You might also like

- Scrum MasterDocument19 pagesScrum MasterDaniel Martinez100% (2)

- Safal Niveshak Mastermind BrochureDocument3 pagesSafal Niveshak Mastermind BrochureNaveen K. JindalNo ratings yet

- Northern Star Resources LTD: More +KG/T Intercepts Into Voyager Lodes, PaulsensDocument6 pagesNorthern Star Resources LTD: More +KG/T Intercepts Into Voyager Lodes, Paulsenschrisb700No ratings yet

- Pro-Forma Balance SheetDocument3 pagesPro-Forma Balance Sheetoxfordentrepreneur0% (2)

- Barrick Gold 2009 Annual ReportDocument170 pagesBarrick Gold 2009 Annual ReportBarrickGoldNo ratings yet

- Indonesia Salary Guide Ebook PDFDocument22 pagesIndonesia Salary Guide Ebook PDFteguh_setiono100% (2)

- Royal Bank of CanadaDocument18 pagesRoyal Bank of CanadaShruti VinyasNo ratings yet

- Business Plan Easy VapeDocument24 pagesBusiness Plan Easy VapeCharlie HolmesNo ratings yet

- Strategic Alliance Process & ManagementDocument87 pagesStrategic Alliance Process & ManagementPratiksha Shekhar Bhadrige100% (1)

- Comparative Study Between Private Sector Banks and Public Sector BanksDocument61 pagesComparative Study Between Private Sector Banks and Public Sector BanksJitendra Kumar68% (40)

- Soal Latihan Cash Flow Fix Dan JawabanDocument6 pagesSoal Latihan Cash Flow Fix Dan JawabanInggil Subhan100% (1)

- Debenhams Analyst ReportDocument108 pagesDebenhams Analyst ReportFisher Black75% (4)

- By All Means Necessary - How China's Resource Quest Is Changing The World - Elizabeth Economy and Micha Levi - ByAllMeaNecHowChiResQueIsChaTheWor PDFDocument298 pagesBy All Means Necessary - How China's Resource Quest Is Changing The World - Elizabeth Economy and Micha Levi - ByAllMeaNecHowChiResQueIsChaTheWor PDFbastisnNo ratings yet

- KCI Kendilo Coal Indonesia ProfileDocument1 pageKCI Kendilo Coal Indonesia Profilegbh_suryoNo ratings yet

- News Release: Newmont Updates 5-Year Business Plan - 2003 Gold Reserves in Ghana Expected To Reach 10 Million OuncesDocument12 pagesNews Release: Newmont Updates 5-Year Business Plan - 2003 Gold Reserves in Ghana Expected To Reach 10 Million OuncescobbymarkNo ratings yet

- Yamana Gold Announces Record Q4 and Full Year 2014 ResultsDocument35 pagesYamana Gold Announces Record Q4 and Full Year 2014 ResultsJavier Montecinos MalebranNo ratings yet

- Falco Announces Positive Preliminary Economic Assessment for Quebec Gold ProjectDocument12 pagesFalco Announces Positive Preliminary Economic Assessment for Quebec Gold ProjectrosaliaNo ratings yet

- Leading Gold Company ReportDocument100 pagesLeading Gold Company ReportDavid RvNo ratings yet

- ACACIA-Results For The 3 Months Ended 31 March 2019 - FINAL (1) - 1Document22 pagesACACIA-Results For The 3 Months Ended 31 March 2019 - FINAL (1) - 1Baraka LetaraNo ratings yet

- Dynatronics CaseDocument6 pagesDynatronics CaseScribdTranslationsNo ratings yet

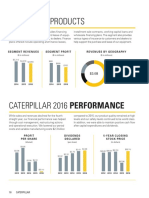

- Pages From 2016 Cat Ar-5Document1 pagePages From 2016 Cat Ar-5EngTamerNo ratings yet

- 2017 Annual Report Final e Sig PDFDocument186 pages2017 Annual Report Final e Sig PDFKristen CollierNo ratings yet

- Kinross Reports 2013 First-Quarter ResultsDocument15 pagesKinross Reports 2013 First-Quarter ResultsRicky Martin MartinNo ratings yet

