You might also like

- Anatomy of the 2007-2009 Financial Crisis and Credit Risk TransferDocument16 pagesAnatomy of the 2007-2009 Financial Crisis and Credit Risk TransferBelle AnnaNo ratings yet

- The Great Recession: The burst of the property bubble and the excesses of speculationFrom EverandThe Great Recession: The burst of the property bubble and the excesses of speculationNo ratings yet

- Real Estate CDO and CDS LectureDocument25 pagesReal Estate CDO and CDS Lecturefunkchunk33No ratings yet

- FinTech Rising: Navigating the maze of US & EU regulationsFrom EverandFinTech Rising: Navigating the maze of US & EU regulationsRating: 5 out of 5 stars5/5 (1)

- Financial Crisis 2007-09Document9 pagesFinancial Crisis 2007-09RikardasNo ratings yet

- Learnings from Financial DisastersDocument33 pagesLearnings from Financial DisastersChip choiNo ratings yet

- MIT14 02S14 Finanic CrisisDocument19 pagesMIT14 02S14 Finanic CrisisShirat MohsinNo ratings yet

- International Finance FinalDocument27 pagesInternational Finance FinalRishabh RaiNo ratings yet

- CLO PrimerDocument31 pagesCLO PrimerdgnyNo ratings yet

- HSBC's Mortgage Lending DecisionDocument22 pagesHSBC's Mortgage Lending Decisionbestchi19No ratings yet

- RE Capital Markets 6.9 330pDocument82 pagesRE Capital Markets 6.9 330pAirollNo ratings yet

- Aglietta (2008)Document4 pagesAglietta (2008)Lucas BalestraNo ratings yet

- Global Economic OutlookDocument23 pagesGlobal Economic OutlookRAMESHBABUNo ratings yet

- Macro 5Document72 pagesMacro 5ChangeBunnyNo ratings yet

- Fortis Bank Maritime FinanceDocument43 pagesFortis Bank Maritime FinancebluepperNo ratings yet

- Liquidity Crunch 2007 08 SlidesDocument32 pagesLiquidity Crunch 2007 08 SlidesKuvan AkrehNo ratings yet

- 2023-10-28 Sub Prime Mortgage Crisis V0.02amDocument13 pages2023-10-28 Sub Prime Mortgage Crisis V0.02amb23036No ratings yet

- Financial Crisis: in The United StatesDocument48 pagesFinancial Crisis: in The United StatesPhuongAnh NguyenNo ratings yet

- Summary Chapter 8Document6 pagesSummary Chapter 8Zahidul AlamNo ratings yet

- Subprime Mortgage Crisis 2008Document37 pagesSubprime Mortgage Crisis 2008Robin Thieu100% (16)

- Instructor: Bernard Malamud: - Office: BEH 502Document36 pagesInstructor: Bernard Malamud: - Office: BEH 502kinaNo ratings yet

- SVB Crisis and ImpactDocument1 pageSVB Crisis and Impactharshad jainNo ratings yet

- 3 - The Investment Environment (Part II)Document16 pages3 - The Investment Environment (Part II)Salvador FigueroaNo ratings yet

- Liquidity Risk: Aries H. Prasetyo, SE, MM, PH.D, RFP-I, CERDocument47 pagesLiquidity Risk: Aries H. Prasetyo, SE, MM, PH.D, RFP-I, CERDonny Ramanto100% (1)

- Dev Strischek SVP Credit Policy Officer SunTrust BankDocument46 pagesDev Strischek SVP Credit Policy Officer SunTrust Bankprash.rajuNo ratings yet

- A Tale of Two Hedge FundsDocument17 pagesA Tale of Two Hedge FundsS Sarkar100% (1)

- Why Do Financial Crises OccurDocument21 pagesWhy Do Financial Crises OccurАндријана Б. ДаневскаNo ratings yet

- Who's Holding The Bag?Document64 pagesWho's Holding The Bag?char1eylu100% (4)

- LEH 20071023 TopicsInABCPConduitsDocument24 pagesLEH 20071023 TopicsInABCPConduitsNuggets MusicNo ratings yet

- Chapter 4 - ABSDocument22 pagesChapter 4 - ABSRiha MachireddyNo ratings yet

- Cdos: Mortgage Fruit Gone Bad What Is A Cdo?Document7 pagesCdos: Mortgage Fruit Gone Bad What Is A Cdo?Thought LeadersNo ratings yet

- Japanese Banking CrisisDocument36 pagesJapanese Banking CrisisAmol BagulNo ratings yet

