You might also like

- Human Rights: Previous Year's MCQs of Tripura University and Answers with Short ExplanationsFrom EverandHuman Rights: Previous Year's MCQs of Tripura University and Answers with Short ExplanationsNo ratings yet

- History of Life Insurance in IndiaDocument4 pagesHistory of Life Insurance in IndiaGanesh DadgeNo ratings yet

- AMU Kerala Centre Life Insurance Project ReportDocument12 pagesAMU Kerala Centre Life Insurance Project ReportSadhvi SinghNo ratings yet

- Chapter 1-What Is Insurance?Document20 pagesChapter 1-What Is Insurance?Akshada Chitnis100% (2)

- IRDA Act SummaryDocument67 pagesIRDA Act SummaryVirendra JhaNo ratings yet

- Nationalisation of Insurance BusinessDocument12 pagesNationalisation of Insurance BusinessSanjay Ram Diwakar50% (2)

- Role & Function of IRDADocument2 pagesRole & Function of IRDAadityavik67% (6)

- INSURANCE LAW IN INDIADocument44 pagesINSURANCE LAW IN INDIAVaibhav AhujaNo ratings yet

- Assignment and Nomination Under Insurance PoliciesDocument5 pagesAssignment and Nomination Under Insurance PoliciesNasma AbidiNo ratings yet

- History of Insurance Legislation in IndiaDocument17 pagesHistory of Insurance Legislation in IndiaSagar Bhadrige83% (6)

- Insurance Regulatory Authority Act ExplainedDocument6 pagesInsurance Regulatory Authority Act ExplainedTitus ClementNo ratings yet

- Motor Insurance in India FDDocument16 pagesMotor Insurance in India FDSushil JindalNo ratings yet

- Re Insurance & Double InsuranceDocument36 pagesRe Insurance & Double InsuranceNimish PatankarNo ratings yet

- Importance of Life InsuranceDocument18 pagesImportance of Life InsuranceAsim KunduNo ratings yet

- General Principles of Insurance LawDocument12 pagesGeneral Principles of Insurance LawCarina Amor ClaveriaNo ratings yet

- Banking and Insurance ElementsDocument11 pagesBanking and Insurance ElementsNisarg ShahNo ratings yet

- Insurance, Negotiable Instruments and Banking Assignment: "Insurable Interest"Document19 pagesInsurance, Negotiable Instruments and Banking Assignment: "Insurable Interest"OwaisWarsiNo ratings yet

- Pledge Study NotesDocument3 pagesPledge Study NotesJason MarquezNo ratings yet

- Fire InsuranceDocument9 pagesFire InsuranceNisarg KhamarNo ratings yet

- Settlement of Claim and Payment of MoneyDocument9 pagesSettlement of Claim and Payment of MoneyVarnika TayaNo ratings yet

- Claim Management Life Insurance - DocsDocument3 pagesClaim Management Life Insurance - DocsShubham NamdevNo ratings yet

- Unorganised Workers Social Security ActDocument3 pagesUnorganised Workers Social Security ActnarendrabisoyiNo ratings yet

- Principle of Insurable InterestDocument5 pagesPrinciple of Insurable InterestshreyaNo ratings yet

- Accident InsuranceDocument26 pagesAccident InsuranceNandini JaganNo ratings yet

- Insurance Law in India Question and AnswerDocument15 pagesInsurance Law in India Question and AnswerMaitrayee NandyNo ratings yet

- Privatization of Insurance Sector in IndiaDocument14 pagesPrivatization of Insurance Sector in IndiaProf. R V SinghNo ratings yet

- Gujarat National Law University: Utmost Good FaithDocument26 pagesGujarat National Law University: Utmost Good FaithMeghna SinghNo ratings yet

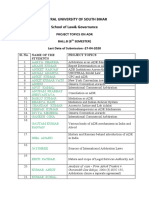

- Central University of South Bihar School of Law& GovernanceDocument4 pagesCentral University of South Bihar School of Law& GovernanceKumar KishanNo ratings yet

- Impact of COVID-19 On Insurance SectorDocument2 pagesImpact of COVID-19 On Insurance SectorMahbubur RahmanNo ratings yet

- Unit 4 Duty of Disclosure Materiality of Facts and MisrepresentationDocument19 pagesUnit 4 Duty of Disclosure Materiality of Facts and MisrepresentationIsrael KalabaNo ratings yet

- Insurance Ombudsman Explained: Key Roles and ResponsibilitiesDocument25 pagesInsurance Ombudsman Explained: Key Roles and ResponsibilitiesParameshwar Bhat NNo ratings yet

