You might also like

- 2018-12 Monthly Housing Market OutlookDocument27 pages2018-12 Monthly Housing Market OutlookC.A.R. Research & Economics100% (1)

- 2018-02 February Housing Market OutlookDocument22 pages2018-02 February Housing Market OutlookC.A.R. Research & EconomicsNo ratings yet

- 2018-10 Monthly Housing Market OutlookDocument27 pages2018-10 Monthly Housing Market OutlookC.A.R. Research & Economics100% (2)

- 2017-12 Monthly Housing Market OutlookDocument19 pages2017-12 Monthly Housing Market OutlookC.A.R. Research & Economics100% (2)

- Monthly Housing Market Outlook 2017-04Document16 pagesMonthly Housing Market Outlook 2017-04C.A.R. Research & Economics100% (2)

- Q 219 Miami Beach MatrixDocument5 pagesQ 219 Miami Beach MatrixAnonymous gRjrOsy4No ratings yet

- 2018-11 Monthly Housing Market Outlook (Public)Document27 pages2018-11 Monthly Housing Market Outlook (Public)C.A.R. Research & Economics100% (1)

- 2017-11 Monthly Housing Market OutlookDocument19 pages2017-11 Monthly Housing Market OutlookC.A.R. Research & EconomicsNo ratings yet

- November 2017 Monthly Housing Market OutlookDocument19 pagesNovember 2017 Monthly Housing Market OutlookBrian RaynohaNo ratings yet

- Monthly Housing Market Outlook 2017-02Document15 pagesMonthly Housing Market Outlook 2017-02C.A.R. Research & EconomicsNo ratings yet

- 2019-05-02 Mid Yr. LunchDocument65 pages2019-05-02 Mid Yr. LunchC.A.R. Research & EconomicsNo ratings yet

- Monthly Housing Market Outlook 2017-01Document15 pagesMonthly Housing Market Outlook 2017-01C.A.R. Research & EconomicsNo ratings yet

- 2023-03 Monthly Housing Market OutlookDocument57 pages2023-03 Monthly Housing Market OutlookC.A.R. Research & Economics100% (1)

- Latin America 2020 Forecast and Key Vertical Trends AnalysisDocument45 pagesLatin America 2020 Forecast and Key Vertical Trends AnalysisRodrigo MendonçaNo ratings yet

- July 2018 Current Sales & Price StatisticsDocument2 pagesJuly 2018 Current Sales & Price StatisticsBrian RaynohaNo ratings yet

- Today's Market : Riverside Area Local Market Report, Third Quarter 2009Document5 pagesToday's Market : Riverside Area Local Market Report, Third Quarter 2009Sub2MDNo ratings yet

- 2018-09 Monthly Housing Market Outlook 101918Document19 pages2018-09 Monthly Housing Market Outlook 101918Alma MenchacaNo ratings yet

- 2023-06 Monthly Housing Market OutlookDocument57 pages2023-06 Monthly Housing Market OutlookC.A.R. Research & EconomicsNo ratings yet

- Traditional HAIDocument9 pagesTraditional HAIC.A.R. Research & Economics100% (1)

- Monthly Housing Market Outlook 2017-04Document16 pagesMonthly Housing Market Outlook 2017-04C.A.R. Research & EconomicsNo ratings yet

- Reducing The Barriers To Affordable Housing: July 10, 2006Document35 pagesReducing The Barriers To Affordable Housing: July 10, 2006M-NCPPCNo ratings yet

- 2023-Q1 Traditional Housing Affordability Index (HAI)Document9 pages2023-Q1 Traditional Housing Affordability Index (HAI)C.A.R. Research & EconomicsNo ratings yet

- LA Economic Vitals Dec Jan 2021Document5 pagesLA Economic Vitals Dec Jan 2021ChrisMNo ratings yet

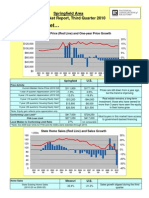

- Today's Market : Springfield Area Local Market Report, Third Quarter 2010Document7 pagesToday's Market : Springfield Area Local Market Report, Third Quarter 2010phatty34No ratings yet

- Traditional HAI PresentationDocument9 pagesTraditional HAI PresentationC.A.R. Research & EconomicsNo ratings yet

- Traditional HAIDocument14 pagesTraditional HAIC.A.R. Research & EconomicsNo ratings yet

- Monthly Housing Market OutlookDocument57 pagesMonthly Housing Market OutlookC.A.R. Research & EconomicsNo ratings yet

- 2024-02 Monthly Housing Market OutlookDocument57 pages2024-02 Monthly Housing Market OutlookC.A.R. Research & Economics100% (1)

