You might also like

- Hampton Machine Tool CaseDocument7 pagesHampton Machine Tool CaseChaitanya80% (10)

- Brand Architecture and PortfolioDocument24 pagesBrand Architecture and PortfolioAdil100% (2)

- Visual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsFrom EverandVisual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsNo ratings yet

- Computerised Accounting Practice Set Using MYOB AccountRight - Advanced Level: Australian EditionFrom EverandComputerised Accounting Practice Set Using MYOB AccountRight - Advanced Level: Australian EditionNo ratings yet

- Chapter 3&4 - HR StratDocument8 pagesChapter 3&4 - HR StratAlyannaNo ratings yet

- Cannon Ball Review Part 4Document20 pagesCannon Ball Review Part 4Jhopel Casagnap Eman100% (1)

- Crux Case Book 2023Document344 pagesCrux Case Book 2023vsmbhav05No ratings yet

- Project Case 9-30 Master BudgetDocument6 pagesProject Case 9-30 Master Budgetleizalm29% (7)

- Understanding Financial MarketsDocument80 pagesUnderstanding Financial Marketsabhijeit86100% (2)

- Chapter 3 SolutionsDocument7 pagesChapter 3 Solutionshassan.murad63% (8)

- Module 1 Process Costing Nature and OperationsDocument19 pagesModule 1 Process Costing Nature and Operationscha11100% (3)

- Project Management PPT FinalDocument14 pagesProject Management PPT FinalA KNo ratings yet

- Master Budgeting (Sample Problems With Answers)Document11 pagesMaster Budgeting (Sample Problems With Answers)Jonalyn TaboNo ratings yet

- Treasury Management Vs Cash Management Answer To Warm Up ExercisesDocument8 pagesTreasury Management Vs Cash Management Answer To Warm Up Exercisesephraim0% (1)

- 2017 Fall Solution: Sales BudgetDocument3 pages2017 Fall Solution: Sales BudgetRaam Tha BossNo ratings yet

- Acctg 202Document9 pagesAcctg 202Lore Desa CenizaNo ratings yet

- Questions On Cash Budget-2Document7 pagesQuestions On Cash Budget-2Mpolokeng HlabanaNo ratings yet

- Sales, Expenses and Cash Flow AnalysisDocument6 pagesSales, Expenses and Cash Flow AnalysisRUPIKA R GNo ratings yet

- Total Cash Available (1 + 2) 82,500 124,000 89,275Document6 pagesTotal Cash Available (1 + 2) 82,500 124,000 89,275Nischal LawojuNo ratings yet

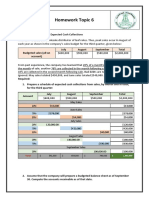

- Homework Topic 6: EXERCISE 8-1 Schedule of Expected Cash CollectionsDocument3 pagesHomework Topic 6: EXERCISE 8-1 Schedule of Expected Cash CollectionskhetamNo ratings yet

- Case 8-31: April May June QuarterDocument2 pagesCase 8-31: April May June QuarterileviejoieNo ratings yet

- Assignment 17 SolutionDocument2 pagesAssignment 17 SolutionSinpaoNo ratings yet

- HomeworkDocument3 pagesHomeworkZihao TangNo ratings yet

- Cash Receipts and Disbursements ScheduleDocument10 pagesCash Receipts and Disbursements ScheduleSYED ANEES ALINo ratings yet

- Exercises 7A1 and 7B1: Book: Administrative AccountingDocument9 pagesExercises 7A1 and 7B1: Book: Administrative AccountingScribdTranslationsNo ratings yet

- Managerial Accounting Chapter 7Document4 pagesManagerial Accounting Chapter 7Neema MarkNo ratings yet

- 08 Task PerformanceDocument3 pages08 Task PerformanceBetchang AquinoNo ratings yet

- Exercise 1: Schedule of Expected Cash CollectionDocument7 pagesExercise 1: Schedule of Expected Cash CollectionLenard Josh IngallaNo ratings yet

- Mas ReviewerDocument14 pagesMas ReviewerMichelle AvilesNo ratings yet

- Tut Mene AccDocument7 pagesTut Mene Accnatasya angelNo ratings yet

- Budgeting Activity - Annamarisse Parungao - BSA 2BDocument6 pagesBudgeting Activity - Annamarisse Parungao - BSA 2BAnnamarisse parungaoNo ratings yet

- 08 TP - Evangelista Angela - 501PDocument9 pages08 TP - Evangelista Angela - 501PBetchang AquinoNo ratings yet