- Insurance Law ProjectDocument17 pagesInsurance Law ProjectSukrit GandhiNo ratings yet

- Central University of South Bihar: PROJECT-TOPIC: - "Nature & Scope of Motor Vehicle Insurance"Document20 pagesCentral University of South Bihar: PROJECT-TOPIC: - "Nature & Scope of Motor Vehicle Insurance"DHARAM DEEPAK VISHWASHNo ratings yet

- The Development of Insurance Law: The English & Indian ExperiencesDocument17 pagesThe Development of Insurance Law: The English & Indian ExperiencesTanya RajNo ratings yet

- Comparative study of public & private life insurersDocument9 pagesComparative study of public & private life insurersAamir Sohail KurashiNo ratings yet

- Shrinkhala Jaiswal - Sem VII. InsuranceLawDocument17 pagesShrinkhala Jaiswal - Sem VII. InsuranceLawNaveen MeenaNo ratings yet

- Life InsuranceDocument39 pagesLife Insurancearjunmba11962450% (2)

- Seven principles of insurance including utmost good faith, indemnity and causationDocument8 pagesSeven principles of insurance including utmost good faith, indemnity and causationanilnair88No ratings yet

- Motor InsuranceDocument44 pagesMotor InsuranceAnil Verma57% (7)

- Insurance ProjectDocument16 pagesInsurance ProjectSagrika VidyarthiNo ratings yet

- Utmost Good FaithDocument10 pagesUtmost Good FaithAditya PrakashNo ratings yet

- MortgageDocument8 pagesMortgagePriyanjali BanerjeeNo ratings yet

- INTRODUCTION Insurance ProjectDocument4 pagesINTRODUCTION Insurance ProjectAbhay TiwariNo ratings yet

- IRDA Act ExplainedDocument5 pagesIRDA Act ExplainedSuraj ChandraNo ratings yet

- Banking OmbudsmanDocument6 pagesBanking Ombudsman21813401No ratings yet

- Duty of DisclosureDocument22 pagesDuty of DisclosureRohit SinhaNo ratings yet

- IRDA by The DudesDocument13 pagesIRDA by The DudesAbhimanyu MaheshwariNo ratings yet

- Calculating Motor Accident CompensationDocument3 pagesCalculating Motor Accident Compensation11naqviNo ratings yet

- Class - LL.B (HONS.) II SEM. Subject - Insurance Law: Unit I:IntroductionDocument26 pagesClass - LL.B (HONS.) II SEM. Subject - Insurance Law: Unit I:IntroductionVineet ShahNo ratings yet

- 3rd Party InsuranceDocument13 pages3rd Party InsurancePraveen Rawat100% (2)

- Banking Law: Notes OnDocument134 pagesBanking Law: Notes OnLittz MandumpalaNo ratings yet

- IRDA's Role in Regulating India's Insurance SectorDocument65 pagesIRDA's Role in Regulating India's Insurance SectorMekhala RaoNo ratings yet

- Consumer Protection 1Document12 pagesConsumer Protection 1Shailesh KumarNo ratings yet

- Company Law: Assignment ONDocument10 pagesCompany Law: Assignment ONsandeepNo ratings yet

- Law of InsuranceDocument7 pagesLaw of InsuranceJack Dowson100% (1)

- Avishek Insurance ProjectDocument15 pagesAvishek Insurance ProjectAvishek PathakNo ratings yet

- Dr. M.S. Raj-Purohit's Notes on Indian Limitation ActDocument10 pagesDr. M.S. Raj-Purohit's Notes on Indian Limitation ActRadhika Reddy50% (2)

- Life Insurance Claims & COPRA 1986Document34 pagesLife Insurance Claims & COPRA 1986Samhitha KandlakuntaNo ratings yet

- Growth of India's Insurance Industry from British Rule to Market ReformsDocument2 pagesGrowth of India's Insurance Industry from British Rule to Market ReformsSiddharth Cassonova BiswasNo ratings yet

- History of Insurance Law in India:: Section 2 (11), Insurance Act, 1938 Defines "Life Insurance Business"Document20 pagesHistory of Insurance Law in India:: Section 2 (11), Insurance Act, 1938 Defines "Life Insurance Business"shubham kumarNo ratings yet

- Meaning of Life Insurance and It Types of PoliciesDocument2 pagesMeaning of Life Insurance and It Types of Policiesshakti ranjan mohanty100% (1)

- Life InsuranceDocument2 pagesLife Insuranceshakti ranjan mohantyNo ratings yet

- Winding UpDocument20 pagesWinding Upshakti ranjan mohanty100% (2)