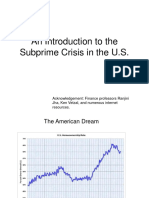

- An Introduction To The Subprime Crisis in The U.SDocument25 pagesAn Introduction To The Subprime Crisis in The U.SAdeel RanaNo ratings yet

- Securitization of Mortgages Voctober2019Document64 pagesSecuritization of Mortgages Voctober2019Hins LeeNo ratings yet

- AnalytixWise - Risk Analytics Unit 3 Credit Risk AnalyticsDocument29 pagesAnalytixWise - Risk Analytics Unit 3 Credit Risk AnalyticsUrvashi Singh100% (1)

- Liquidity Management by Islamic BanksDocument9 pagesLiquidity Management by Islamic BanksMiran shah chowdhury100% (3)

- Fin 4150 Week 9 LecturesDocument40 pagesFin 4150 Week 9 LecturesEric McLaughlinNo ratings yet

- GFC2007Document15 pagesGFC2007Nur Hidayah JalilNo ratings yet

- Credit Crunch What Went WrongDocument32 pagesCredit Crunch What Went WrongGautam ChapagainNo ratings yet

- Macroeconomic (Saving and Investment)Document110 pagesMacroeconomic (Saving and Investment)Sheillie KirklandNo ratings yet

- SVB Crisis - O3 SecuritiesDocument7 pagesSVB Crisis - O3 SecuritiesAnkit PandeNo ratings yet

- Bankers New Clothes - Slides PrintDocument18 pagesBankers New Clothes - Slides PrintShyamal VermaNo ratings yet

- FN323 - Debt Capital MarketDocument10 pagesFN323 - Debt Capital MarketNapat InseeyongNo ratings yet

- The Subprime Mortgage Crisis and Credit Default SwapsDocument22 pagesThe Subprime Mortgage Crisis and Credit Default SwapsAnirban DubeyNo ratings yet

- Sub-Prime Loans ExplainedDocument16 pagesSub-Prime Loans ExplainedDavneet KaurNo ratings yet

- SecuritizationDocument34 pagesSecuritizationsanil mehtaNo ratings yet

- CMBS 101: Commercial Mortgage-Backed Securities TrainingDocument30 pagesCMBS 101: Commercial Mortgage-Backed Securities Trainingsvati jindalNo ratings yet

- Factors Causing Financial CrisesDocument16 pagesFactors Causing Financial CrisesfizaAhaiderNo ratings yet

- Broker Presentation - Website 2021Document25 pagesBroker Presentation - Website 2021Eugene HaNo ratings yet

- Dbrs Rmbs Criteria 2004-12Document12 pagesDbrs Rmbs Criteria 2004-12janisnagobadsNo ratings yet

- Assignment Subprime MortgageDocument6 pagesAssignment Subprime MortgagemypinkladyNo ratings yet

- RAMID Souhail Final Exam Case StudyDocument38 pagesRAMID Souhail Final Exam Case Studyjean.jacquesNo ratings yet

- Chapter 9Document33 pagesChapter 9Faris IkhwanNo ratings yet

- Pershing Sq. Pres On Housing 11-3-10Document48 pagesPershing Sq. Pres On Housing 11-3-10the_knowledge_pileNo ratings yet

- Capital StructureDocument62 pagesCapital Structuregio040700No ratings yet

- Chapter-4: Sources and Uses of Funds, Performance Evaluation and Bank FailureDocument16 pagesChapter-4: Sources and Uses of Funds, Performance Evaluation and Bank FailureEEL KfWBMZ2.1No ratings yet

- Factors That Influence Credit Yield SpreadsDocument20 pagesFactors That Influence Credit Yield SpreadsTaanNo ratings yet

- Project Finance: Campbell R. Harvey Aditya Agarwal Sandeep KaulDocument99 pagesProject Finance: Campbell R. Harvey Aditya Agarwal Sandeep KaulSudhir WaghuleNo ratings yet

- Microsoft Office 2007: Excel Chapter 1Document66 pagesMicrosoft Office 2007: Excel Chapter 1a4agarwalNo ratings yet

- Bexar Audubon SocietyDocument4 pagesBexar Audubon Societyapi-20792794No ratings yet

- E-Mail Subject: School Kit 2010' Initiative: Enabling Lesser Fortunate To Acquire Their Fundamental Right To EducationDocument1 pageE-Mail Subject: School Kit 2010' Initiative: Enabling Lesser Fortunate To Acquire Their Fundamental Right To Educationa4agarwalNo ratings yet