- Practice Question of Cash BudgetingDocument5 pagesPractice Question of Cash BudgetingHira RaisNo ratings yet

- Group Managerial AccountingDocument9 pagesGroup Managerial AccountingSlamet SalimNo ratings yet

- Financial PlanningDocument6 pagesFinancial Planningakimasa raizeNo ratings yet

- The Answer For The Exercise of Trading Company The ABC StoreDocument6 pagesThe Answer For The Exercise of Trading Company The ABC StoreSajakul SornNo ratings yet

- Ain20190418028 ModifiedDocument5 pagesAin20190418028 ModifiedNiomi GolraiNo ratings yet

- Exercise 1 Margarett Company: Sales BudgetDocument4 pagesExercise 1 Margarett Company: Sales BudgetHannaniah PabicoNo ratings yet

- Problem On Cash Budget: 8 (The End of The Prior Quarter), The Company's Balance Were As FollowsDocument4 pagesProblem On Cash Budget: 8 (The End of The Prior Quarter), The Company's Balance Were As Followsshreya chapagainNo ratings yet

- Cash BudgetingDocument3 pagesCash Budgetingsunil.ctNo ratings yet

- Schedule of Cash Collection, Production Needs, and Manufacturing Overhead CostsDocument5 pagesSchedule of Cash Collection, Production Needs, and Manufacturing Overhead CostsYến Hoàng HảiNo ratings yet

- Answer Key Materi 1 UtsDocument10 pagesAnswer Key Materi 1 UtsKusuma Aji SuryaNo ratings yet

- Boomstick Corp quarterly budgets and financial statementsDocument14 pagesBoomstick Corp quarterly budgets and financial statementsDivya GoyalNo ratings yet

- Chapter 7Document57 pagesChapter 7scryx bloodNo ratings yet

- Exercise 2.1Document9 pagesExercise 2.1Nurul ShazalinaNo ratings yet

- Cash Budget For January Thru July Based On Expected Sales Nov Dec Jan Feb MarDocument6 pagesCash Budget For January Thru July Based On Expected Sales Nov Dec Jan Feb MardanielkangNo ratings yet

- Fin420 AssignmentDocument2 pagesFin420 Assignment2023607226No ratings yet

- TUTORIAL 8 BudgetDocument7 pagesTUTORIAL 8 Budgetsarahayeesha1No ratings yet

- Bai Tap KTQT 2Document12 pagesBai Tap KTQT 2Tram NguyenNo ratings yet

- Budgeting and Budgetary ControlDocument13 pagesBudgeting and Budgetary ControlRenu PoddarNo ratings yet

- Latihan Susun LK & Arus Kas (Rommy Haris Winanda)Document9 pagesLatihan Susun LK & Arus Kas (Rommy Haris Winanda)rommyNo ratings yet

- Acct 2020 Excel Budget ProblemDocument6 pagesAcct 2020 Excel Budget Problemapi-307661249No ratings yet

- Adjusting EntriesDocument19 pagesAdjusting EntriesLoanita EarlyantiNo ratings yet

- 1.1 Answer - Exercise Production Budget GildenDocument2 pages1.1 Answer - Exercise Production Budget GildenHazim BadrinNo ratings yet

- CashBudgettutsolnsDocument12 pagesCashBudgettutsolnsuudsefdNo ratings yet

- Sales Budget and Financial ProjectionsDocument12 pagesSales Budget and Financial ProjectionsAbejero Trisha Nicole A.No ratings yet

- CF 19-03-21 (BudgetDocument21 pagesCF 19-03-21 (BudgetTarisya PermatasariNo ratings yet

- Homework Submission Point For Lecture Date 15 - 8Document8 pagesHomework Submission Point For Lecture Date 15 - 8Hạ Phạm NhậtNo ratings yet

- Quiz No. 2 Multiple Choice and Problem Solving QuestionsDocument6 pagesQuiz No. 2 Multiple Choice and Problem Solving QuestionsNonami AbicoNo ratings yet

- Pasicolan - Case StudybedgetingDocument5 pagesPasicolan - Case StudybedgetingMark Joshua PasicolanNo ratings yet

- BT Ke Toan Quan TriDocument39 pagesBT Ke Toan Quan TriTram NguyenNo ratings yet

- Soal Final Test Farizauriga Periodical 2023-24Document19 pagesSoal Final Test Farizauriga Periodical 2023-24VelzaNo ratings yet

- Solutions To Chapter 15 Questions - Managing Current AssetsDocument5 pagesSolutions To Chapter 15 Questions - Managing Current AssetsSyeda MiznaNo ratings yet

