You might also like

- Chapters 1 & 2 Government and Corporate Social Responsibility (GCSR)Document20 pagesChapters 1 & 2 Government and Corporate Social Responsibility (GCSR)Armie RicoNo ratings yet

- Models and Frameworks of Social Responsibility of BusinessDocument8 pagesModels and Frameworks of Social Responsibility of Businesshoxhii100% (2)

- Week 3 - Code of Ethics in BusinessDocument6 pagesWeek 3 - Code of Ethics in BusinessSeverus S Potter100% (3)

- Models & Frameworks of Social Responsibility in TheDocument3 pagesModels & Frameworks of Social Responsibility in TheSheila Mae Malesido63% (8)

- 2 Core Principles of Fairness Accountability and TransparencyDocument28 pages2 Core Principles of Fairness Accountability and Transparencyrommel legaspi67% (3)

- Lesson 10:: History and Perspectives On Corporate Social ResponsibilityDocument33 pagesLesson 10:: History and Perspectives On Corporate Social ResponsibilityAnonymous 5npGhmNo ratings yet

- Responsibilities and Accountabilities of EntrepreneursDocument1 pageResponsibilities and Accountabilities of EntrepreneursCatherine Rivera80% (10)

- Carroll CSR PyramidDocument3 pagesCarroll CSR PyramidVersoza NelNo ratings yet

- 01.1 - 1.3 - Introduction and Differentiate The Forms of Business OrganizatiDocument38 pages01.1 - 1.3 - Introduction and Differentiate The Forms of Business OrganizatiChristian Carator MagbanuaNo ratings yet

- Different Models and Frameworks of Social ResponsibilityDocument18 pagesDifferent Models and Frameworks of Social ResponsibilityJomar Benedico100% (1)

- BUSINESS ETHICS LAS q3-q4Document22 pagesBUSINESS ETHICS LAS q3-q4Graciously Elle100% (1)

- Business Ethics ModuleDocument7 pagesBusiness Ethics ModuleRica Canaba100% (2)

- Government and Corporate Social Responsibility (GCSR) Chapter 1: Strategic Public Policy Vision for CSRDocument4 pagesGovernment and Corporate Social Responsibility (GCSR) Chapter 1: Strategic Public Policy Vision for CSRLouelie Jean AlfornonNo ratings yet

- Business Ethics and Social R EsponsibilityDocument29 pagesBusiness Ethics and Social R EsponsibilityCharlene Dana100% (1)

- Chapter 2 Foundations of The Business EthicsDocument7 pagesChapter 2 Foundations of The Business EthicsCyrelOcfemia100% (5)

- HBM 122 Lesson 4 Code of Ethics and Business ConductDocument18 pagesHBM 122 Lesson 4 Code of Ethics and Business ConductKrisshaNo ratings yet

- Common Practices in Business OrganizationDocument24 pagesCommon Practices in Business Organizationromeo magcalas75% (4)

- Business Ethics Module 1Document3 pagesBusiness Ethics Module 1Spencer Asuncion Ü100% (2)

- Social Responsibility of EntrepreneursDocument39 pagesSocial Responsibility of EntrepreneursArrabella De Mesa100% (2)

- Impact of Belief Systems on Business PracticesDocument14 pagesImpact of Belief Systems on Business Practicessarah fojasNo ratings yet

- 5 The Concept of Corporate Social ResponsibilityDocument15 pages5 The Concept of Corporate Social Responsibilityrommel legaspiNo ratings yet

- 3 Classical Ethical Philosophies An IntroductionDocument16 pages3 Classical Ethical Philosophies An Introductionrommel legaspi75% (4)

- Corporate Social ResponsibilityDocument4 pagesCorporate Social ResponsibilityCnette S. Lumbo100% (3)

- Optimize Business Operations with Transparency, Fairness and AccountabilityDocument33 pagesOptimize Business Operations with Transparency, Fairness and AccountabilityAllan Angeles Orbita70% (10)

- Week 10 - Models of Corporate Social ResponsibilityDocument10 pagesWeek 10 - Models of Corporate Social ResponsibilityZybel RosalesNo ratings yet

- Lesson1 Nature and Forms of Business OrganizationsDocument15 pagesLesson1 Nature and Forms of Business OrganizationsMarykay Bermeo100% (1)

- Business Ethics and Social Responsibilty (TM) PDFDocument48 pagesBusiness Ethics and Social Responsibilty (TM) PDFEri Echalar92% (13)