- Pending Home Sales Index - 2017-05Document10 pagesPending Home Sales Index - 2017-05C.A.R. Research & EconomicsNo ratings yet

- Exploring The Disruptive Force of Retail M&A: Michael JohnsDocument20 pagesExploring The Disruptive Force of Retail M&A: Michael JohnsVineetNo ratings yet

- Market Snapshot Full Years 08-09Document1 pageMarket Snapshot Full Years 08-09Breckenridge Grand Real EstateNo ratings yet

- 2023-11 Monthly Housing Market OutlookDocument57 pages2023-11 Monthly Housing Market OutlookC.A.R. Research & Economics100% (1)

- Miami Sales Coastal Mainland: Report Data Brief - Not For DistributionDocument4 pagesMiami Sales Coastal Mainland: Report Data Brief - Not For DistributionAnonymous Feglbx5No ratings yet

- 2020-09 Monthly Housing Market OutlookDocument50 pages2020-09 Monthly Housing Market OutlookC.A.R. Research & EconomicsNo ratings yet

- Savage 3.19 Market ReportDocument1 pageSavage 3.19 Market ReportLeslie DahlenNo ratings yet

- 2024-01 Monthly Housing Market OutlookDocument57 pages2024-01 Monthly Housing Market OutlookC.A.R. Research & EconomicsNo ratings yet

- GRAR 2022-Q1 SummaryDocument4 pagesGRAR 2022-Q1 SummaryNews 8 WROCNo ratings yet

- 2023-05 Monthly Housing Market OutlookDocument57 pages2023-05 Monthly Housing Market OutlookC.A.R. Research & EconomicsNo ratings yet

- 2023-10 Monthly Housing Market OutlookDocument57 pages2023-10 Monthly Housing Market OutlookC.A.R. Research & EconomicsNo ratings yet

- 2023-12 Monthly Housing Market OutlookDocument57 pages2023-12 Monthly Housing Market OutlookC.A.R. Research & Economics100% (1)

- 2019 Advertising Kit v1.02Document16 pages2019 Advertising Kit v1.02indiaoriginNo ratings yet

- GRAR Summary 2022-Q4Document5 pagesGRAR Summary 2022-Q4Tyler DiedrichNo ratings yet

- Fredericksburg Americas Alliance MarketBeat Retail Q12020 PDFDocument2 pagesFredericksburg Americas Alliance MarketBeat Retail Q12020 PDFKevin ParkerNo ratings yet

- Paulson 2007 Year End Report Earns Nearly 600Document16 pagesPaulson 2007 Year End Report Earns Nearly 600Tunaljit ChoudhuryNo ratings yet

- Excel Dashboard Templates 29Document2 pagesExcel Dashboard Templates 29Foxuae Abu DahbiNo ratings yet

- Monthly Housing Market OutlookDocument57 pagesMonthly Housing Market OutlookC.A.R. Research & EconomicsNo ratings yet

- NMF 2018 Kansas City MF ReportDocument7 pagesNMF 2018 Kansas City MF ReportPhilip Maxwell AftuckNo ratings yet

- Ks Whopays FactsheetDocument2 pagesKs Whopays FactsheetbrentwistromNo ratings yet

- Traditional HAI PresentationDocument9 pagesTraditional HAI PresentationC.A.R. Research & EconomicsNo ratings yet

- March 2019 Local Market UpdateDocument18 pagesMarch 2019 Local Market UpdateLuci EdwardsNo ratings yet

- 2018-06-01 CA Mid-Year Forecast UpdateDocument49 pages2018-06-01 CA Mid-Year Forecast UpdateC.A.R. Research & Economics100% (1)

- Edtt Tourism Market Monitor 2019 12Document5 pagesEdtt Tourism Market Monitor 2019 12Anthony BrosNo ratings yet

- Selling Canadian Books in Colombia: A Guide for Canadian PublishersFrom EverandSelling Canadian Books in Colombia: A Guide for Canadian PublishersNo ratings yet

- Unloved Bull Markets: Getting Rich the Easy Way by Riding Bull MarketsFrom EverandUnloved Bull Markets: Getting Rich the Easy Way by Riding Bull MarketsNo ratings yet

- Obama’S Wonder Years: 8 Years of Lower Unemployment & Rising Stock MarketsFrom EverandObama’S Wonder Years: 8 Years of Lower Unemployment & Rising Stock MarketsNo ratings yet

- The Pros & Cons of Homeownership #3: Inflation Protection: Financial Freedom, #209From EverandThe Pros & Cons of Homeownership #3: Inflation Protection: Financial Freedom, #209No ratings yet

