You might also like

- KV OEF Library NewsletterDocument4 pagesKV OEF Library NewsletterRakesh Kumar PandeyNo ratings yet

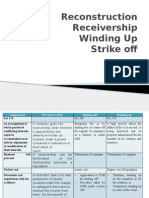

- Reconstruction Receivership Winding Up Strike OffDocument71 pagesReconstruction Receivership Winding Up Strike OffMohammad Hasrul AkmalNo ratings yet

- BFW 3331 T6 AnswersDocument6 pagesBFW 3331 T6 AnswersDylanchong91No ratings yet

- Interest Rate ParityDocument5 pagesInterest Rate Parityrosario correiaNo ratings yet

- TANGAZO LA NAFASI ZA KAZI eGA, TBA & KADCO PDFDocument23 pagesTANGAZO LA NAFASI ZA KAZI eGA, TBA & KADCO PDFEmanuel John BangoNo ratings yet

- Assignment Enron & Worldcom - FinalDocument3 pagesAssignment Enron & Worldcom - FinalMD FAISALNo ratings yet

- Venture Capital FinanceDocument7 pagesVenture Capital FinanceSachi LunechiyaNo ratings yet

- International Finance Group 2Document8 pagesInternational Finance Group 2Abdallah SadikiNo ratings yet

- Assignment FINM7406Document4 pagesAssignment FINM7406TaufikTaoNo ratings yet

- Environmental Financial ReportingDocument8 pagesEnvironmental Financial Reportingnhoccon22No ratings yet

- Analysis of Financial Statements PDFDocument14 pagesAnalysis of Financial Statements PDFMuhammad Akmal HossainNo ratings yet

- Int'l Training College assignment on investment proposal returnsDocument3 pagesInt'l Training College assignment on investment proposal returnsWilliam MushongaNo ratings yet

- DebitCreditAnalysisComparesAccountsYear"TITLE "CashflowStatementAnalyzesPrimeSportsGearCashFlows2013" TITLE "RatioAnalysisComparesGlobalTechFinancialsSalesProfit201213Document7 pagesDebitCreditAnalysisComparesAccountsYear"TITLE "CashflowStatementAnalyzesPrimeSportsGearCashFlows2013" TITLE "RatioAnalysisComparesGlobalTechFinancialsSalesProfit201213shineneigh00No ratings yet

- The Foreign Exchange Market and International Parity ConditionsDocument19 pagesThe Foreign Exchange Market and International Parity ConditionsMarcia PattersonNo ratings yet

- MARKING KEY: ASSIGNMENT 1 ON FINANCIAL MANAGEMENT 2 MODULEDocument3 pagesMARKING KEY: ASSIGNMENT 1 ON FINANCIAL MANAGEMENT 2 MODULEWilliam MushongaNo ratings yet

- Problem Questions Solutions PDFDocument4 pagesProblem Questions Solutions PDFdeepanshi jainNo ratings yet

- Accounting and FinanceDocument2 pagesAccounting and FinanceHabte DebeleNo ratings yet

- CH 9 Flexible Budgets CompressedDocument36 pagesCH 9 Flexible Budgets Compressedmuhammad fathoniNo ratings yet

- Day 1Document11 pagesDay 1Abdullah EjazNo ratings yet

- Case Study On Demand and Supply (By Archit Kalani)Document11 pagesCase Study On Demand and Supply (By Archit Kalani)Archit KalaniNo ratings yet

- Chap 17Document34 pagesChap 17ridaNo ratings yet

- Practice Test MidtermDocument6 pagesPractice Test Midtermrjhuff41No ratings yet

- STCBL Financial AnalysisDocument33 pagesSTCBL Financial AnalysisSonam K Gyamtsho67% (3)

- Accounting of Ijarah ContractsDocument53 pagesAccounting of Ijarah ContractsShaikhaAlnoaimiNo ratings yet

- Solvay Adv Acc Case 6 Wapiti Group ConsolidationDocument24 pagesSolvay Adv Acc Case 6 Wapiti Group ConsolidationlolaNo ratings yet

- RatioDocument24 pagesRatioSadika KhanNo ratings yet

- AUD610 Advanced Auditing (Handouts March 2016)Document202 pagesAUD610 Advanced Auditing (Handouts March 2016)ewinze100% (1)

- Week 1 Conceptual Framework For Financial ReportingDocument17 pagesWeek 1 Conceptual Framework For Financial ReportingSHANE NAVARRONo ratings yet

- Chapter - 5 Long Term FinancingDocument6 pagesChapter - 5 Long Term FinancingmuzgunniNo ratings yet

- NBS Non Performing LoansDocument28 pagesNBS Non Performing LoansGreg ZuccariniNo ratings yet

