150 - Digital Design: Lecture 6 - Field Programmable Gate Arrays (Fpgas)Document25 pagesEecs150 - Digital Design: Lecture 6 - Field Programmable Gate Arrays (Fpgas)lambajituNo ratings yet

- Digital System Design Using VHDL PaperDocument2 pagesDigital System Design Using VHDL PaperlambajituNo ratings yet

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5782)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (890)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (72)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Okhiria Wisdom Ozeigbe: Customer StatementDocument2 pagesOkhiria Wisdom Ozeigbe: Customer StatementGreat WhizdomNo ratings yet

- Taxation Dissertation SampleDocument36 pagesTaxation Dissertation SampleOnline Dissertation WritingNo ratings yet

- Transfer TaxDocument6 pagesTransfer TaxMark Rainer Yongis LozaresNo ratings yet

- III.5. Fortune Tobacco GR 180006 28 Sept 2011 - CDDocument3 pagesIII.5. Fortune Tobacco GR 180006 28 Sept 2011 - CDNelly HerreraNo ratings yet

- Citcha For Brgy. CertificationDocument3 pagesCitcha For Brgy. CertificationJamaica Uljer RubioNo ratings yet

- mnl1994681085 - STD AivfDocument4 pagesmnl1994681085 - STD AivfChristian Daniel AlmiranezNo ratings yet

- Krishnaveni Talent School: Ao Visiting ReportDocument4 pagesKrishnaveni Talent School: Ao Visiting ReportgopisrinivasNo ratings yet

- GST Returns NotesDocument5 pagesGST Returns NotesvishnureachmeNo ratings yet

- مصرف الانماء - 210625 - 100246 - 210627 - 120329Document1 pageمصرف الانماء - 210625 - 100246 - 210627 - 120329Nadia QusaiNo ratings yet

- BarksDocument45 pagesBarksKaye Alyssa EnriquezNo ratings yet

- Philippine Legal Guide - Tax Case Digest - CIR v. Isabela Cultural Corp. (2007)Document3 pagesPhilippine Legal Guide - Tax Case Digest - CIR v. Isabela Cultural Corp. (2007)Fymgem AlbertoNo ratings yet

- MASTERY TAXATION October-2019 PDFDocument12 pagesMASTERY TAXATION October-2019 PDFJuvelyn Gregorio100% (1)

- Fast Services Payroll SlipDocument1 pageFast Services Payroll SlipLeidegay AnicoyNo ratings yet

- 2019 Chicago TIF SummaryDocument7 pages2019 Chicago TIF SummaryCrainsChicagoBusinessNo ratings yet

- Ingles IIDocument6 pagesIngles IIReport JunglaNo ratings yet

- SBLCDocument2 pagesSBLCwillian cortez100% (1)

- February 2023 payslip for Anurag JainDocument1 pageFebruary 2023 payslip for Anurag Jainmatrix finserve0% (1)

- Kashato Practice Set - 2020-10thedDocument84 pagesKashato Practice Set - 2020-10thedMary Jhiezael Pascual83% (12)

- Amulya Kumar Verma 26asDocument4 pagesAmulya Kumar Verma 26asSatyendra SinghNo ratings yet

- Entity ComparisonDocument3 pagesEntity Comparisoncthunder_1No ratings yet

- Problem 1 - Dallas CorporationDocument6 pagesProblem 1 - Dallas CorporationKatherine Cabading InocandoNo ratings yet

- 502647F 2018Document2 pages502647F 2018Tilak RajNo ratings yet

- ASTPL - BCSS-T Course Registration FormDocument1 pageASTPL - BCSS-T Course Registration Formtengku amirNo ratings yet

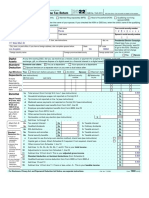

- f1040 PDFDocument2 pagesf1040 PDFCHRISTIAN RODRIGUEZNo ratings yet

- Ride Details Bill Details: Thanks For Travelling With Us, Ravi KushDocument3 pagesRide Details Bill Details: Thanks For Travelling With Us, Ravi KushEr Ravi KushNo ratings yet

- Income From SalariesDocument24 pagesIncome From SalariesvnbanjanNo ratings yet

- TRAIN Law Overview and OutlookDocument4 pagesTRAIN Law Overview and OutlookAdam Ross Toledo BrionesNo ratings yet

- REVOKING REVENUE REGULATIONS REINSTATING PRIOR PROVISIONSDocument2 pagesREVOKING REVENUE REGULATIONS REINSTATING PRIOR PROVISIONSAndrew Benedict PardilloNo ratings yet

- How To Log in To Your FRS Online AccountDocument4 pagesHow To Log in To Your FRS Online AccountSharan FosbinderNo ratings yet

- Account Statement From 9 Jan 2020 To 9 Jul 2020: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument10 pagesAccount Statement From 9 Jan 2020 To 9 Jul 2020: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceAnil Kumar RoutNo ratings yet