You might also like

- STRATEGYDocument44 pagesSTRATEGYsumit guptaNo ratings yet

- GW Company 41st Annual Report 2016-17Document444 pagesGW Company 41st Annual Report 2016-17sumit guptaNo ratings yet

- Quality Dividend Yield Stocks - 301216Document5 pagesQuality Dividend Yield Stocks - 301216sumit guptaNo ratings yet

- Consulting-Ten Commandments of Small Business (Lesson)Document3 pagesConsulting-Ten Commandments of Small Business (Lesson)sumit guptaNo ratings yet

- Consulting-Ten Commandments of Small Business (Lesson)Document1 pageConsulting-Ten Commandments of Small Business (Lesson)nenu_100No ratings yet

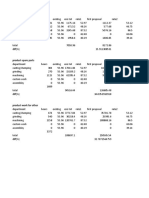

- Comparing department production rates and costs across multiple proposalsDocument2 pagesComparing department production rates and costs across multiple proposalssumit guptaNo ratings yet

- Consulting-Ten Commandments of Small Business (Lesson)Document1 pageConsulting-Ten Commandments of Small Business (Lesson)nenu_100No ratings yet

- Multibagger Stock IdeasDocument14 pagesMultibagger Stock IdeasrajanbondeNo ratings yet

- 27 April stock picks and 5 May Uco Bank targetDocument1 page27 April stock picks and 5 May Uco Bank targetsumit guptaNo ratings yet

- India in Crisis 2017 PDFDocument43 pagesIndia in Crisis 2017 PDFVinayNo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5783)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (890)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (72)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Magzine Forbes PDFDocument126 pagesMagzine Forbes PDFYOGENDER KUMAR100% (2)

- China Banking Corporation v. CIRDocument2 pagesChina Banking Corporation v. CIRRaymond Cheng80% (5)

- 20181112111447443373Document62 pages20181112111447443373HươngNo ratings yet

- Suggested Solutions To Practical ExercisesDocument38 pagesSuggested Solutions To Practical ExercisesDavidNo ratings yet

- Chapter 1: Fundamental Principles TaxationDocument2 pagesChapter 1: Fundamental Principles TaxationRogelio Olasos BernobaNo ratings yet

- PediaSure Marketing Strategy AnalysisDocument21 pagesPediaSure Marketing Strategy AnalysisAsmer Duraid KhanNo ratings yet

- SPS-Avelino-v.-Celedonio 2Document7 pagesSPS-Avelino-v.-Celedonio 2Jorge M. GarciaNo ratings yet

- Lidasan v. COMELEC: Rider Clause: Every Bill Passed by The Congress Shall Embrace OnlyDocument4 pagesLidasan v. COMELEC: Rider Clause: Every Bill Passed by The Congress Shall Embrace Onlyangelo doceoNo ratings yet

- Porters 5Document6 pagesPorters 5Divyavadan MateNo ratings yet

- FIN 325-3-2 Final Project Milestone Two Vertical and Horizontal Analysis Saeed Algarni Facebook IDocument9 pagesFIN 325-3-2 Final Project Milestone Two Vertical and Horizontal Analysis Saeed Algarni Facebook IAlison JcNo ratings yet

- Pricnciple of Maximum Social AdvantageDocument8 pagesPricnciple of Maximum Social Advantagelegendishal5No ratings yet

- Intro To Corporate FinanceDocument75 pagesIntro To Corporate FinanceRashid HussainNo ratings yet

- RFP135 - AMR For PESCO (T1) and MEPCO (T2) - AMEND 1 REVISED PDFDocument39 pagesRFP135 - AMR For PESCO (T1) and MEPCO (T2) - AMEND 1 REVISED PDFAmin AzadNo ratings yet

- New Method of National Income Accounting: Courses Offered: Rbi Grade B Sebi NabardDocument6 pagesNew Method of National Income Accounting: Courses Offered: Rbi Grade B Sebi NabardSai harshaNo ratings yet

- Latihan 1Document25 pagesLatihan 1Sanda Patrisia KomalasariNo ratings yet

- Tax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Document1 pageTax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)AK तकNo ratings yet

- How PESTLE Analysis Helps Tesco's SuccessDocument5 pagesHow PESTLE Analysis Helps Tesco's SuccessAkhil BhatiaNo ratings yet

- Collection of HC and SC DecisionsDocument63 pagesCollection of HC and SC DecisionsDayavantiNo ratings yet

- Punjab Police Performance DataDocument16 pagesPunjab Police Performance DataKhurram PervaizNo ratings yet

- ITB NotesDocument84 pagesITB NotesSadiaNo ratings yet

- Pre-Membership Requirements: Quezon Public School Teachers and Employees Multipurpose CooperativeDocument2 pagesPre-Membership Requirements: Quezon Public School Teachers and Employees Multipurpose CooperativeRoselyn San Diego PacaigueNo ratings yet

- PRF192 Workshop 01 SolutionsDocument7 pagesPRF192 Workshop 01 SolutionsLê Hồng PhướcNo ratings yet

- Pgp12038 A Chandana Landa DaDocument7 pagesPgp12038 A Chandana Landa DaChandana LandaNo ratings yet

- Ahmed Villas, Kacha Shahab Pura, ., Sialkot Sialkot Arifa MamoonaDocument4 pagesAhmed Villas, Kacha Shahab Pura, ., Sialkot Sialkot Arifa MamoonaZeeshan Haider RizviNo ratings yet

- Impact of Income Tax On Economic GrowthDocument16 pagesImpact of Income Tax On Economic Growthrahul singhNo ratings yet

- Trinity College London exam invoiceDocument2 pagesTrinity College London exam invoiceAlbert TaczNo ratings yet

- Corporate: Advantage ProgrammeDocument16 pagesCorporate: Advantage ProgrammeVinay RaoNo ratings yet

- Case:: Swedish Match Phil., Inc. Vs Treasurer of City of ManilaDocument10 pagesCase:: Swedish Match Phil., Inc. Vs Treasurer of City of ManilaVALENTINE MERCY MORALESNo ratings yet

- The Origins of Contemporary France by Hippolyte Taine - Volume 2Document699 pagesThe Origins of Contemporary France by Hippolyte Taine - Volume 2j tullNo ratings yet

- Bumper 2Document7 pagesBumper 2shruthikanambiarNo ratings yet