- Tag - 12152010 - WWDocument7 pagesTag - 12152010 - WWJPCrandorNo ratings yet

- Energold Drilling - Investor PresentationDocument23 pagesEnergold Drilling - Investor PresentationkaiselkNo ratings yet

- 2016ye LuccpDocument32 pages2016ye LuccpkaiselkNo ratings yet

- 2019 LEPANTO FINAL PDF FILE - CompressedDocument90 pages2019 LEPANTO FINAL PDF FILE - CompressedMIGUEL BUENAVENTURA VIRAYNo ratings yet

- Fortuna Reports Consolidated Financial Results For The Second Quarter 2014Document6 pagesFortuna Reports Consolidated Financial Results For The Second Quarter 2014revistaproactivoNo ratings yet

- PT Merdeka Copper Gold TBK: Q3 2021 UpdateDocument37 pagesPT Merdeka Copper Gold TBK: Q3 2021 UpdateRichard nicoNo ratings yet

- Action Notes: Rating/Target/Estimate ChangesDocument23 pagesAction Notes: Rating/Target/Estimate ChangesJeff SharpNo ratings yet

- OceanaGold Corp Dec 2009Document5 pagesOceanaGold Corp Dec 2009O B Research83% (6)

- K CaseDocument11 pagesK CaseHenni RahmanNo ratings yet

- Financial Management Project The Super Project: Submitted ToDocument10 pagesFinancial Management Project The Super Project: Submitted ToShreya SrivastavaNo ratings yet

- 2012 Corporate Update JanuaryDocument33 pages2012 Corporate Update JanuaryWilson Marcelo MurilloNo ratings yet

- Why Did Bulong DefaultDocument10 pagesWhy Did Bulong DefaultHuy Quang ĐỗNo ratings yet

- Citigold Mar QTR 09Document2 pagesCitigold Mar QTR 09rafishNo ratings yet

- MineralIndustryStatistics MGB Feb2013Document1 pageMineralIndustryStatistics MGB Feb2013jfmanNo ratings yet

- BP Amoco BP Amoco 1997 1997 1997 1998Document4 pagesBP Amoco BP Amoco 1997 1997 1997 1998Raj SharmaNo ratings yet

- Freeport-Mcmoran Reports Third-Quarter and Nine-Month 2020 ResultsDocument37 pagesFreeport-Mcmoran Reports Third-Quarter and Nine-Month 2020 ResultsDayu adisaputraNo ratings yet

- Hudbay Announces Updated Constancia ReportDocument11 pagesHudbay Announces Updated Constancia Reportismael machacaNo ratings yet

- #GIR Investor Executive Summary V6-2018Document5 pages#GIR Investor Executive Summary V6-2018Neil GutierrezNo ratings yet

- Salient Features May Week 2 Fy2023Document1 pageSalient Features May Week 2 Fy2023Mike ChiguwareNo ratings yet

- Anderson Energy Announces 2010 Second Quarter Results: HighlightsDocument37 pagesAnderson Energy Announces 2010 Second Quarter Results: Highlightsikehenderson4879No ratings yet

- FCL1102 NDocument6 pagesFCL1102 NJeremy SussmanNo ratings yet

- Metorex Int Dec07Document12 pagesMetorex Int Dec07Take OneNo ratings yet

- Q2 2017 Financial & Operating Results: Friday, July 28, 2017Document36 pagesQ2 2017 Financial & Operating Results: Friday, July 28, 2017kaiselkNo ratings yet

- Mine Valuation of A Typical Gold Deposit: Technical ParametersDocument8 pagesMine Valuation of A Typical Gold Deposit: Technical ParametersGwen Ibarra SuaybaguioNo ratings yet

- GOLD MINE VALUATION KEY PARAMETERSDocument8 pagesGOLD MINE VALUATION KEY PARAMETERSGwen Ibarra SuaybaguioNo ratings yet

- Lease Examples October 09Document1 pageLease Examples October 09panda910No ratings yet