- Financial Reporting Standards for IFRS ComplianceDocument35 pagesFinancial Reporting Standards for IFRS ComplianceLetsah BrightNo ratings yet

- A401 - 02 - Fall 2016Document6 pagesA401 - 02 - Fall 2016Josh ChangNo ratings yet

- Macroeconomy - Understanding key concepts of open economiesDocument9 pagesMacroeconomy - Understanding key concepts of open economiesmarcjeansNo ratings yet

- Forward Rate AgreementDocument8 pagesForward Rate AgreementNaveen BhatiaNo ratings yet

- Paper Chapter 12 Group 1Document17 pagesPaper Chapter 12 Group 1Nadiani Nana100% (1)

- Merit Enterprise Corp's $4B Expansion OptionsDocument3 pagesMerit Enterprise Corp's $4B Expansion OptionsEufemia MabingnayNo ratings yet

- Impact of Government Policy and Regulations in BankingDocument65 pagesImpact of Government Policy and Regulations in BankingNiraj ThapaNo ratings yet

- Apv PDFDocument10 pagesApv PDFSam Sep A SixtyoneNo ratings yet

- Accounting GuessDocument5 pagesAccounting GuessjhouvanNo ratings yet

- MG 204 Mid Semester Exam Solutions Sem 1 2017Document5 pagesMG 204 Mid Semester Exam Solutions Sem 1 2017Nileshni DeviNo ratings yet

- Johnny FinalDocument4 pagesJohnny FinalNikita SharmaNo ratings yet

- Pe04c AnswersDocument3 pagesPe04c AnswersMarian Emmanuelle CristobalNo ratings yet

- The Effects of Management Buyouts On Operating Per PDFDocument38 pagesThe Effects of Management Buyouts On Operating Per PDFASbinance ASbinanceNo ratings yet

- FinAcc Vol. 3 Chap3 ProblemsDocument26 pagesFinAcc Vol. 3 Chap3 ProblemsGelynne Arceo33% (3)

- Quantitative Analysis Sectional TestDocument11 pagesQuantitative Analysis Sectional Testgeeths207No ratings yet

- Financial Statement AnalysisDocument50 pagesFinancial Statement AnalysisRishin Suresh S100% (1)

- The Role of Finacial ManagementDocument25 pagesThe Role of Finacial Managementnitinvohra_capricorn100% (1)

- Trade Me analysis reveals stock valuationDocument20 pagesTrade Me analysis reveals stock valuationCindy YinNo ratings yet

- Financial Statements in The Public Sector PDFDocument15 pagesFinancial Statements in The Public Sector PDFMr DamphaNo ratings yet

- Dallas Police Fire Pension InvestmentsDocument22 pagesDallas Police Fire Pension InvestmentsRobert WilonskyNo ratings yet

- Overview of Financial ManagementDocument187 pagesOverview of Financial ManagementashrawNo ratings yet

- Strategic Management - Midterm Quiz 1Document6 pagesStrategic Management - Midterm Quiz 1Uy SamuelNo ratings yet

- Dell Annual ReportDocument55 pagesDell Annual ReportOmotoso EstherNo ratings yet

- Hotel Management System Project for FM International HotelDocument18 pagesHotel Management System Project for FM International Hotelmamaru bantieNo ratings yet

- IAS 20 Accounting for Government GrantsDocument19 pagesIAS 20 Accounting for Government GrantsGail Bermudez100% (1)

- Discounted Cash Flow (DCF) Definition - InvestopediaDocument2 pagesDiscounted Cash Flow (DCF) Definition - Investopedianaviprasadthebond9532No ratings yet

- Full Deposition of Shellie Hill of Lerner, Sampson & RothfussDocument50 pagesFull Deposition of Shellie Hill of Lerner, Sampson & RothfussForeclosure FraudNo ratings yet

- Generally Accepted Auditing Standards A Complete Guide - 2020 EditionFrom EverandGenerally Accepted Auditing Standards A Complete Guide - 2020 EditionNo ratings yet

- Reg. No.Document4 pagesReg. No.madhumithaNo ratings yet

- CBM 514-3 Question 3Document3 pagesCBM 514-3 Question 3hafsamohmd793No ratings yet

- Interpretation of Financial Statements - IntroductionDocument19 pagesInterpretation of Financial Statements - Introductionsazid9No ratings yet

- Stock Exchange VolatilityDocument104 pagesStock Exchange VolatilityDenis Robert MfugaleNo ratings yet

- Proposal Tax Payer EducationDocument22 pagesProposal Tax Payer EducationDenis Robert Mfugale100% (1)

- Ch5 - Financial Statement AnalysisDocument39 pagesCh5 - Financial Statement AnalysisLaura TurbatuNo ratings yet

