You might also like

- The Basics of Life Insurance: The Answer to What Life Insurance is and How It Works: Personal Finance, #1From EverandThe Basics of Life Insurance: The Answer to What Life Insurance is and How It Works: Personal Finance, #1No ratings yet

- Let The Affection of Your Loved Ones Be Felt at All TimesDocument24 pagesLet The Affection of Your Loved Ones Be Felt at All TimesSudipto RoyNo ratings yet

- Tax Free Wealth: Learn the strategies and loopholes of the wealthy on lowering taxes by leveraging Cash Value Life Insurance, 1031 Real Estate Exchanges, 401k & IRA InvestingFrom EverandTax Free Wealth: Learn the strategies and loopholes of the wealthy on lowering taxes by leveraging Cash Value Life Insurance, 1031 Real Estate Exchanges, 401k & IRA InvestingNo ratings yet

- Poorna Suraksha BrochureDocument24 pagesPoorna Suraksha BrochureG P Rao TNo ratings yet

- Poorna Suraksha Brochure BRDocument22 pagesPoorna Suraksha Brochure BRecostarNo ratings yet

- You Invest. We Insure.: Century SIPDocument4 pagesYou Invest. We Insure.: Century SIPPratik SharmaNo ratings yet

- Saral Jeevan Bima Brochure-BRDocument10 pagesSaral Jeevan Bima Brochure-BRprabuNo ratings yet

- Retirement PlanDocument6 pagesRetirement PlanbaradreenaNo ratings yet

- SBI Life - Retire Smart - Brochure - Ver03Document16 pagesSBI Life - Retire Smart - Brochure - Ver03Vishal kaushalendra Kumar singhNo ratings yet

- RLMMP - BrochureDocument7 pagesRLMMP - BrochureAnjesh KumarNo ratings yet

- SBI Life - Saral Retirement Saver - BrochureDocument14 pagesSBI Life - Saral Retirement Saver - BrochureNitin KumarNo ratings yet

- Singlife Elite TermDocument8 pagesSinglife Elite TermDaniel OonNo ratings yet

- Click 2 Protect SchemeDocument10 pagesClick 2 Protect SchemeSandeep BhatiaNo ratings yet

- SBI Life - Saral Jeevan Bima - BrochureDocument9 pagesSBI Life - Saral Jeevan Bima - BrochureH.O. Rajendra TiwariNo ratings yet

- Edelweiss Tokio Life Wealth Ultima ReviewDocument2 pagesEdelweiss Tokio Life Wealth Ultima ReviewJagdeesh ShettyNo ratings yet

- IndiaFirst Smart Save Plan guideDocument16 pagesIndiaFirst Smart Save Plan guideVishal SharmaNo ratings yet

- P Nbs JB BrochureDocument5 pagesP Nbs JB BrochureavkashNo ratings yet

- Retire - Smart - Brochure - Brand ReimagineDocument16 pagesRetire - Smart - Brochure - Brand Reimagineneop lopianNo ratings yet

- Protect your loved ones with affordable term life coverageDocument12 pagesProtect your loved ones with affordable term life coverageYao Le Titanium ChenNo ratings yet

- MetLife Endowment Savings Plan PRINT Brochure - 2016 V2 - tcm47-27873Document4 pagesMetLife Endowment Savings Plan PRINT Brochure - 2016 V2 - tcm47-27873himanshu goyalNo ratings yet

- RNL Super Bachat Plus Suraksha Plan BrochureDocument20 pagesRNL Super Bachat Plus Suraksha Plan BrochureanupamNo ratings yet

- When It Comes To Securing Your Loved Ones, Trust Us.: Saral JeevanDocument10 pagesWhen It Comes To Securing Your Loved Ones, Trust Us.: Saral Jeevanjithin jayNo ratings yet

- Term Life Insurance FinalDocument10 pagesTerm Life Insurance FinalsearchingnobodyNo ratings yet

- IRaksha TROP Version2 Brochure WebDocument5 pagesIRaksha TROP Version2 Brochure WebNazeerNo ratings yet

- Edelweiss_Tokio_Life_Wealth_Accumulation_AcceleratedCover_V01_BrochureDocument10 pagesEdelweiss_Tokio_Life_Wealth_Accumulation_AcceleratedCover_V01_BrochureavisekgNo ratings yet

- PRUHealth FamLove-BrochureDocument12 pagesPRUHealth FamLove-BrochureDhey ZheNo ratings yet