- Business Ethics - Module 8 - 4th QuarterDocument8 pagesBusiness Ethics - Module 8 - 4th QuarterACCOUNTING MANAGEMENT100% (2)

- Module 3Document4 pagesModule 3Kelvin Jay Sebastian Sapla100% (2)

- Business Ethics - Module 9Document10 pagesBusiness Ethics - Module 9ACCOUNTING MANAGEMENT80% (5)

- Business Ethics in Philippine PerspectiveDocument18 pagesBusiness Ethics in Philippine PerspectiveGG50% (2)

- Basic Premises and Specific Relevance of Corporate Social ResponsibilityDocument2 pagesBasic Premises and Specific Relevance of Corporate Social ResponsibilitySheila Mae Guerta Lacerona71% (7)

- Lesson 3: Classical Philosophies and The Evolution of Business EthicsDocument16 pagesLesson 3: Classical Philosophies and The Evolution of Business Ethicsshin50% (4)

- Business Forms ExplainedDocument39 pagesBusiness Forms ExplainedPrances Pelobello50% (2)

- BUS ETHICS Module 3 PhilosophiesDocument8 pagesBUS ETHICS Module 3 PhilosophiesKJ JonesNo ratings yet

- Business Ethics and Social Responsibility: Quarter 4 - Module 2: Ethical Issues in EntrepreneurshipDocument20 pagesBusiness Ethics and Social Responsibility: Quarter 4 - Module 2: Ethical Issues in EntrepreneurshipJenieffer Pescador86% (7)

- Ethics Has No Place in BusinessDocument5 pagesEthics Has No Place in BusinessYahleeni Meena Raja Deran100% (3)

- The Impact of Belief Systems in The Business SettingsDocument24 pagesThe Impact of Belief Systems in The Business SettingsAndrei Barela50% (2)

- Religious Roots Of Business EthicsDocument10 pagesReligious Roots Of Business EthicsPrabhu Presanna60% (5)

- The Nature and Forms of Business OrganizationsDocument18 pagesThe Nature and Forms of Business OrganizationsAllan Angeles Orbita100% (1)

- Corporate Social Responsibility CSRDocument41 pagesCorporate Social Responsibility CSRSatyajeet Pawar86% (43)

- Business Ethics Module 4Document9 pagesBusiness Ethics Module 4Kanton FernandezNo ratings yet

- Business Ethics and Social Responsibility (1 Quarter: Week 5)Document6 pagesBusiness Ethics and Social Responsibility (1 Quarter: Week 5)marissa casareno almueteNo ratings yet

- Corporate Social ResponsibilityDocument4 pagesCorporate Social ResponsibilityNelsonMoseMNo ratings yet

- Impact of Belief Systems in Business PracticesDocument21 pagesImpact of Belief Systems in Business PracticesSteven SiloNo ratings yet

- Business Ethics and Social Responsibility-SHS: Learning CompetencyDocument14 pagesBusiness Ethics and Social Responsibility-SHS: Learning CompetencyMizza Moreno Cantila67% (6)

- CSR Reference Framework ExplainedDocument1 pageCSR Reference Framework ExplainedNicole MaglalangNo ratings yet

- ABM - Business Ethics and Social Responsibility CG PDFDocument5 pagesABM - Business Ethics and Social Responsibility CG PDFJanella96% (25)

- Ethics and Corporate Social ResponsibilityDocument66 pagesEthics and Corporate Social ResponsibilityKillua Zoldyck100% (1)

- Business Ethics and Social ResponsibilityDocument5 pagesBusiness Ethics and Social Responsibilitystanleywong100% (10)

- The Corporate Social Responsibility: Lesson 9Document9 pagesThe Corporate Social Responsibility: Lesson 9KrisshaNo ratings yet

- Social Responsibility of EntrepreneursDocument13 pagesSocial Responsibility of EntrepreneursJoseph Opao Jr.0% (1)

- Classical Philosophies' Business ImplicationsDocument4 pagesClassical Philosophies' Business ImplicationsLee Arne Barayuga33% (3)

- 01.4.5 Common Practices in Business OrganizationsDocument30 pages01.4.5 Common Practices in Business OrganizationsChristian Carator Magbanua100% (5)

- Lesson 6: Major Ethical PhilosophersDocument25 pagesLesson 6: Major Ethical PhilosophersKrisshaNo ratings yet