- Bypassed: A Modern Guide for Local Mortgage Pros Left Behind by the Digital CustomerFrom EverandBypassed: A Modern Guide for Local Mortgage Pros Left Behind by the Digital CustomerNo ratings yet

- House Poor: How to Buy and Sell Your Home Come Bubble or BustFrom EverandHouse Poor: How to Buy and Sell Your Home Come Bubble or BustNo ratings yet

- 2024-03 Monthly Housing Market OutlookDocument57 pages2024-03 Monthly Housing Market OutlookC.A.R. Research & EconomicsNo ratings yet

- 2024-02 Monthly Housing Market OutlookDocument57 pages2024-02 Monthly Housing Market OutlookC.A.R. Research & Economics100% (1)

- Traditional HAI PresentationDocument9 pagesTraditional HAI PresentationC.A.R. Research & EconomicsNo ratings yet

- 2023-12 Monthly Housing Market OutlookDocument57 pages2023-12 Monthly Housing Market OutlookC.A.R. Research & Economics100% (1)

- 2023-01 Monthly Housing Market OutlookDocument57 pages2023-01 Monthly Housing Market OutlookC.A.R. Research & Economics100% (1)

- 2023-Q1 Traditional Housing Affordability Index (HAI)Document9 pages2023-Q1 Traditional Housing Affordability Index (HAI)C.A.R. Research & EconomicsNo ratings yet

- 2022 AHMS ReportDocument51 pages2022 AHMS ReportC.A.R. Research & Economics100% (1)

- 2024-02 Monthly Housing Market OutlookDocument57 pages2024-02 Monthly Housing Market OutlookC.A.R. Research & Economics100% (1)

- 2023-12 Monthly Housing Market OutlookDocument57 pages2023-12 Monthly Housing Market OutlookC.A.R. Research & Economics100% (1)

- 2023-11 Monthly Housing Market OutlookDocument57 pages2023-11 Monthly Housing Market OutlookC.A.R. Research & Economics100% (1)

- Monthly Housing Market OutlookDocument57 pagesMonthly Housing Market OutlookC.A.R. Research & EconomicsNo ratings yet

- Traditional HAI PresentationDocument9 pagesTraditional HAI PresentationC.A.R. Research & EconomicsNo ratings yet

- Traditional HAI PresentationDocument9 pagesTraditional HAI PresentationC.A.R. Research & EconomicsNo ratings yet

- 2023-03 Monthly Housing Market OutlookDocument57 pages2023-03 Monthly Housing Market OutlookC.A.R. Research & Economics100% (1)

- 2023-05 Monthly Housing Market OutlookDocument57 pages2023-05 Monthly Housing Market OutlookC.A.R. Research & EconomicsNo ratings yet

- 2022-11 Monthly Housing Market OutlookDocument57 pages2022-11 Monthly Housing Market OutlookC.A.R. Research & EconomicsNo ratings yet

- Traditional HAI PresentationDocument9 pagesTraditional HAI PresentationC.A.R. Research & EconomicsNo ratings yet

- 2022-12 Monthly Housing Market OutlookDocument58 pages2022-12 Monthly Housing Market OutlookC.A.R. Research & Economics100% (1)

- 2022-10 Monthly Housing Market OutlookDocument57 pages2022-10 Monthly Housing Market OutlookC.A.R. Research & Economics100% (1)

- Traditional HAI PresentationDocument9 pagesTraditional HAI PresentationC.A.R. Research & EconomicsNo ratings yet

- 2022-07 Monthly Housing Market OutlookDocument57 pages2022-07 Monthly Housing Market OutlookC.A.R. Research & EconomicsNo ratings yet

- 2022-09 Monthly Housing Market OutlookDocument57 pages2022-09 Monthly Housing Market OutlookC.A.R. Research & Economics100% (1)

- 2022-06 Monthly Housing Market OutlookDocument57 pages2022-06 Monthly Housing Market OutlookC.A.R. Research & Economics100% (1)

- 2022-08 Monthly Housing Market OutlookDocument57 pages2022-08 Monthly Housing Market OutlookC.A.R. Research & Economics100% (1)

- California Housing Affordability UpdateDocument9 pagesCalifornia Housing Affordability UpdateC.A.R. Research & EconomicsNo ratings yet

- 2022-04 Monthly Housing Market OutlookDocument9 pages2022-04 Monthly Housing Market OutlookC.A.R. Research & EconomicsNo ratings yet

- 2022-05 Monthly Housing Market OutlookDocument56 pages2022-05 Monthly Housing Market OutlookC.A.R. Research & Economics100% (1)

- 2022-04 Monthly Housing Market OutlookDocument56 pages2022-04 Monthly Housing Market OutlookC.A.R. Research & EconomicsNo ratings yet