- Client S Fitwellplus15 05092022131558Document15 pagesClient S Fitwellplus15 05092022131558Jonel GallazaNo ratings yet

- Be There For Your Family. Always.: Assure PlusDocument10 pagesBe There For Your Family. Always.: Assure PlusSidhant kumarNo ratings yet

- Brochure RockSolidDocument10 pagesBrochure RockSolidLaltu PaniNo ratings yet

- IndiaFirst Maha Jeevan Plan - BrochureDocument11 pagesIndiaFirst Maha Jeevan Plan - BrochureBirddoxyNo ratings yet

- Power Your Independent Retirement.: WWW - Sbilife.co - inDocument20 pagesPower Your Independent Retirement.: WWW - Sbilife.co - injithin jayNo ratings yet

- Jeevan Nivesh CanarahsbcDocument14 pagesJeevan Nivesh CanarahsbcVinesh ChandraNo ratings yet

- Ensure Your Family's Future With Bajaj Allianz New Risk Care PlanDocument2 pagesEnsure Your Family's Future With Bajaj Allianz New Risk Care PlanGuru9756No ratings yet

- Shubh Nivesh Brochure - BRDocument15 pagesShubh Nivesh Brochure - BRSumit RpNo ratings yet

- Mahalife Gold: Tata Aia Life InsuranceDocument5 pagesMahalife Gold: Tata Aia Life InsuranceFrancis ReddyNo ratings yet

- 1228 - ABSLI Wealth Infinia LeafletDocument11 pages1228 - ABSLI Wealth Infinia LeafletvamsipalagummiNo ratings yet

- Jeevan SafarDocument7 pagesJeevan SafarNishant SinhaNo ratings yet

- HDFC Click 2 Protect Plus: What Are The Key Features of This PlanDocument5 pagesHDFC Click 2 Protect Plus: What Are The Key Features of This PlanAniket DesaiNo ratings yet

- Sun Smarter Life ClassicDocument7 pagesSun Smarter Life Classicpaul jan sarachoNo ratings yet

- Saral Swadhan Supreme - Brochure - V01 15th JanDocument9 pagesSaral Swadhan Supreme - Brochure - V01 15th JanNitin KumarNo ratings yet

- SBI Life eShield - Affordable life insurance for MTNL employeesDocument20 pagesSBI Life eShield - Affordable life insurance for MTNL employeesVivek SharmaNo ratings yet

- Life and Health Insurance ChapterDocument29 pagesLife and Health Insurance ChapterWonde BiruNo ratings yet

- Kotak Classic Endowment Plan Brochure1Document12 pagesKotak Classic Endowment Plan Brochure1Kranthi Kumar ReddyNo ratings yet

- SBI Life - Smart Platina Assure - BrochureDocument12 pagesSBI Life - Smart Platina Assure - Brochuresourav agarwalNo ratings yet

- Fixed Money Back Plan - Brochure WebDocument7 pagesFixed Money Back Plan - Brochure WebsamNo ratings yet

- Jeevan - Sathi Eng BH PDFDocument2 pagesJeevan - Sathi Eng BH PDFNaygarp IhtapirtNo ratings yet

- Put your finances on autopilot with guaranteed benefitsDocument8 pagesPut your finances on autopilot with guaranteed benefitsDjddhNo ratings yet

- QC-3654 Guaranteed Wealth Plan Brochure - V5a - 1Document19 pagesQC-3654 Guaranteed Wealth Plan Brochure - V5a - 1202032053 imtnagNo ratings yet

- A One of Its Kind Plan: For Internal Circulation OnlyDocument16 pagesA One of Its Kind Plan: For Internal Circulation OnlyAdityaNo ratings yet

- Smart Growth Brochure Fina 0Document24 pagesSmart Growth Brochure Fina 0Sooraj KuruvathNo ratings yet

- Secure Family's Future OnlineDocument8 pagesSecure Family's Future OnlineabhishekNo ratings yet

- Smart Shield Brochure - BRDocument10 pagesSmart Shield Brochure - BRSumit RpNo ratings yet

- Enjoy your passions even in retirementDocument5 pagesEnjoy your passions even in retirementmuzpatNo ratings yet

- Shubh+Nivesh+Brochure BR+1Document15 pagesShubh+Nivesh+Brochure BR+1red proNo ratings yet

- Radiance Brochure PDFDocument25 pagesRadiance Brochure PDFTarakanta MohantyNo ratings yet