- Bus Ethics - Module 7 - Major Ethical Issues in The Corporate WorldDocument6 pagesBus Ethics - Module 7 - Major Ethical Issues in The Corporate WorldKJ JonesNo ratings yet

- 07 - Dima Jamali - 2011, Stakeholder TheoryDocument20 pages07 - Dima Jamali - 2011, Stakeholder TheoryannisanalaNo ratings yet

- Handouts in CSRDocument3 pagesHandouts in CSRLucero Dela Cuesta TrangiaNo ratings yet

- Reading Material in Ethics Week 4 FinalsDocument5 pagesReading Material in Ethics Week 4 FinalsGeorge Lubiano PastorNo ratings yet

- Should Modern Businesses Engage in CSRDocument3 pagesShould Modern Businesses Engage in CSRSofia TabauNo ratings yet

- Partnership Operations: Accounting Cycle of A PartnershipDocument13 pagesPartnership Operations: Accounting Cycle of A Partnershipred100% (1)

- RiskmgmteventsDocument2 pagesRiskmgmteventsredNo ratings yet

- SWOT Analysis RecommendationsDocument1 pageSWOT Analysis RecommendationsredNo ratings yet

- National Income DeterminationDocument23 pagesNational Income DeterminationredNo ratings yet

- SGV Cup Level 2Document6 pagesSGV Cup Level 2Nicolette DonovanNo ratings yet

- General and Application ControlsDocument12 pagesGeneral and Application ControlsredNo ratings yet

- Risk Exposures and The Internal Control StructureDocument20 pagesRisk Exposures and The Internal Control StructureredNo ratings yet

- Phoenix Petroleum Philippines, IncDocument1 pagePhoenix Petroleum Philippines, IncredNo ratings yet

- Computer-Based Transaction Processing: Off-Line Data EntryDocument9 pagesComputer-Based Transaction Processing: Off-Line Data EntryredNo ratings yet

- Managing Security of Information SystemsDocument4 pagesManaging Security of Information SystemsredNo ratings yet

- Aggregate Planning Strategies: Aggregate Planning Is The Process of Developing, Analyzing, and Maintaining A PreliminaryDocument6 pagesAggregate Planning Strategies: Aggregate Planning Is The Process of Developing, Analyzing, and Maintaining A PreliminaryredNo ratings yet

- National Income DeterminationDocument8 pagesNational Income DeterminationredNo ratings yet

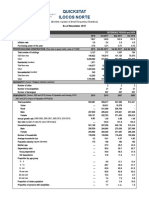

- Ilocos Norte Quickstat January 2015Document5 pagesIlocos Norte Quickstat January 2015redNo ratings yet

- The Three Pillars of SustainabilityDocument9 pagesThe Three Pillars of SustainabilityredNo ratings yet

- CSR Policy EdcDocument3 pagesCSR Policy EdcredNo ratings yet

- Train Law Sect. 31Document5 pagesTrain Law Sect. 31redNo ratings yet

- Economic SustainabilityDocument19 pagesEconomic SustainabilityredNo ratings yet

- RelfecltionDocument3 pagesRelfecltionredNo ratings yet

- Quickstat Ilocos Norte: (Monthly Update of Most Requested Statistics)Document4 pagesQuickstat Ilocos Norte: (Monthly Update of Most Requested Statistics)redNo ratings yet

- Events Coordinator Business PlanDocument10 pagesEvents Coordinator Business PlanredNo ratings yet

- Quickstat Ilocos Norte: (Monthly Update of Most Requested Statistics)Document4 pagesQuickstat Ilocos Norte: (Monthly Update of Most Requested Statistics)redNo ratings yet

- Increases Media Coverage: 1. Improves Public ImageDocument6 pagesIncreases Media Coverage: 1. Improves Public ImageredNo ratings yet

- Train Law Sect. 31Document5 pagesTrain Law Sect. 31redNo ratings yet

- Concrete BlockDocument3 pagesConcrete BlockredNo ratings yet

- Phoenix Petroleum Philippines, Inc.Document1 pagePhoenix Petroleum Philippines, Inc.redNo ratings yet

- CSR Evolution and the Development of Management TheoriesDocument15 pagesCSR Evolution and the Development of Management Theoriesalphabet gulanesNo ratings yet

