You might also like

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (894)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- CORPORATE INCOME TAX (Answer Key)Document5 pagesCORPORATE INCOME TAX (Answer Key)Rujean Salar AltejarNo ratings yet

- The Future of BankingDocument103 pagesThe Future of BankingKostas GeorgioyNo ratings yet

- The Global MinotaurDocument18 pagesThe Global MinotaurKostas GeorgioyNo ratings yet

- Chapter 5 Elasticity and Its ApplicationDocument41 pagesChapter 5 Elasticity and Its ApplicationeiaNo ratings yet

- Chapter 1Document93 pagesChapter 1Ranrave Marqueda DiangcoNo ratings yet

- Group 10 - Eyewear Industry - LenskartDocument46 pagesGroup 10 - Eyewear Industry - LenskartSargun Matta100% (3)

- Whittaker 2011 11 14 Lancaster University Eurosystem Debts, Greece and The Role of BanknotesDocument10 pagesWhittaker 2011 11 14 Lancaster University Eurosystem Debts, Greece and The Role of BanknotesssalovaaraNo ratings yet

- Bu 0612 1Document12 pagesBu 0612 1Kostas GeorgioyNo ratings yet

- SSRN Id2046184Document24 pagesSSRN Id2046184Kostas GeorgioyNo ratings yet

- Karagiannis Kon de As 60Document20 pagesKaragiannis Kon de As 60Kostas GeorgioyNo ratings yet

- Essqr March 2012 enDocument101 pagesEssqr March 2012 enKostas GeorgioyNo ratings yet

- Consumers and Mobile Financial Services March 2012Document70 pagesConsumers and Mobile Financial Services March 2012FedScoopNo ratings yet

- Surviving The Global Financial Crisis: Policy Research Working Paper 5946Document35 pagesSurviving The Global Financial Crisis: Policy Research Working Paper 5946Kostas GeorgioyNo ratings yet

- CDS Spreads in European Periphery Some Technical Issues To ConsiderDocument18 pagesCDS Spreads in European Periphery Some Technical Issues To ConsiderKostas GeorgioyNo ratings yet

- State of The World's Children 2012Document156 pagesState of The World's Children 2012ABC News OnlineNo ratings yet

- Oliveira2012-A New Global Price Unit Independent From Currency Units Proposed As Solution For The World Economic CrisesDocument5 pagesOliveira2012-A New Global Price Unit Independent From Currency Units Proposed As Solution For The World Economic CrisesKostas GeorgioyNo ratings yet

- Whole 59Document157 pagesWhole 59Kostas GeorgioyNo ratings yet

- Chick Ethics Feb121Document14 pagesChick Ethics Feb121Kostas GeorgioyNo ratings yet

- WP 1274Document25 pagesWP 1274Kostas GeorgioyNo ratings yet

- OECD Annual Inflation Rate Eases Slightly To 2.8% in January 2012Document3 pagesOECD Annual Inflation Rate Eases Slightly To 2.8% in January 2012Kostas GeorgioyNo ratings yet

- Golds Berry Sloan SubmissionDocument7 pagesGolds Berry Sloan SubmissionKostas GeorgioyNo ratings yet

- Measuring Well-Being and Fostering Progress An Asia-Pacifi C Perspective by The OECD Statistics DirectorateDocument19 pagesMeasuring Well-Being and Fostering Progress An Asia-Pacifi C Perspective by The OECD Statistics DirectorateKostas GeorgioyNo ratings yet

- Bullard 7 Faces of Peril 2010Document14 pagesBullard 7 Faces of Peril 2010jasonbremerNo ratings yet

- Crises, Labor Market Policy, and Unemployment: Lorenzo E. Bernal-Verdugo, Davide Furceri, and Dominique GuillaumeDocument29 pagesCrises, Labor Market Policy, and Unemployment: Lorenzo E. Bernal-Verdugo, Davide Furceri, and Dominique GuillaumeKostas GeorgioyNo ratings yet

- Greece 2012 02Document24 pagesGreece 2012 02jjopaNo ratings yet

- EPB6Document10 pagesEPB6Kostas GeorgioyNo ratings yet

- WP 1264Document28 pagesWP 1264Kostas GeorgioyNo ratings yet

- WEF Global Risks Report 2012Document64 pagesWEF Global Risks Report 2012leithvanonselenNo ratings yet