- SilverCrest Announces Positive Feasibility Study Results for Las Chispas ProjectDocument10 pagesSilverCrest Announces Positive Feasibility Study Results for Las Chispas ProjectMahdi Tukang BatuNo ratings yet

- American Cheminal Corp SpreadsheetDocument16 pagesAmerican Cheminal Corp SpreadsheetRahul PandeyNo ratings yet

- Gold & Silver Rates As On 01.04.1981 & From 31.03.2011 - Taxguru - inDocument4 pagesGold & Silver Rates As On 01.04.1981 & From 31.03.2011 - Taxguru - inDevenderNo ratings yet

- Lun 150729 CandelariaDocument2 pagesLun 150729 CandelariaEMMANUEL DIEGO MARTINEZ SOZANo ratings yet

- Dynamically Positioned Annual Report HighlightsDocument158 pagesDynamically Positioned Annual Report HighlightsMike MaguireNo ratings yet

- Contango Oil & Gas Co. PresentationDocument18 pagesContango Oil & Gas Co. PresentationCale SmithNo ratings yet

- UK Subsidiary Translation MethodsDocument2 pagesUK Subsidiary Translation MethodsBhagyeshGhagiNo ratings yet

- Centamin PLC Results For The Year Ended 31 December 2017 and Full Year Dividend DeclarationDocument69 pagesCentamin PLC Results For The Year Ended 31 December 2017 and Full Year Dividend DeclarationSudhit SethiNo ratings yet

- FrancoNevada Annual Report 2021Document100 pagesFrancoNevada Annual Report 2021wigidas889No ratings yet

- OCC's Quarterly Report On Bank Trading and Derivatives Activities Second Quarter 2009Document33 pagesOCC's Quarterly Report On Bank Trading and Derivatives Activities Second Quarter 2009qtipxNo ratings yet

- OCC's Quarterly Report On Bank Trading and Derivatives Activities Second Quarter 2009Document33 pagesOCC's Quarterly Report On Bank Trading and Derivatives Activities Second Quarter 2009Nathan MartinNo ratings yet

- Disclosure DocDocument3 pagesDisclosure DocgekkoNo ratings yet

- Gammon Gold Sept 2010 PresentationDocument45 pagesGammon Gold Sept 2010 PresentationAla BasterNo ratings yet

- Designed To: 2009 Annual ReportDocument78 pagesDesigned To: 2009 Annual ReportAsif HaiderNo ratings yet

- Archipelago SummaryDocument1 pageArchipelago SummaryixanoziousNo ratings yet

- Real Life. Real Answers.: NaborDocument4 pagesReal Life. Real Answers.: Naborapi-26167871No ratings yet

- Operating Exposure (Or Chapter 9)Document19 pagesOperating Exposure (Or Chapter 9)sindhupallavigundaNo ratings yet

- Strong Buy Recommendation for Undervalued Gold Miner NWGC Trading at Just $0.10 per ShareDocument9 pagesStrong Buy Recommendation for Undervalued Gold Miner NWGC Trading at Just $0.10 per SharejrswitzerNo ratings yet

- Cut Stone & Stone Products World Summary: Market Values & Financials by CountryFrom EverandCut Stone & Stone Products World Summary: Market Values & Financials by CountryNo ratings yet

- Silverware & Platedware World Summary: Market Values & Financials by CountryFrom EverandSilverware & Platedware World Summary: Market Values & Financials by CountryNo ratings yet

- Crushed & Broken Stone Products World Summary: Market Values & Financials by CountryFrom EverandCrushed & Broken Stone Products World Summary: Market Values & Financials by CountryNo ratings yet

- Silicon Carbide Solid & Grains & Powders & Flour Abrasives World Summary: Market Sector Values & Financials by CountryFrom EverandSilicon Carbide Solid & Grains & Powders & Flour Abrasives World Summary: Market Sector Values & Financials by CountryNo ratings yet

- RI Coal Data Collection System 2013 ESDMDocument12 pagesRI Coal Data Collection System 2013 ESDMgbh_suryoNo ratings yet

- CooperativeDocument14 pagesCooperativeSiddhartha NeogNo ratings yet

- Global Mining Trend June 2014 PWCDocument52 pagesGlobal Mining Trend June 2014 PWCgbh_suryoNo ratings yet