- Max New York Life InsuranceDocument27 pagesMax New York Life InsurancehardikpawarNo ratings yet

- A one of its Kind Non-Participating Endowment Life Insurance PlanDocument18 pagesA one of its Kind Non-Participating Endowment Life Insurance PlanKunal ShahNo ratings yet

- Jeevan Sathi PlusDocument6 pagesJeevan Sathi Plusap87No ratings yet

- Sales and Distribution PresentationDocument12 pagesSales and Distribution PresentationRaushan kumarNo ratings yet

- Key Features DocumentDocument25 pagesKey Features DocumentPectro BiotechNo ratings yet

- Wbi 37162Document16 pagesWbi 37162Sanjay RaghuvanshiNo ratings yet

- Subject Utilization ReportDocument1 pageSubject Utilization ReportSanjay RaghuvanshiNo ratings yet

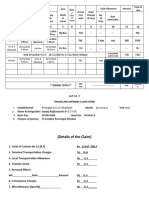

- (Details of The Claim) : 1 2 3 4 5 6 7 8 9 10 11 12 by Bus - 74/ - 74/ - 74/ - 1 Day 180 254Document2 pages(Details of The Claim) : 1 2 3 4 5 6 7 8 9 10 11 12 by Bus - 74/ - 74/ - 74/ - 1 Day 180 254Sanjay RaghuvanshiNo ratings yet

- 2020031215848486Document27 pages2020031215848486Sanjay RaghuvanshiNo ratings yet

- IETS-HP - Installation Document-Ver1.1Document27 pagesIETS-HP - Installation Document-Ver1.1Sanjay Raghuvanshi100% (1)

- © Ncert Not To Be Republished: O Kikjh) JKTK VKSJ RHFKZ K KHDocument12 pages© Ncert Not To Be Republished: O Kikjh) JKTK VKSJ RHFKZ K KHAshish KushwahaNo ratings yet

- Vehicle Systems and Components QuizDocument27 pagesVehicle Systems and Components QuizSanjay Raghuvanshi100% (1)

- HPPSC Recruitment for Finance and Accounts ServiceDocument13 pagesHPPSC Recruitment for Finance and Accounts ServiceSanjay RaghuvanshiNo ratings yet

- Vehicle Systems and Components QuizDocument27 pagesVehicle Systems and Components QuizSanjay Raghuvanshi100% (1)

- Java ScriptttDocument8 pagesJava ScriptttSanjay RaghuvanshiNo ratings yet

- PHP in HindiDocument56 pagesPHP in HindiRitesh Bagwale100% (1)

- Almost Complete Database of Gate 2012 Cs ResultsDocument319 pagesAlmost Complete Database of Gate 2012 Cs ResultsSanjay RaghuvanshiNo ratings yet

- CS GATE'2017 Paper 02 Key SolutionDocument32 pagesCS GATE'2017 Paper 02 Key Solutionvarsha1504No ratings yet

- INA Award List in RDocument1 pageINA Award List in RSanjay RaghuvanshiNo ratings yet

- PN B Met Life Mera Term PlanDocument8 pagesPN B Met Life Mera Term PlanSanjay RaghuvanshiNo ratings yet

- Digital SystemsDocument675 pagesDigital SystemsvikramjhaNo ratings yet

- Improving Buffalo Breeding Through Genetics and ManagementDocument12 pagesImproving Buffalo Breeding Through Genetics and ManagementrichardikNo ratings yet

- Iit PatnaDocument8 pagesIit PatnaSanjay RaghuvanshiNo ratings yet

- Chemistry Analyzer Mindray BS-230 BrochureDocument8 pagesChemistry Analyzer Mindray BS-230 BrochureVinsmoke Sanji100% (2)

- Infertility and ItDocument3 pagesInfertility and ItDeepanshu ShakargayeNo ratings yet

- Promega Timing Apoptosis Assay PublicationDocument4 pagesPromega Timing Apoptosis Assay Publicationαγαπημένη του ΧριστούNo ratings yet

- Chapter-3. Human Reproduction Case Based QuestionsDocument33 pagesChapter-3. Human Reproduction Case Based QuestionsSania GeorgeNo ratings yet

- 01 - CortisolDocument276 pages01 - CortisolTy Lucas100% (5)

- Edma Classification ReagentsDocument82 pagesEdma Classification ReagentsHarun GanićNo ratings yet