- Objects and Purposes of Company LegislationDocument7 pagesObjects and Purposes of Company Legislationshakti ranjan mohantyNo ratings yet

- Claims Management DepartmentDocument2 pagesClaims Management Departmentshakti ranjan mohantyNo ratings yet

- Indemnity and GuaranteeDocument10 pagesIndemnity and Guaranteeshakti ranjan mohantyNo ratings yet

- Insurance ContractDocument6 pagesInsurance Contractshakti ranjan mohantyNo ratings yet

- Functions of Life Insurance Corporation of IndiaDocument1 pageFunctions of Life Insurance Corporation of Indiashakti ranjan mohantyNo ratings yet

- Application of General Rules of Law of Contracts To Life InsuranceDocument1 pageApplication of General Rules of Law of Contracts To Life Insuranceshakti ranjan mohantyNo ratings yet

- Ingredients or Principles of Insurance LawDocument4 pagesIngredients or Principles of Insurance Lawshakti ranjan mohantyNo ratings yet

- The Formation of A CompanyDocument17 pagesThe Formation of A Companyshakti ranjan mohantyNo ratings yet

- The Memorandum and Articles of AssociationDocument15 pagesThe Memorandum and Articles of Associationshakti ranjan mohantyNo ratings yet

- Commercial Law AgencyDocument17 pagesCommercial Law Agencyshakti ranjan mohantyNo ratings yet

- DirectorsDocument23 pagesDirectorsshakti ranjan mohantyNo ratings yet

- Bailment and PledgeDocument8 pagesBailment and Pledgeshakti ranjan mohantyNo ratings yet

- Borrowing PowersDocument8 pagesBorrowing Powersshakti ranjan mohantyNo ratings yet

- Who Are The Children in Need of Care and ProtectionDocument7 pagesWho Are The Children in Need of Care and Protectionshakti ranjan mohanty100% (3)

- CapitalDocument26 pagesCapitalshakti ranjan mohantyNo ratings yet

- Juvenile Justice 2Document3 pagesJuvenile Justice 2shakti ranjan mohantyNo ratings yet

- Juvenile JusticeDocument2 pagesJuvenile Justiceshakti ranjan mohantyNo ratings yet

- Child Labor Laws in IndiaDocument1 pageChild Labor Laws in Indiashakti ranjan mohantyNo ratings yet

- Human Rights Are Those Rights Which Are Essential To Live As Human BeingsDocument2 pagesHuman Rights Are Those Rights Which Are Essential To Live As Human Beingsshakti ranjan mohantyNo ratings yet

- Child Prostitution in IndiaDocument9 pagesChild Prostitution in Indialawrence100% (1)

- History of Juvenile JusticeDocument2 pagesHistory of Juvenile Justiceshakti ranjan mohantyNo ratings yet

- Role of International Labour OrganizationDocument2 pagesRole of International Labour Organizationshakti ranjan mohantyNo ratings yet

- Child Trafficking in IndiaDocument2 pagesChild Trafficking in Indiashakti ranjan mohantyNo ratings yet

- Children in Conflict With LawDocument2 pagesChildren in Conflict With Lawshakti ranjan mohantyNo ratings yet

- Child Pornograhy Laws in IndiaDocument1 pageChild Pornograhy Laws in Indiashakti ranjan mohantyNo ratings yet

- Child Marriage Act IndiaDocument1 pageChild Marriage Act Indiashakti ranjan mohantyNo ratings yet

- Qatari Diar Nasser Al AnsariDocument3 pagesQatari Diar Nasser Al AnsariVani SaraswathiNo ratings yet

- Real Estate in India by AbhimanDocument24 pagesReal Estate in India by AbhimanabhimanbeheraNo ratings yet

- The Post Graduate Diploma in Education of The Zimbabwe Open University As A Tool For Socio-Economic TransformationDocument7 pagesThe Post Graduate Diploma in Education of The Zimbabwe Open University As A Tool For Socio-Economic TransformationinventionjournalsNo ratings yet

- Absa Personal Share Portfolio One PDFDocument2 pagesAbsa Personal Share Portfolio One PDFmarko joosteNo ratings yet

- Survey Questionnier For Startup BarriersDocument5 pagesSurvey Questionnier For Startup BarriersSarhangTahir100% (4)

- Aswath Damodaran - Valuation of SynergyDocument60 pagesAswath Damodaran - Valuation of SynergyIvaNo ratings yet

- 370 - 13735 - EA221 - 2010 - 1 - 1 - 1 - Linear Programming 1Document73 pages370 - 13735 - EA221 - 2010 - 1 - 1 - 1 - Linear Programming 1Catrina NunezNo ratings yet