- Proverbs 7 Proverbs 8 Proverbs 9 Romans 9: ScriptureDocument2 pagesProverbs 7 Proverbs 8 Proverbs 9 Romans 9: Scripturea4agarwalNo ratings yet

- NullDocument7 pagesNullapi-29068912No ratings yet

- BC Bike Race 2010: Mandatory Gear: The List - Per Person (The Safetysixpack)Document1 pageBC Bike Race 2010: Mandatory Gear: The List - Per Person (The Safetysixpack)a4agarwalNo ratings yet

- NullDocument8 pagesNulla4agarwalNo ratings yet

- Bexar Audubon SocietyDocument8 pagesBexar Audubon Societyapi-20792794No ratings yet

- Bexar Audubon SocietyDocument4 pagesBexar Audubon Societyapi-20792794No ratings yet

- School Kit 2010: "Nine Tenths of Education Is Encouragement"Document15 pagesSchool Kit 2010: "Nine Tenths of Education Is Encouragement"api-26579472No ratings yet

- NullDocument8 pagesNulla4agarwalNo ratings yet

- School Kit 2010: "Nine Tenths of Education Is Encouragement"Document15 pagesSchool Kit 2010: "Nine Tenths of Education Is Encouragement"api-26579472No ratings yet

- Sociolinguistics: Tuesday 6/8Document8 pagesSociolinguistics: Tuesday 6/8a4agarwalNo ratings yet

- Friends of The Greenbelt Foundation: Communications Assistant (Intern)Document2 pagesFriends of The Greenbelt Foundation: Communications Assistant (Intern)a4agarwalNo ratings yet

- NOAA WebsiteDocument4 pagesNOAA Websitea4agarwalNo ratings yet

- MondayDocument2 pagesMondaya4agarwalNo ratings yet

- Cialis Female ViagraDocument1 pageCialis Female Viagraa4agarwalNo ratings yet

- SociolinguisticsDocument8 pagesSociolinguisticsa4agarwalNo ratings yet

- Character Archetypes: The BullyDocument13 pagesCharacter Archetypes: The Bullya4agarwalNo ratings yet

- NullDocument7 pagesNulla4agarwalNo ratings yet

- NullDocument2 pagesNulla4agarwalNo ratings yet

- NullDocument1 pageNulla4agarwalNo ratings yet

- People and Place ... Pgs 2 & 4 Community Issues ... Pgs 3 & 5Document6 pagesPeople and Place ... Pgs 2 & 4 Community Issues ... Pgs 3 & 5a4agarwalNo ratings yet

- Northeast Middle School AthleticsDocument1 pageNortheast Middle School Athleticsa4agarwalNo ratings yet

- NullDocument44 pagesNulla4agarwalNo ratings yet

- Teach Baton Rouge Observation Form: Practitioner Teacher: Teacher Advisor: DateDocument2 pagesTeach Baton Rouge Observation Form: Practitioner Teacher: Teacher Advisor: Datea4agarwalNo ratings yet

- NullDocument2 pagesNulla4agarwalNo ratings yet

- "The Gabriel": LansdaleDocument5 pages"The Gabriel": Lansdalea4agarwalNo ratings yet

- Banking EnglishDocument23 pagesBanking Englisha4agarwalNo ratings yet

- IDD Competencies CMC CompetenciesDocument1 pageIDD Competencies CMC Competenciesa4agarwalNo ratings yet

- Commodities Reading List ScheduleDocument5 pagesCommodities Reading List Schedulelaozi222No ratings yet

- Project Report on Portfolio Management, Live Trading, Equity Research & Derivatives at Aditya Birla Sun Life InsuranceDocument60 pagesProject Report on Portfolio Management, Live Trading, Equity Research & Derivatives at Aditya Birla Sun Life InsuranceDarshan ShahNo ratings yet

- Unit 4: Investment VehiclesDocument29 pagesUnit 4: Investment Vehiclesworld4meNo ratings yet

- Forex Incontrol User ManualDocument3 pagesForex Incontrol User ManualAlexandre VassolerNo ratings yet

- Managing A Portfolio: Closed-End Funds Exchange Traded FundsDocument4 pagesManaging A Portfolio: Closed-End Funds Exchange Traded FundsDivya Singh RathoreNo ratings yet

- Account Number Currency Int Amt CR Int Amt DR: End of ReportDocument2 pagesAccount Number Currency Int Amt CR Int Amt DR: End of ReportshivaprasadssNo ratings yet