- 111811Document41 pages111811Kostas GeorgioyNo ratings yet

- Issue2 1Document12 pagesIssue2 1Kostas GeorgioyNo ratings yet

- Ecp 447 enDocument179 pagesEcp 447 enKostas GeorgioyNo ratings yet

- 110601mankiew The Reincarnation of Keynesian EconomicsDocument13 pages110601mankiew The Reincarnation of Keynesian EconomicsSantiago PetriNo ratings yet

- WP 1237Document36 pagesWP 1237Kostas GeorgioyNo ratings yet

- Tender Pack RK3145-TE08 Concrete Lined Open DrainsDocument68 pagesTender Pack RK3145-TE08 Concrete Lined Open DrainsMahleka ConstructionNo ratings yet

- Assignment 2 1Document9 pagesAssignment 2 1api-226053416No ratings yet

- Customer BookDocument19 pagesCustomer BookEugen CrasovskiNo ratings yet

- Swe2005-Software Testing: Verification and Validation TestingDocument28 pagesSwe2005-Software Testing: Verification and Validation TestingKarthik GoudNo ratings yet

- (Offline) Rundown Awarding AiseefDocument4 pages(Offline) Rundown Awarding AiseefFanji HastomoNo ratings yet

- Tutorial 3 DB U2000429Document3 pagesTutorial 3 DB U2000429Haikal HaziqNo ratings yet

- Comparative Valuation of Strides With Its Competitors Using Relative Valuation TechniqueDocument26 pagesComparative Valuation of Strides With Its Competitors Using Relative Valuation TechniqueVipin ChandraNo ratings yet

- FM - Hosp - Tutorial 5Document7 pagesFM - Hosp - Tutorial 5Sylvia AnneNo ratings yet

- PT Karya Mandri Accounts SummaryDocument2 pagesPT Karya Mandri Accounts SummaryFerdi PutraNo ratings yet

- Train Depot.V08 PDFDocument3 pagesTrain Depot.V08 PDFrdricheyNo ratings yet

- Budget Speech Urdu 2020 21Document42 pagesBudget Speech Urdu 2020 21DawndotcomNo ratings yet

- Simplify The Above ParagraphDocument56 pagesSimplify The Above ParagraphAmjad NiaziNo ratings yet

- Root of All EvilDocument8 pagesRoot of All EvilKostNo ratings yet

- Brand Building Block, 111172033Document2 pagesBrand Building Block, 111172033Barson MithunNo ratings yet

- LofransCat LowRec 2019Document72 pagesLofransCat LowRec 2019Mauricio Da Cunha AlmeidaNo ratings yet

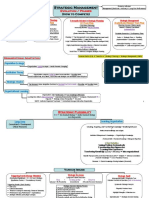

- Strategic Management - Chapter (1) - Modified Maps - Coloured - March 2021Document4 pagesStrategic Management - Chapter (1) - Modified Maps - Coloured - March 2021ahmedgelixNo ratings yet

- Hindustan TimesDocument65 pagesHindustan TimesPREETNo ratings yet

- 1 Fundamentals of Market Research 2 1Document34 pages1 Fundamentals of Market Research 2 1Reem HassanNo ratings yet

- Digital Platform & Ecosystem DefinitionsDocument16 pagesDigital Platform & Ecosystem DefinitionsSyayu ZhukhruffaNo ratings yet

- Introduction of The CompanyDocument25 pagesIntroduction of The CompanynareshNo ratings yet

- Rek April2023Document14 pagesRek April2023asna simamoraNo ratings yet

- E-Commerce 2015 11th Edition Laudon Solutions Manual 1Document36 pagesE-Commerce 2015 11th Edition Laudon Solutions Manual 1joshuamooreqicoykmtan100% (21)

- Competitive Analysis: Top 5 CompetitorsDocument5 pagesCompetitive Analysis: Top 5 Competitorssonakshi mathurNo ratings yet

- Compact Printed Circuit Heat ExchangerDocument3 pagesCompact Printed Circuit Heat ExchangerNur Amanina50% (2)

- Zerrudo ENTREP ANSWER SHEETSDocument8 pagesZerrudo ENTREP ANSWER SHEETSGlen DaleNo ratings yet

- 42k S4hana2021 Set-Up en XXDocument166 pages42k S4hana2021 Set-Up en XXarunkumar dharmarajanNo ratings yet