- Thyroid NeoplasmsDocument62 pagesThyroid Neoplasmshemanarasimha gandikotaNo ratings yet

- Thyroid Eye Disease Diagnosis and TreatmentDocument486 pagesThyroid Eye Disease Diagnosis and TreatmentUnsmil UnguNo ratings yet

- Activity in Digestive System I.: Name of Structure Description No. of Structure (Answer)Document2 pagesActivity in Digestive System I.: Name of Structure Description No. of Structure (Answer)Lainie ZefiahNo ratings yet

- Endocrinology Question 1Document16 pagesEndocrinology Question 1BasirQidwai100% (4)

- Abbott Annual Report 2016Document80 pagesAbbott Annual Report 2016Ojo-publico.comNo ratings yet

- Presentation ScheduleDocument11 pagesPresentation Scheduledesy armalinaNo ratings yet

- Hormones Intro QuestionsDocument2 pagesHormones Intro Questionspiotr.ng.333No ratings yet

- Abegail Joy B. Manlunas BS Psychology: Endocrine System Organ Hormone Function Disorder If Too High Disorder If Too LowDocument4 pagesAbegail Joy B. Manlunas BS Psychology: Endocrine System Organ Hormone Function Disorder If Too High Disorder If Too LowabegailmanlunasNo ratings yet

- Journal of Functional Foods: SciencedirectDocument8 pagesJournal of Functional Foods: SciencedirectYamile BravoNo ratings yet

- Lesson 1. Right Hemisphere / Left Hemisphere: 1.1 VocabularyDocument3 pagesLesson 1. Right Hemisphere / Left Hemisphere: 1.1 Vocabularyyamel BisonoNo ratings yet

- Applied Veterinary Andrology and Artificial InseminationDocument146 pagesApplied Veterinary Andrology and Artificial InseminationDeep Patel50% (2)

- Ast (Got) BXC0201 A25 A15Document2 pagesAst (Got) BXC0201 A25 A15jef1234321No ratings yet

- Cell Injury: Dr. Sanjiv Kumar Assistant Professor, Deptt. of Pathology, BVC, PatnaDocument32 pagesCell Injury: Dr. Sanjiv Kumar Assistant Professor, Deptt. of Pathology, BVC, PatnaAjinkya JadhaoNo ratings yet

- CLAUDE BOUCHARD - Handbook of Obesity - Etiology and Pathophysiology, Second Edition (2007, Taylor and Francis)Document1,056 pagesCLAUDE BOUCHARD - Handbook of Obesity - Etiology and Pathophysiology, Second Edition (2007, Taylor and Francis)Ewerson CruzNo ratings yet

- Casas, Jo-An Pauline A. - (LAB) Basic Concepts in NutritionDocument2 pagesCasas, Jo-An Pauline A. - (LAB) Basic Concepts in NutritionCasas, Jo-an Pauline A.No ratings yet

- Cambridge IGCSE: BIOLOGY 0610/32Document20 pagesCambridge IGCSE: BIOLOGY 0610/32bipin jainNo ratings yet

- Mini by Me - DR SuhilDocument188 pagesMini by Me - DR SuhilA L N O F E E ,TMNo ratings yet

- Immulite Assay Menu PDFDocument2 pagesImmulite Assay Menu PDFОлександрNo ratings yet

- Low-Dose Desoxycorticosterone Pivalate Treatment of Hypoadrenocorticism in Dogs: A Randomized Controlled Clinical TrialDocument9 pagesLow-Dose Desoxycorticosterone Pivalate Treatment of Hypoadrenocorticism in Dogs: A Randomized Controlled Clinical TrialEduardo SantamaríaNo ratings yet

- Thyroid function test report for 18-year old maleDocument2 pagesThyroid function test report for 18-year old malearjun guptaNo ratings yet

- Issue #75 (January 2021)Document89 pagesIssue #75 (January 2021)Đạt NguyễnNo ratings yet

- Infrared Reference Spectra F-KDocument22 pagesInfrared Reference Spectra F-KGalih Widys PambayunNo ratings yet

- Grade 12 - General Biology2 - Q4 - Module - 5 - Homeostasis and Feedback Mechanisms. For PrintingDocument12 pagesGrade 12 - General Biology2 - Q4 - Module - 5 - Homeostasis and Feedback Mechanisms. For PrintingAlexa ValdezNo ratings yet

- 2b Case StudyDocument5 pages2b Case StudyCkaye MontilNo ratings yet