- Iecmd - Jan 2020Document79 pagesIecmd - Jan 2020Steven Wang100% (1)

- McRae Mark SureFire Forex Trading PDFDocument113 pagesMcRae Mark SureFire Forex Trading PDFjoshijaysoft100% (1)

- Thrift Operations: Financial Markets and Institutions, 7e, Jeff MaduraDocument30 pagesThrift Operations: Financial Markets and Institutions, 7e, Jeff MaduraKevin NicoNo ratings yet

- Balance Sheet VW Ar18Document1 pageBalance Sheet VW Ar18Sneha SinghNo ratings yet

- How to Become a Stock Market Genius by Investing in Underfollowed SituationsDocument2 pagesHow to Become a Stock Market Genius by Investing in Underfollowed SituationsRyan ReitzNo ratings yet

- MJ 2021Document11 pagesMJ 2021Yusuf MohamedNo ratings yet

- DR A.P.J. Abdul Kalam Technical University Lucknow: Uttam Group of InstitutionsDocument33 pagesDR A.P.J. Abdul Kalam Technical University Lucknow: Uttam Group of InstitutionsMayank jainNo ratings yet

- The Asian Crisis and Investor Behavior in Thailand'S Equity MarketDocument23 pagesThe Asian Crisis and Investor Behavior in Thailand'S Equity MarketAleis RiquelmeNo ratings yet

- Mishkin 6ce TB Ch27Document8 pagesMishkin 6ce TB Ch27JaeDukAndrewSeoNo ratings yet

- Trading Support and Resistance Levels V 3 PDF 20240112 185657 0000Document14 pagesTrading Support and Resistance Levels V 3 PDF 20240112 185657 0000akxi2468No ratings yet

- Merchant Banking - A Comparative Analysis of Private and Government SectorDocument7 pagesMerchant Banking - A Comparative Analysis of Private and Government SectorHarsh KbddhsjNo ratings yet

- Revenue (Sales) XXX (-) Variable Costs XXXDocument10 pagesRevenue (Sales) XXX (-) Variable Costs XXXNageshwar SinghNo ratings yet

- Price of MoneyDocument32 pagesPrice of MoneyneffjasoNo ratings yet

- Sandy Lai HKU PaperDocument49 pagesSandy Lai HKU PaperAnish S.MenonNo ratings yet

- Assignment#04Document10 pagesAssignment#04irfanhaidersewagNo ratings yet

- E-Commerce 2015 11th Edition Laudon Solutions Manual 1Document36 pagesE-Commerce 2015 11th Edition Laudon Solutions Manual 1joshuamooreqicoykmtan100% (21)

- Reliance Securities account authorizationDocument2 pagesReliance Securities account authorizationManojNo ratings yet

- Instructional Module FABMN2 12 Lesson No. 6Document2 pagesInstructional Module FABMN2 12 Lesson No. 6Daneya Enrica JoseNo ratings yet

- Essential 1Document13 pagesEssential 1chandoraNo ratings yet

- Useful Notes For Bank XamDocument40 pagesUseful Notes For Bank XamVersha ManakpuriNo ratings yet

- 18ardennes RulesDocument20 pages18ardennes RulestobymaoNo ratings yet

- Article CapitalallocationDocument85 pagesArticle CapitalallocationBruno SchembriNo ratings yet

- Yearbook 2009Document274 pagesYearbook 2009mkasi2k9No ratings yet

- Chapter 8Document29 pagesChapter 8jgau0017No ratings yet

- University of Berkshire Hathaway: 30 Years of Lessons Learned from Warren Buffett & Charlie Munger at the Annual Shareholders MeetingFrom EverandUniversity of Berkshire Hathaway: 30 Years of Lessons Learned from Warren Buffett & Charlie Munger at the Annual Shareholders MeetingRating: 4.5 out of 5 stars4.5/5 (97)

- These are the Plunderers: How Private Equity Runs—and Wrecks—AmericaFrom EverandThese are the Plunderers: How Private Equity Runs—and Wrecks—AmericaRating: 4.5 out of 5 stars4.5/5 (14)

- Financial Intelligence: A Manager's Guide to Knowing What the Numbers Really MeanFrom EverandFinancial Intelligence: A Manager's Guide to Knowing What the Numbers Really MeanRating: 4.5 out of 5 stars4.5/5 (79)