- RI 50 WKP Geothermal Location List 2013Document2 pagesRI 50 WKP Geothermal Location List 2013gbh_suryoNo ratings yet

- Metallurgical CoalTrans Conference April 2012 BHPDocument28 pagesMetallurgical CoalTrans Conference April 2012 BHPgbh_suryoNo ratings yet

- Antofagasta February 2012 IRDocument43 pagesAntofagasta February 2012 IRgbh_suryoNo ratings yet

- Syrian Phosphate Project ASHGILLDocument8 pagesSyrian Phosphate Project ASHGILLgbh_suryoNo ratings yet

- Steel Raw Materials FocusDocument27 pagesSteel Raw Materials Focusgbh_suryoNo ratings yet

- Kba C. Guide English PDFDocument17 pagesKba C. Guide English PDFfelixmuyoveNo ratings yet

- Fraud Investigation & Dispute Services Regulatory ComplianceDocument4 pagesFraud Investigation & Dispute Services Regulatory ComplianceJanaelaNo ratings yet

- This Study Resource WasDocument6 pagesThis Study Resource WasKurtNo ratings yet

- Askari Bank Test PatternDocument4 pagesAskari Bank Test PatternM. Umair Choudhry63% (8)

- 1 Annex I. Imprimatur Investment Agreement: Example Offer Letter, Key Terms and Outline ProcessDocument5 pages1 Annex I. Imprimatur Investment Agreement: Example Offer Letter, Key Terms and Outline ProcessAfandie Van WhyNo ratings yet

- US Internal Revenue Service: p938 - 2002Document160 pagesUS Internal Revenue Service: p938 - 2002IRSNo ratings yet

- Bank Al Habib Effective AssignmentDocument35 pagesBank Al Habib Effective AssignmentAhmed Jan DahriNo ratings yet

- Uploads Presentations 102 Mr. Lakshminarayana K RDocument12 pagesUploads Presentations 102 Mr. Lakshminarayana K RNaveen ThakurNo ratings yet

- FINALS - Practical Accounting 2Document4 pagesFINALS - Practical Accounting 2Angela Viernes100% (2)

- A Study On Performance Evaluation of Mutual FundsDocument12 pagesA Study On Performance Evaluation of Mutual FundsBinayKPNo ratings yet

- Debenture TrusteeDocument6 pagesDebenture TrusteeRajesh GoelNo ratings yet

- S.R. Batliboi Co - LLP Campus Slides - FinalDocument17 pagesS.R. Batliboi Co - LLP Campus Slides - FinalRiaan JoshiahNo ratings yet

- Edmonton Property Value Assessments 2016Document2 pagesEdmonton Property Value Assessments 2016Anonymous QRCBjQd5I7No ratings yet

- T.B - CH09Document17 pagesT.B - CH09MohammadYaqoobNo ratings yet

- Role of Financial IntermediariesDocument8 pagesRole of Financial Intermediariesashwini.krs80No ratings yet

- FDsetia 20150923pj8xfnDocument41 pagesFDsetia 20150923pj8xfnJames WarrenNo ratings yet

- Apollo Munich Health Insurance Company Management ProfileDocument5 pagesApollo Munich Health Insurance Company Management ProfileAman Bhatia : SR. SEO in Apollo Munich Health Insurance CompanyNo ratings yet

- SEC v. Imran Husain Et Al Doc 33 Filed 22 Nov 16Document61 pagesSEC v. Imran Husain Et Al Doc 33 Filed 22 Nov 16scion.scionNo ratings yet

- Tata-Digital-India-Fun0 2222233333333Document42 pagesTata-Digital-India-Fun0 2222233333333yasirNo ratings yet

- Gross IncomeDocument21 pagesGross IncomeALYANNAH HAROUNNo ratings yet

- Provide A Brief Overview of The Firms and Industry Sector. Rex Industry BerhadDocument4 pagesProvide A Brief Overview of The Firms and Industry Sector. Rex Industry Berhadainmazni5No ratings yet