- Date Open High Low Close Shares Traded Turnover (Rs. CR)Document2 pagesDate Open High Low Close Shares Traded Turnover (Rs. CR)Akshit JhingranNo ratings yet

- Corporate Profile and ServicesDocument43 pagesCorporate Profile and Servicesnavaid79No ratings yet

- Experienced CS Rohit Tyagi Seeks Finance RoleDocument3 pagesExperienced CS Rohit Tyagi Seeks Finance RoleroseNo ratings yet

- E IBD102008Document36 pagesE IBD102008cphanhuyNo ratings yet

- Chapter 7Document8 pagesChapter 7ne002No ratings yet

- Oecd Frascati ManualDocument402 pagesOecd Frascati Manualmarquez182No ratings yet

- ProjectReport Unilever WWKBDocument83 pagesProjectReport Unilever WWKBEmiria Ferida ShafianandaNo ratings yet

- ACC 1340 Financial Accounting - Chapter 1Document9 pagesACC 1340 Financial Accounting - Chapter 1Menaka KulathungaNo ratings yet

- Accounting Policies and Procedures ManualDocument32 pagesAccounting Policies and Procedures ManualAdmire Mamvura100% (2)

- Tower Sharing WHITE PAPERDocument12 pagesTower Sharing WHITE PAPERdipteshsinhaNo ratings yet

- CIBIL - Know Your Cibil Score - Get Your Cibil Score Deal4loansDocument2 pagesCIBIL - Know Your Cibil Score - Get Your Cibil Score Deal4loansVenkatrao GarigipatiNo ratings yet

- Constitution of Business and Classification of MSMEDocument30 pagesConstitution of Business and Classification of MSMERaj ChauhanNo ratings yet

- Financial Management 1 0Document80 pagesFinancial Management 1 0Awoke mulugetaNo ratings yet

- Channels - PlaceDocument23 pagesChannels - Placeuday369No ratings yet

- A Major Project Report On A Study of Awareness and Knowledge About Wealth Management Among IndividualsDocument51 pagesA Major Project Report On A Study of Awareness and Knowledge About Wealth Management Among IndividualsGaurav Solanki50% (2)

- Vallix QuestionnairesDocument14 pagesVallix QuestionnairesKathleen LucasNo ratings yet

- Financial Statement Analysis: I Ntegrated CaseDocument13 pagesFinancial Statement Analysis: I Ntegrated Casehtet sanNo ratings yet

- Revista AbbDocument84 pagesRevista Abbenrique zamoraNo ratings yet

- Narayana HealthcareDocument42 pagesNarayana HealthcarektejankarNo ratings yet

- Punjab Turkey ProjectDocument32 pagesPunjab Turkey ProjectFaisal BaigNo ratings yet

- Stock Market IndexDocument27 pagesStock Market Indexjubaida khanamNo ratings yet

- Introduction to Business Policy ChapterDocument7 pagesIntroduction to Business Policy ChapterMazumder Suman100% (1)

- Company Law Study PlanDocument10 pagesCompany Law Study PlanSheharyar RafiqNo ratings yet

- Outliers by Malcolm Gladwell - Book Summary: The Story of SuccessFrom EverandOutliers by Malcolm Gladwell - Book Summary: The Story of SuccessRating: 4.5 out of 5 stars4.5/5 (17)

- Nursing School Entrance Exams: HESI A2 / NLN PAX-RN / PSB-RN / RNEE / TEASFrom EverandNursing School Entrance Exams: HESI A2 / NLN PAX-RN / PSB-RN / RNEE / TEASNo ratings yet

- Real Property, Law Essentials: Governing Law for Law School and Bar Exam PrepFrom EverandReal Property, Law Essentials: Governing Law for Law School and Bar Exam PrepNo ratings yet

- The PMP Project Management Professional Certification Exam Study Guide PMBOK Seventh 7th Edition: The Complete Exam Prep With Practice Tests and Insider Tips & Tricks | Achieve a 98% Pass Rate on Your First AttemptFrom EverandThe PMP Project Management Professional Certification Exam Study Guide PMBOK Seventh 7th Edition: The Complete Exam Prep With Practice Tests and Insider Tips & Tricks | Achieve a 98% Pass Rate on Your First AttemptNo ratings yet

- FUNDAMENTALS OF NURSING: Passbooks Study GuideFrom EverandFUNDAMENTALS OF NURSING: Passbooks Study GuideRating: 5 out of 5 stars5/5 (1)