- Disloyal: A Memoir: The True Story of the Former Personal Attorney to President Donald J. TrumpFrom EverandDisloyal: A Memoir: The True Story of the Former Personal Attorney to President Donald J. TrumpRating: 4 out of 5 stars4/5 (214)

- Value: The Four Cornerstones of Corporate FinanceFrom EverandValue: The Four Cornerstones of Corporate FinanceRating: 4.5 out of 5 stars4.5/5 (18)

- Introduction to Negotiable Instruments: As per Indian LawsFrom EverandIntroduction to Negotiable Instruments: As per Indian LawsRating: 5 out of 5 stars5/5 (1)

- Mastering Private Equity: Transformation via Venture Capital, Minority Investments and BuyoutsFrom EverandMastering Private Equity: Transformation via Venture Capital, Minority Investments and BuyoutsNo ratings yet

- Venture Deals, 4th Edition: Be Smarter than Your Lawyer and Venture CapitalistFrom EverandVenture Deals, 4th Edition: Be Smarter than Your Lawyer and Venture CapitalistRating: 4.5 out of 5 stars4.5/5 (73)

- Getting Through: Cold Calling Techniques To Get Your Foot In The DoorFrom EverandGetting Through: Cold Calling Techniques To Get Your Foot In The DoorRating: 4.5 out of 5 stars4.5/5 (63)

- Financial Modeling and Valuation: A Practical Guide to Investment Banking and Private EquityFrom EverandFinancial Modeling and Valuation: A Practical Guide to Investment Banking and Private EquityRating: 4.5 out of 5 stars4.5/5 (4)

- Add Then Multiply: How small businesses can think like big businesses and achieve exponential growthFrom EverandAdd Then Multiply: How small businesses can think like big businesses and achieve exponential growthNo ratings yet

- Summary of The Black Swan: by Nassim Nicholas Taleb | Includes AnalysisFrom EverandSummary of The Black Swan: by Nassim Nicholas Taleb | Includes AnalysisRating: 5 out of 5 stars5/5 (6)

- Burn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialFrom EverandBurn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialNo ratings yet

- Angel: How to Invest in Technology Startups-Timeless Advice from an Angel Investor Who Turned $100,000 into $100,000,000From EverandAngel: How to Invest in Technology Startups-Timeless Advice from an Angel Investor Who Turned $100,000 into $100,000,000Rating: 4.5 out of 5 stars4.5/5 (86)

- Finance Basics (HBR 20-Minute Manager Series)From EverandFinance Basics (HBR 20-Minute Manager Series)Rating: 4.5 out of 5 stars4.5/5 (32)

- Buffettology: The Previously Unexplained Techniques That Have Made Warren Buffett American's Most Famous InvestorFrom EverandBuffettology: The Previously Unexplained Techniques That Have Made Warren Buffett American's Most Famous InvestorRating: 4.5 out of 5 stars4.5/5 (132)

- Startup CEO: A Field Guide to Scaling Up Your Business (Techstars)From EverandStartup CEO: A Field Guide to Scaling Up Your Business (Techstars)Rating: 4.5 out of 5 stars4.5/5 (4)

- Burn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialFrom EverandBurn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialRating: 4.5 out of 5 stars4.5/5 (32)

- The Masters of Private Equity and Venture Capital: Management Lessons from the Pioneers of Private InvestingFrom EverandThe Masters of Private Equity and Venture Capital: Management Lessons from the Pioneers of Private InvestingRating: 4.5 out of 5 stars4.5/5 (17)

- Joy of Agility: How to Solve Problems and Succeed SoonerFrom EverandJoy of Agility: How to Solve Problems and Succeed SoonerRating: 4 out of 5 stars4/5 (1)

- Warren Buffett Book of Investing Wisdom: 350 Quotes from the World's Most Successful InvestorFrom EverandWarren Buffett Book of Investing Wisdom: 350 Quotes from the World's Most Successful InvestorNo ratings yet

- The Complete Book of Wills, Estates & Trusts (4th Edition): Advice That Can Save You Thousands of Dollars in Legal Fees and TaxesFrom EverandThe Complete Book of Wills, Estates & Trusts (4th Edition): Advice That Can Save You Thousands of Dollars in Legal Fees and TaxesRating: 4 out of 5 stars4/5 (1)

- The Business Legal Lifecycle US Edition: How To Successfully Navigate Your Way From Start Up To SuccessFrom EverandThe Business Legal Lifecycle US Edition: How To Successfully Navigate Your Way From Start Up To SuccessNo ratings yet