- TBChap 005Document93 pagesTBChap 005Dylan BarronNo ratings yet

- TCS Corporate Sustainability Report 2012 13Document92 pagesTCS Corporate Sustainability Report 2012 13adityabaid4No ratings yet

- Case Gucci Positive Luxury ESSEC-G-213-1Document24 pagesCase Gucci Positive Luxury ESSEC-G-213-1Mohammed Aaquib MubeenNo ratings yet

- MAA763 Governance and Fraud: Revision T2 2017Document40 pagesMAA763 Governance and Fraud: Revision T2 2017MalikNo ratings yet

- Organic and Fairtrade Certified Clothing BrandsDocument3 pagesOrganic and Fairtrade Certified Clothing BrandsPreksha PandeyNo ratings yet

- Module-Principles of MarketingDocument176 pagesModule-Principles of Marketingjuvan0575% (4)

- Tata Steel: Q1. Apply PESTLE, FIVE FORCES & SWOT Analysis On Following Tata BusinessDocument51 pagesTata Steel: Q1. Apply PESTLE, FIVE FORCES & SWOT Analysis On Following Tata BusinessAnsh AnandNo ratings yet

- Week 5 Notes 1Document1 pageWeek 5 Notes 1Jilyn roque100% (1)

- Ethics CSR Corporate GovernanceDocument2 pagesEthics CSR Corporate GovernanceSatyam SharmaNo ratings yet

- Corporate Social Responsibility in Emerging Market Economies - Determinants, Consequences, and Future Research DirectionsDocument53 pagesCorporate Social Responsibility in Emerging Market Economies - Determinants, Consequences, and Future Research DirectionsJana HassanNo ratings yet

- Coca-Cola's Socio-Cultural Impact in IndiaDocument2 pagesCoca-Cola's Socio-Cultural Impact in IndiaLalima Bassi33% (3)

- VNM - Annual Report 2021Document121 pagesVNM - Annual Report 2021Hải Yến Võ ThịNo ratings yet

- HPCL CSR Social Audit ReportDocument56 pagesHPCL CSR Social Audit Reportllr_ka_happaNo ratings yet

- Samsung Internship ReportDocument30 pagesSamsung Internship ReportRõméø Rãhùl50% (4)

- 1 SMDocument15 pages1 SMRijanita MariyanaNo ratings yet

- Project - IsrDocument42 pagesProject - IsrhimanshuNo ratings yet

- Universiti Teknologi Mara Final Assessment: Confidential AC/FEB2021/CRG650Document9 pagesUniversiti Teknologi Mara Final Assessment: Confidential AC/FEB2021/CRG650Norkhaiihiidayah WatiieNo ratings yet

- IRRBAM Vol2Document100 pagesIRRBAM Vol2GwenNo ratings yet

- Contemporary Business: Business Ethics and Social ResponsibilityDocument23 pagesContemporary Business: Business Ethics and Social ResponsibilityAlex diorNo ratings yet

- 09574099710805556Document50 pages09574099710805556heartback100% (2)

- Muslim Consumer BehaviorDocument26 pagesMuslim Consumer BehaviorKan SonNo ratings yet

- GreenICT OntologyDocument22 pagesGreenICT OntologybanatusNo ratings yet

- The Influence of Collaboration and Decision - Making in Sustainable Supply Chain Management - A Case Study Analysis On Skechers USA Inc.Document96 pagesThe Influence of Collaboration and Decision - Making in Sustainable Supply Chain Management - A Case Study Analysis On Skechers USA Inc.Angelica ChavesNo ratings yet

- Wajiha Tariq. Organizational Behavior. Assignment 1Document4 pagesWajiha Tariq. Organizational Behavior. Assignment 1Amina QamarNo ratings yet

- About UsDocument3 pagesAbout UsMadushanNo ratings yet

- Down To Earth Sept 16-30Document76 pagesDown To Earth Sept 16-30Anandbabu RadhakrishnanNo ratings yet

- Literature Review On Accounting StandardsDocument8 pagesLiterature Review On Accounting Standardsafmzywxfelvqoj100% (1)

- CN Asia Annual Report 2015Document106 pagesCN Asia Annual Report 2015Siti AmalinaNo ratings yet

- Week 4-5-Creating Futures Sustainable Enterprise and Innovation - Promoting SustainabilityDocument36 pagesWeek 4-5-Creating Futures Sustainable Enterprise and Innovation - Promoting SustainabilityAfaf AnwarNo ratings yet