- Proj 2Document15 pagesProj 2Shahan AsifNo ratings yet

- XYZ Sdn.Bhd. Cash Budget Analysis July-Sept 2011Document4 pagesXYZ Sdn.Bhd. Cash Budget Analysis July-Sept 2011nurainNo ratings yet

- Pawn Shop Revenues World Summary: Market Values & Financials by CountryFrom EverandPawn Shop Revenues World Summary: Market Values & Financials by CountryNo ratings yet

- Succession Planning StrategiesDocument2 pagesSuccession Planning StrategiesAlyannaNo ratings yet

- 0chapter 1-Strategic ManagementDocument19 pages0chapter 1-Strategic ManagementAlyannaNo ratings yet

- Compensation Assignment1Document2 pagesCompensation Assignment1AlyannaNo ratings yet

- Evidencia 2 Comparing MyproductDocument5 pagesEvidencia 2 Comparing MyproductOskar Sandoval A/NNo ratings yet

- Analysis of New Product Launch Using Google Double Click (Ritika and Sanchit Kaushal)Document13 pagesAnalysis of New Product Launch Using Google Double Click (Ritika and Sanchit Kaushal)ritika singh100% (5)

- Cannibalizations On Product Protfolio, Innovation and PromotionsDocument20 pagesCannibalizations On Product Protfolio, Innovation and Promotionsjasraj_singhNo ratings yet

- Responsibility Accounting and Transfer Pricing ProblemsDocument20 pagesResponsibility Accounting and Transfer Pricing ProblemsWeniel Dela VictoriaNo ratings yet

- GMO - Profits For The LongRun - Affirming The Case For QualityDocument7 pagesGMO - Profits For The LongRun - Affirming The Case For QualityHelio KwonNo ratings yet

- Lecture 2 Notes IDocument23 pagesLecture 2 Notes I林靖雯No ratings yet

- The Functions of Financial SystemDocument4 pagesThe Functions of Financial SystemMaha Lakshmi33% (3)

- Cinepolis & Exam 2018 - SolutionsDocument8 pagesCinepolis & Exam 2018 - Solutionsmathieu652540No ratings yet

- Syllabus For Acctg101 (Fundamentals of Accounting I) : Philippine Advent College - Salug CampusDocument9 pagesSyllabus For Acctg101 (Fundamentals of Accounting I) : Philippine Advent College - Salug CampusJM LomoljoNo ratings yet

- Digital Marketing Importance in The New Era: M.ShirishaDocument6 pagesDigital Marketing Importance in The New Era: M.ShirishaAfad KhanNo ratings yet

- Man Econ FinalsDocument5 pagesMan Econ FinalsJessel TagalogNo ratings yet

- International Marketing ConceptDocument14 pagesInternational Marketing Conceptginz2008No ratings yet

- Profit MaximisationDocument7 pagesProfit MaximisationAmir SadeeqNo ratings yet

- Customer-Centricity in Retail BankingDocument17 pagesCustomer-Centricity in Retail BankingMadalina PopescuNo ratings yet

- Selene Felix ResumeDocument2 pagesSelene Felix ResumeMary QuinzonNo ratings yet

- Westetal3e ch01Document24 pagesWestetal3e ch01biaskhjdafNo ratings yet

- Brand Equity: Pakistan Tobacco Company LimitedDocument26 pagesBrand Equity: Pakistan Tobacco Company LimitedAsif RiazNo ratings yet

- XII BST Oswaal SQPs Sample Papers 12 2024 @CUETCBSEDocument162 pagesXII BST Oswaal SQPs Sample Papers 12 2024 @CUETCBSEjapgunkaur1No ratings yet

- MCC5412 - Lecture 4Document38 pagesMCC5412 - Lecture 4Dickson ChanNo ratings yet

- Tugas Ke 5 Ade Hidayat Kelas 1a MMDocument4 pagesTugas Ke 5 Ade Hidayat Kelas 1a MMadeNo ratings yet

- Ansoff MatrixDocument3 pagesAnsoff Matrixbiswarup deyNo ratings yet

- Blackrock Special Report - Inflation-Linked Bonds PrimerDocument8 pagesBlackrock Special Report - Inflation-Linked Bonds PrimerGreg JachnoNo ratings yet

- ECO111 Quiz02 Spring2023-1Document56 pagesECO111 Quiz02 Spring2023-1Trần Quang NinhNo ratings yet

- Sumit FinalDocument27 pagesSumit FinalambrosialnectarNo ratings yet