- Finscope Tanzania Survey On Banking Industry 2006Document132 pagesFinscope Tanzania Survey On Banking Industry 2006Denis Robert MfugaleNo ratings yet

- Mid Semester Test - 2Document1 pageMid Semester Test - 2Denis Robert MfugaleNo ratings yet

- CasesDocument34 pagesCasesSaket KumarNo ratings yet

- Troubles of LakshmiDocument7 pagesTroubles of LakshmiDebolina DeyNo ratings yet

- BFS ProjectDocument18 pagesBFS ProjectStefenny PanggadewiNo ratings yet

- FV FV: ExplanationDocument54 pagesFV FV: Explanationenergizerabby83% (6)

- A View About The Determinants of Change in Share Prices A Case From Karachi Stock Exchange (Banking)Document17 pagesA View About The Determinants of Change in Share Prices A Case From Karachi Stock Exchange (Banking)(FPTU HCM) Phạm Anh Thiện TùngNo ratings yet

- Valuation For StartupsDocument39 pagesValuation For StartupsrabiadzNo ratings yet

- FinQuiz - CFA Level 3, June, 2017 - Study PlanDocument3 pagesFinQuiz - CFA Level 3, June, 2017 - Study PlanTaha OwaisNo ratings yet

- ISB Consulting Casebook 2013 - FinalDocument86 pagesISB Consulting Casebook 2013 - FinalANo ratings yet

- ABIR's International (Re) Insurers' Global Underwriting ReportDocument2 pagesABIR's International (Re) Insurers' Global Underwriting ReportAnonymous UpWci5100% (1)

- Full Download Fundamentals of Financial Management 12th Edition Brigham Test BankDocument35 pagesFull Download Fundamentals of Financial Management 12th Edition Brigham Test Bankleavings.strix.b9xf100% (49)

- ExamView Pro - DEBT FINANCING - TST PDFDocument15 pagesExamView Pro - DEBT FINANCING - TST PDFShannon ElizaldeNo ratings yet

- House For Sale in Kihali-ManualDocument30 pagesHouse For Sale in Kihali-ManualAmirul WashingtonNo ratings yet

- Eyewear - Ppt-Marketing Report-Term 1Document7 pagesEyewear - Ppt-Marketing Report-Term 1Turner TuringNo ratings yet

- 11 03 2019 - Embassy REIT Offer Document (Optimized) PDFDocument675 pages11 03 2019 - Embassy REIT Offer Document (Optimized) PDFSubash Nehru. SNo ratings yet

- Fama and French:: Three Factor ModelDocument17 pagesFama and French:: Three Factor ModelMahmudy Putera ArsenalNo ratings yet

- Cairns India Private LimitedDocument25 pagesCairns India Private LimitedSuruchi GoyalNo ratings yet

- IAS 38 - SolutionDocument2 pagesIAS 38 - SolutionNguyễn PhươngNo ratings yet

- Apuntes Business ManagementDocument7 pagesApuntes Business ManagementSara Callado CarbonellNo ratings yet

- Reversal Patterns: Part 1Document16 pagesReversal Patterns: Part 1Oxford Capital Strategies LtdNo ratings yet

- Project On Mutual FundDocument95 pagesProject On Mutual FundMadhusudana p nNo ratings yet

- 142a Banknifty Weekly Options StrategyDocument6 pages142a Banknifty Weekly Options StrategyudayNo ratings yet

- Operational Research Assignment............ (Ca Final Cost and Or)Document87 pagesOperational Research Assignment............ (Ca Final Cost and Or)Pravinn_Mahajan80% (5)

- 04 .All About Int Rates, Zero RatesDocument87 pages04 .All About Int Rates, Zero RatesHarshit DwivediNo ratings yet

- Balance Sheet of Canara BankDocument17 pagesBalance Sheet of Canara BankSathish KumarNo ratings yet

- Sampa Video Inc.: Thousand of Dollars Exhibit 4Document2 pagesSampa Video Inc.: Thousand of Dollars Exhibit 4nimarNo ratings yet

- Questionnaire For Financial Advosory SurveyDocument2 pagesQuestionnaire For Financial Advosory SurveyharishmnNo ratings yet

- 07 Valuing Early-Stage BusinessesDocument8 pages07 Valuing Early-Stage Businessesmaghanna88No ratings yet

- 5.1 Basic Methods For Eng'g Eco StudyDocument16 pages5.1 Basic Methods For Eng'g Eco StudyVinceNo ratings yet

- Prudential Norms For Non-Banking Financial (Non-Deposit Accepting or Holding) CompaniesDocument6 pagesPrudential Norms For Non-Banking Financial (Non-Deposit Accepting or Holding) CompaniesGreeshma Babu ShylajaNo ratings yet