- 2023/2024 ASVAB For Dummies (+ 7 Practice Tests, Flashcards, & Videos Online)From Everand2023/2024 ASVAB For Dummies (+ 7 Practice Tests, Flashcards, & Videos Online)No ratings yet

- Radiographic Testing: Theory, Formulas, Terminology, and Interviews Q&AFrom EverandRadiographic Testing: Theory, Formulas, Terminology, and Interviews Q&ANo ratings yet

- The NCLEX-RN Exam Study Guide: Premium Edition: Proven Methods to Pass the NCLEX-RN Examination with Confidence – Extensive Next Generation NCLEX (NGN) Practice Test Questions with AnswersFrom EverandThe NCLEX-RN Exam Study Guide: Premium Edition: Proven Methods to Pass the NCLEX-RN Examination with Confidence – Extensive Next Generation NCLEX (NGN) Practice Test Questions with AnswersNo ratings yet

- EMT (Emergency Medical Technician) Crash Course with Online Practice Test, 2nd Edition: Get a Passing Score in Less TimeFrom EverandEMT (Emergency Medical Technician) Crash Course with Online Practice Test, 2nd Edition: Get a Passing Score in Less TimeRating: 3.5 out of 5 stars3.5/5 (3)

- Improve Your Global Business English: The Essential Toolkit for Writing and Communicating Across BordersFrom EverandImprove Your Global Business English: The Essential Toolkit for Writing and Communicating Across BordersRating: 4 out of 5 stars4/5 (14)

- EMT (Emergency Medical Technician) Crash Course Book + OnlineFrom EverandEMT (Emergency Medical Technician) Crash Course Book + OnlineRating: 4.5 out of 5 stars4.5/5 (4)

- PTCE - Pharmacy Technician Certification Exam Flashcard Book + OnlineFrom EverandPTCE - Pharmacy Technician Certification Exam Flashcard Book + OnlineNo ratings yet

- ASE A1 Engine Repair Study Guide: Complete Review & Test Prep For The ASE A1 Engine Repair Exam: With Three Full-Length Practice Tests & AnswersFrom EverandASE A1 Engine Repair Study Guide: Complete Review & Test Prep For The ASE A1 Engine Repair Exam: With Three Full-Length Practice Tests & AnswersNo ratings yet

- Check Your English Vocabulary for TOEFL: Essential words and phrases to help you maximise your TOEFL scoreFrom EverandCheck Your English Vocabulary for TOEFL: Essential words and phrases to help you maximise your TOEFL scoreRating: 5 out of 5 stars5/5 (1)

- The Science of Self-Discipline: The Willpower, Mental Toughness, and Self-Control to Resist Temptation and Achieve Your GoalsFrom EverandThe Science of Self-Discipline: The Willpower, Mental Toughness, and Self-Control to Resist Temptation and Achieve Your GoalsRating: 4.5 out of 5 stars4.5/5 (76)

- Driver CPC – the Official DVSA Guide for Professional Goods Vehicle Drivers: DVSA Safe Driving for Life SeriesFrom EverandDriver CPC – the Official DVSA Guide for Professional Goods Vehicle Drivers: DVSA Safe Driving for Life SeriesNo ratings yet

- Intermediate Accounting 2: a QuickStudy Digital Reference GuideFrom EverandIntermediate Accounting 2: a QuickStudy Digital Reference GuideNo ratings yet

- Summary of Sapiens: A Brief History of Humankind By Yuval Noah HarariFrom EverandSummary of Sapiens: A Brief History of Humankind By Yuval Noah HarariRating: 1 out of 5 stars1/5 (3)

- 2024 – 2025 FAA Drone License Exam Guide: A Simplified Approach to Passing the FAA Part 107 Drone License Exam at a sitting With Test Questions and AnswersFrom Everand2024 – 2025 FAA Drone License Exam Guide: A Simplified Approach to Passing the FAA Part 107 Drone License Exam at a sitting With Test Questions and AnswersNo ratings yet

- NCLEX-RN Exam Prep 2024-2025: 500 NCLEX-RN Test Prep Questions and Answers with ExplanationsFrom EverandNCLEX-RN Exam Prep 2024-2025: 500 NCLEX-RN Test Prep Questions and Answers with ExplanationsNo ratings yet

- Child Protective Services Specialist: Passbooks Study GuideFrom EverandChild Protective Services Specialist: Passbooks Study GuideNo ratings yet

- Python Handbook For Beginners. A Hands-On Crash Course For Kids, Newbies and Everybody ElseFrom EverandPython Handbook For Beginners. A Hands-On Crash Course For Kids, Newbies and Everybody ElseNo ratings yet