- 2022-02 Monthly Housing Market OutlookDocument55 pages2022-02 Monthly Housing Market OutlookC.A.R. Research & Economics100% (1)

- 2022-03 Monthly Housing Market OutlookDocument55 pages2022-03 Monthly Housing Market OutlookC.A.R. Research & Economics100% (2)

- Nirbhaya High Court JudgementDocument340 pagesNirbhaya High Court Judgementravikantsv100% (4)

- Town Hall Fund Trustees Win Suit to Recover SubscriptionDocument2 pagesTown Hall Fund Trustees Win Suit to Recover SubscriptionutkarshNo ratings yet

- Tristar Case Sol.Document4 pagesTristar Case Sol.Niketa JaiswalNo ratings yet

- Should Pixar Get Acquired by DisneyDocument9 pagesShould Pixar Get Acquired by DisneyAmbrish ChaudharyNo ratings yet

- TOS Quiz 4Document6 pagesTOS Quiz 4maria ronoraNo ratings yet

- SSC c11016 For Exam Shortlisted-10 - XLSXDocument13 pagesSSC c11016 For Exam Shortlisted-10 - XLSXpikumarNo ratings yet

- Security Management - Hse Level 3Document16 pagesSecurity Management - Hse Level 3Emmanuel AdenolaNo ratings yet

- Sacramento Kings 2018-19 Schedule GuideDocument1 pageSacramento Kings 2018-19 Schedule GuideMelchor BalolongNo ratings yet

- Rent A Bike For Life - UPLB CHE SCDocument5 pagesRent A Bike For Life - UPLB CHE SCAura Carla TolentinoNo ratings yet

- MUN HandbookDocument52 pagesMUN HandbookSyasya SyahieraNo ratings yet

- Media and Information Literacy DLPDocument2 pagesMedia and Information Literacy DLPMike John MaximoNo ratings yet

- Bank Management: Dr. Rania Salem Department of FinanceDocument22 pagesBank Management: Dr. Rania Salem Department of FinanceDoha KashNo ratings yet

- Tracer Study Proposal 2020Document6 pagesTracer Study Proposal 2020Charlene PadillaNo ratings yet

- KADI JOKES: Collection of Popular Tamil "AruvaiDocument13 pagesKADI JOKES: Collection of Popular Tamil "Aruvaiarni tkdcsNo ratings yet

- IESCO GST No. bill provides Say No To Corruption detailsDocument2 pagesIESCO GST No. bill provides Say No To Corruption detailsUmer SarfarazNo ratings yet

- Enager Industries3Document5 pagesEnager Industries3pratheek30100% (1)

- Archaeological Discoveries at LumbiniDocument3 pagesArchaeological Discoveries at LumbiniJagganath VishwamitraNo ratings yet

- Presidential Powers ExplainedDocument3 pagesPresidential Powers ExplainedDragoşCosminRăduţăNo ratings yet

- (1997) 1 SLR (R) 0681Document18 pages(1997) 1 SLR (R) 0681Sulaiman CheliosNo ratings yet

- Personal History Statement Instructions: ConfidentialDocument8 pagesPersonal History Statement Instructions: ConfidentialcgacNo ratings yet

- Marketing Principles 551 v2 PDFDocument606 pagesMarketing Principles 551 v2 PDFMandal Sagar0% (1)

- What is damages and liquidated damages in a contract? (38Document4 pagesWhat is damages and liquidated damages in a contract? (38VK GOWDANo ratings yet

- A Study On Leadership Styles and Coporate Culture Preferences in Ongc, RajahmundryDocument91 pagesA Study On Leadership Styles and Coporate Culture Preferences in Ongc, RajahmundrySUDEEP KUMAR100% (4)

- 六年级修辞01 Worksheet CroppedDocument5 pages六年级修辞01 Worksheet CroppedI am BearNo ratings yet

- 10 Famous Filipino WritersDocument11 pages10 Famous Filipino Writersmichael segundo100% (3)

- Linguistic imperialism's negative impactsDocument2 pagesLinguistic imperialism's negative impactsVero Scharff100% (3)

- Lesson 07 - Deriving The Laws IIIDocument11 pagesLesson 07 - Deriving The Laws IIIMilan KokowiczNo ratings yet

- Pin Heidy. Prepositions of Time in On at 2Document1 pagePin Heidy. Prepositions of Time in On at 2Heidy PinNo ratings yet

- Central Surety vs. C.N HodgesDocument11 pagesCentral Surety vs. C.N HodgesMirzi Olga Breech SilangNo ratings yet

- IfrsDocument17 pagesIfrsMiracle VerteraNo ratings yet